EXTEND

& PRETEND:

Is the US Facing a Cash Crunch?

The

US Government is caught in a cash vise and is being squeezed between

too slow a rebound in tax revenues and the limitations on how quickly it

can realistically take its funding requirements to the US Treasury

auction. The US Treasury was saved in March by what the government reports

as �proprietary receipts�. Those receipts require an explanation that is

not well publicized since it begs the question of what happens next month

without the $117 BILLION journal entry.

The

US Government is caught in a cash vise and is being squeezed between

too slow a rebound in tax revenues and the limitations on how quickly it

can realistically take its funding requirements to the US Treasury

auction. The US Treasury was saved in March by what the government reports

as �proprietary receipts�. Those receipts require an explanation that is

not well publicized since it begs the question of what happens next month

without the $117 BILLION journal entry.

The March cash management numbers from the US Treasury�s Financial

Management Service are alarming and in my estimation have become perilous.

The economy is simply taking much too long to recover which is affecting

urgently required tax receipts.

If the US Treasury issues even higher debt supply to the market too fast,

it threatens driving up interest rates prematurely and thereby elevating

already strained government financing costs despite already increased

supply. Since the US government has steadily reduced maturity duration

over the last few years to obfuscate a growing debt problem, the issue is

compounded by the rapidly increasing levels of roll-over funding now

additionally being required.

It is a tricky balance between gauging how fast tax receipts will return

and what supply the monthly treasury auction is able to absorb. Cash flow

is the primary reason small businesses fail unexpectedly. This is also why

sovereign governments fail abruptly.

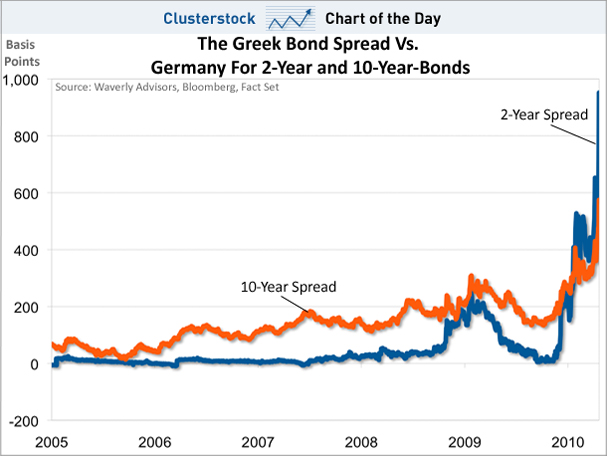

We witnessed in Greece what happens when investors get nervous. Yields not

only spike but typically

move to even higher levels than most originally

thought possible.

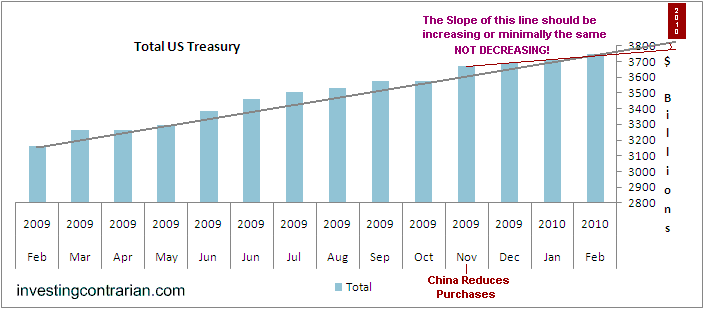

US TREASURY CASH

REQUIREMENTS

On April 14th the Financial Management Service, a bureau of the

US Department of the Treasury released its

Monthly Treasury Statement for March 2010. I was waiting for

it because of what I saw in February - the gap between receipts

and outlays was widening disturbingly.

I knew the US Treasury was going to have to pull a �rabbit out of a hat�

or we might see a similar scare in the US Treasury Auction, with a spike

in treasury yields that occurred in Greece. What was reported was a

mystery and for those that read

Extend & Pretend: Gaming the US Tax Payer, I will call this Suspicious

Clue #8.

SUSPICIOUS CLUE #8

-

PROPRIETARY RECEIPTS FROM THE PUBLIC

CLICK TO ENLARGE

The report shows US Treasury receipts were down disturbingly and almost

all government outlays were up. I personally have had Profit & Loss

responsibility on numerous occasions during my career and I would have

been apprehensive facing the auditors or board of directors with such a

blatant example of mismanagement. Absolutely no cuts in expenses, with

falling revenues, all made to marginally appear better than the February

report by a single line item called �other�. Executives get fired for

such a report but governments just carry on until the inevitable crisis

event finally occurs. Then the traditional blame game begins, blame is

assigned and belated and poorly formulated policy responses are enacted.

So what is this �other�? When you examine the Outlay Ledger of the

Department of the Treasury for March 2010 (below) you see it to be a

onetime item classified as a negative outlay. For the non accountants, this

is a government receipt that is placed in the outlays as a negative amount,

thereby showing government outlays to be smaller than they otherwise would

have been. Though this is acceptable accounting it would lead to the wrong

conclusions, unless you read the details buried in the back pages. This

�other� is referred to as a �Proprietary Receipt from the Public�.

An IRS document explains just what that means in an accounting context:

"Proprietary Receipts from the Public are collections from outside the

Government that are deposited in receipt accounts that arise as a result

of the Government�s business-type or market-oriented activities. Among

these are interest received, proceeds from the sale of property and

products, charges for non-regulatory services, and rents and

royalties."(2)

This is a $117.3 BILLION amount!! The total 2010 US Tax receipts

for US Corporations is only budgeted to be $157 Billion!

CLICK TO ENLARGE

My investigations suggest that it is likely

suspiciously engineered TARP (Troubled Asset Relief

Program) money being returned to the US Treasury, along with a slowdown in

TARP issuance versus budget. Assuming this is the case, and not simply an

aircraft carrier or two we have sold and are now leasing back, like

California is doing with all state owned buildings, we still have a major

problem. What happens next month? The TARP fund returns will stop or we

will run out of aircraft carriers. Is unemployment going to surge or

are corporate tax receipts going to expand by over $117B next month?

Timothy Geithner and the US Treasury somehow dodged the bullet because

of �other� this month. How does it look for next month for cash

management? Let�s consider tax receipts to see if there is a possible

�rabbit in the hat� there.

TAX RECEIPTS

You personally met your April 15th tax filing deadline and you

likely took some consolation in your tax frustrations by knowing you

weren�t alone. The quiet truth is you are becoming more alone each year if

you haven�t understood the new realities of the US Tax game. 47% of

Americans (3) and two-thirds of US corporations (4) will pay no taxes in

2010. Where do you fit? These are pretty startling revelations to most

of us and don�t bode well to fixing the monthly Treasury cash requirements

quickly, especially with unemployment still stubbornly elevated.

PERSONAL INCOME TAX

The Associated Press reported on April 7th, 2010.

About

47 percent will pay no federal income taxes at all for 2009.

Either their incomes were too low, or they qualified for enough credits,

deductions and exemptions to eliminate their liability. That's according

to projections by the Tax Policy Center, a Washington research

organization.

About

47 percent will pay no federal income taxes at all for 2009.

Either their incomes were too low, or they qualified for enough credits,

deductions and exemptions to eliminate their liability. That's according

to projections by the Tax Policy Center, a Washington research

organization.

In recent years, credits for low- and middle-income families have grown

so much that a family of four making as much as $50,000 will owe no

federal income tax for 2009, as long as there are two children younger

than 17, according to a separate analysis by the consulting firm

Deloitte Tax.

Tax cuts enacted in the past decade have been generous to wealthy

taxpayers, too, making them a target for President Barack Obama and

Democrats in Congress. Less noticed were tax cuts for low- and

middle-income families, which were expanded when Obama signed the

massive economic recovery package last year.

The result is a tax system that exempts almost half the country from

paying for programs that benefit everyone,

including national defense, public safety, infrastructure and education.

It is a system in which the top 10 percent of earners � households

making an average of $366,400 in 2006 � paid about 73 percent of the

income taxes collected by the federal government.

EXAMPLE

The family was entitled to a standard deduction of $11,400 and four

personal exemptions of $3,650 apiece, leaving a taxable income of

$24,000. The federal income tax on $24,000 is $2,769. With two children

younger than 17, the family qualified for two $1,000 child tax credits.

Its Making Work Pay credit was $800 because the parents were married

filing jointly. The $2,800 in credits exceeds the $2,769 in taxes, so

the family makes a $31 profit from the federal income tax. That ought to

take the sting out of April 15.

With the government presently talking about once again extending

unemployment benefits, it appears we have more downside than upside on the

income tax revenue receipt line item going forward.

CORPORATE TAX

The Center for American Progress reported in 2004, while fighting President

George W Bush�s further cuts in corporate taxation:

The news that more than 60 percent of U.S. corporations failed to pay

any federal taxes from 1996 through 2000 when corporate profits were

soaring and that corporate tax receipts had fallen to just 7.4 percent

of overall federal tax revenue in 2003 � the lowest since 1983 and the

second-lowest rate since 1934 � is an outrage. But it should come as no

surprise to anyone who has been paying attention to national tax policy

over the past few years. The General Accounting Office (GAO) report also

found that an astonishing 94 percent of corporations reported tax

liability of less than 5 percent of their total income during the same

time period.

The last Special General Accounting Office (GAO) study concerning

corporate taxation was in 2004 and it showed:

The corporate income tax rate is ostensibly 35 percent, but companies

are able to reduce their effective burden by claiming various deductions

and credits. US companies paid an average of $11.88 (1.19 percent) in

corporate taxes for every $1,000 in gross receipts, the study said.

Foreign-owned

companies fared better in some respects than their US-based competitors.

The report found that 71 percent of foreign-controlled corporations

paid no taxes on their US income, while 89 percent had liabilities of

less than 5 percent of their income.

Foreign-owned

companies fared better in some respects than their US-based competitors.

The report found that 71 percent of foreign-controlled corporations

paid no taxes on their US income, while 89 percent had liabilities of

less than 5 percent of their income.

The GAO didn't attempt to determine why so many companies were able to

avoid paying taxes. It said possible explanations included legitimate

deductions for current-year operating losses, losses carried forward

from previous years, and sufficient credits to offset any tax

liabilities. In addition, it said improper pricing of transactions

between US and foreign operations could contribute to tax avoidance.

The percentage of federal tax collections paid by corporations has

tumbled from a high of 39.8 percent in 1943 to a low of 7.4 percent last

year. It ranged from 10 percent to 11 percent in 1996-2000, the period

studied by the GAO.

Boston Globe

04-11-04

In 2005 the GAO issued another report. The Washington Post�s analysis in

Many Firms didn�t pay Taxes highlighted:

About two-thirds of corporations operating in the United States did not

pay taxes annually from 1998 to 2005. In 2005, after collectively making

$2.5 trillion in sales, corporations gave a variety of reasons on their

tax returns to account for the absence of taxable revenue. The most

frequently listed included the cost of producing their goods, salary

expenses and interest payments on their debt, the report said. The GAO

did not analyze whether the firms had profits that should have been

taxed.

Sen. Byron L. Dorgan (D-N.D.) called the findings "a shocking indictment

of the current tax system."

"It's

shameful that so many corporations make big profits and pay nothing to

support our country," he said. "The tax system that allows this

wholesale tax avoidance is an embarrassment and unfair to hardworking

Americans

who pay their fair share of taxes. We need to plug these tax loopholes

and put these corporations back on the tax rolls."

Eric Toder, a senior fellow at the Urban Institute, said the vast

majority of corporations are small businesses and start-ups that have

adopted a corporate structure that allows them to lower their tax bills.

"I'm not trying to imply that there aren't tax-compliance issues among

small corporations," he said. "But when you are talking about businesses

that size, I would suspect the norm would be to not pay taxes, and

there's nothing nefarious about that." Toder had not yet seen the GAO

study.

A greater proportion of large corporations pay taxes, according to the

GAO. In 2005, about 28 percent of large corporations paid no taxes. Of

the 1.3 million corporations included in the study, 998 were categorized

as "large."

Dorgan and Sen. Carl M. Levin (D-Mich.) requested the report out of

concern that some corporations were using "transfer pricing" to

reduce their tax bills. The practice allows multi-national companies to

transfer goods and assets between internal divisions so they can record

income in a jurisdiction with low tax rates.

The GAO said data on transfer pricing were scarce. Instead, it compared

the percentages of foreign- and U.S.-controlled corporations that are

paying taxes.

In general, the GAO found that slightly more foreign firms paid no

taxes. From 1998 to 2005, 68 percent of foreign-controlled

corporations sent nothing to the Internal Revenue Service, compared with

66 percent of U.S. companies. The report noted in an opening paragraph,

however, that the GAO did not study whether the foreign companies were

using transfer pricing.

Still, Levin said: "This report makes clear that too many corporations

are using tax trickery to send their profits overseas and avoid paying

their fair share in the United States."

It has only become worse, with President George W Bush tax cuts and corporate friendly

tax policy. President Barack Obama has been preoccupied with spending to

consider revenue receipts as a priority.

Additionally, offshore tax accounting is completely un-policed

and highly secretive with approximately 30 countries serving as tax havens to help corporations avoid taxes. The addition of

$605T derivatives market now makes it almost impossible to police global

corporations from tax avoidance.

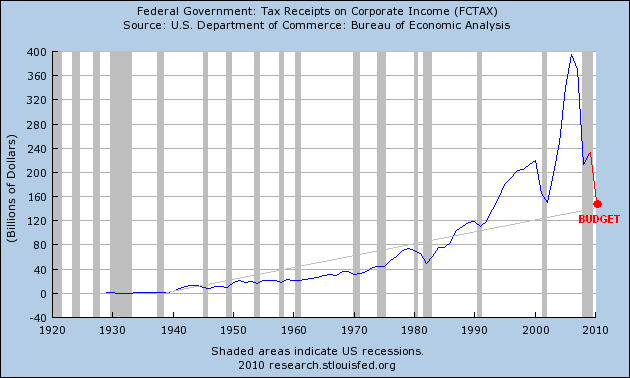

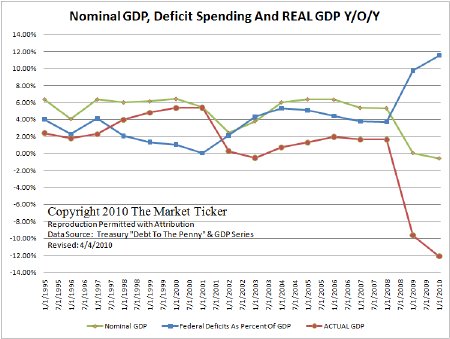

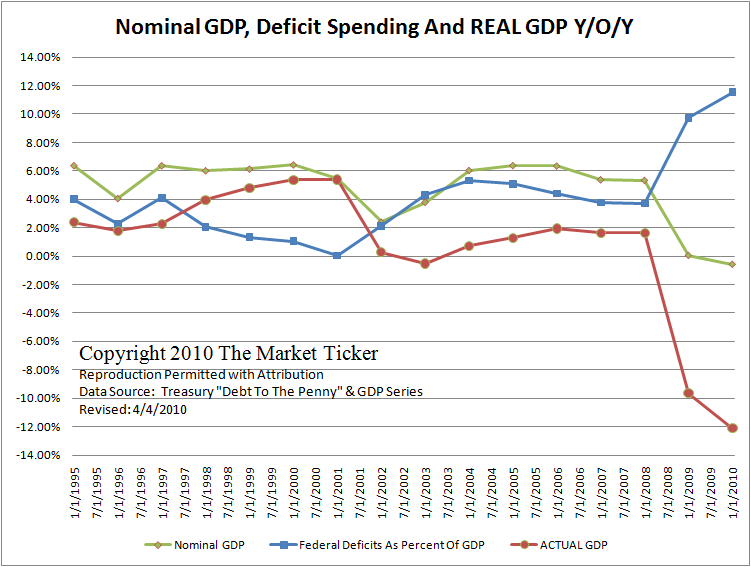

Below is the current Federal Reserve�s Tax Receipts on Corporate Income

where I have added the budget expectation for 2010 of $156.7B. As you have

already seen, we are presently falling behind last year's rate of tax

receipts.

When we

compare corporate tax receipts to Nominal GDP we see huge disparities that

are now built into the US Corporate Taxation policy. When GDP was growing,

US Taxation was not. The effective rates after loopholes and

offshore accounting created the following results.

A HORRIFIC CHART

Corporate and Personal taxes are not going to materially fix the US Cash Crunch

short term.

This alarming chart suggests one or more of three possibilities:

1- There is no relationship between corporate taxes and GDP.

2- Corporate pretax profits have seen near exponential growth over the

last 30 years without being reflected in US taxes receipts.

3- Pretax corporate profits have become more and more an offshore

phenomone.

In an analysis of taxes paid by 275 of the largest U.S. corporations,

the liberal watchdog group Citizens for Tax Justice found that effective

corporate tax rates have fallen by 20 percent since 2001, even as pretax

profits jumped 26 percent. Between 2001 and 2003, the 275 companies paid

taxes totaling 18.4 percent on their total profits, about half the 35

percent corporate income tax rate. Of the 275, 82 either paid no

taxes or received large refunds in at least one of the past three years.

The

Washington Post

12-26-04

Investors are operating under the notion that an improvement in the

economy and employment will alleviate the pressures on the Treasury

Auction. This notion I believe is misplaced. Though I am skeptical about

significant improvements in either the economy or employment, this view is

mute in comparison to what will actually be required to make a material

difference to tax receipts. The problems described above are intractable

without major congressional policy initiatives. Congress is presently

doing nothing to address them. In fact they are headed in absolutely the

opposite direction.

So the question is even more difficult to answer. Where will tax receipts

come from to keep the US Treasury from being forced to place accelerating

supply on the monthly Treasury Auction?

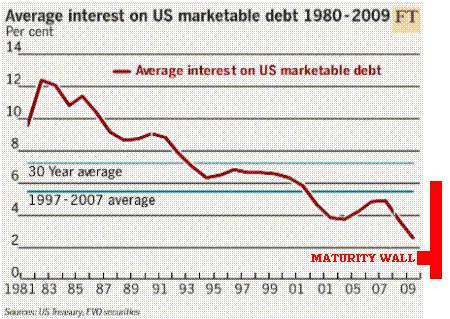

DEBT ISSUANCE

I know

many of you are saying we will just be forced to place more supply

on the Treasury Auction and accept higher rates. As I mentioned earlier,

the US

has

already moved down the duration curve steadily over the last

few years to make increasing debt levels less onerous. It obviously comes

with huge risk, considering interest rates are at all time historic lows.

If we were forced to refinance the national debt at 5.5% versus the

average maturity of just over 2% shown above, we would have a serious

problem. We need to place corporate tax receipts versus interest payment

rate charges in perspective.

|

$14T National Debt at 5.5% |

$770B |

|

$14 T National Debt @ a 3% difference |

$420B |

|

Total US Corporate Income Tax Budget for 2010 |

$157B |

This is too

far out to be critical to our monthly cash management concerns, but is

still a major strategic consideration affecting short term US Treasury

Auction options. Closer in however, the US Treasury is obviously caught in

a vise about not pushing rates up any faster than absolutely necessary for

concern that in the not too distant future the very existence of the US

and its ability to service its debt may be at stake.

CONCLUSION

The US cash

management challenge is significant. Taking out this month�s �plug�

number, any surprises or further delays in economic rebound will

likely trigger serious market reactions.

�This story is not going

to stop at the end of the year.

There is inertia in the

deterioration of credit metrics.�

Moody�s Investor Services

Sign Up for the next release in the

Extend & Pretend series:

Commentary

SOURCES:

(1) 04-14-10

March

2010t Issue: Monthly Treasury Statement: Publications & Guidance:

Financial Management Service

(2) 04-13-10

The

incredible shrinking deficit

Salon.com

(3) 04-07-10

Nearly half of US households escape fed income tax

AP

(4) 04-11-04

Most

US firms paid no income taxes in '90s

Boston Globe

(5) 12-26-04

Corporate Taxes: Going, Going

The Washington Post

The last Extend & Pretend article:

EXTEND & PRETEND - Gaming the US Tax Payer

Gordon T Long

Tipping Points

Mr. Long is a former senior group executive with IBM & Motorola, a

principle in a high tech public start-up and founder of a private venture

capital fund. He is presently involved in private equity placements

internationally along with proprietary trading involving the development &

application of Chaos Theory and Mandelbrot Generator algorithms.

Gordon T Long is not a registered advisor and does not give investment

advice. His comments are an expression of opinion only and should not be

construed in any manner whatsoever as recommendations to buy or sell a

stock, option, future, bond, commodity or any other financial instrument

at any time. While he believes his statements to be true, they always

depend on the reliability of his own credible sources. Of course, he

recommends that you consult with a qualified investment advisor, one

licensed by appropriate regulatory agencies in your legal jurisdiction,

before making any investment decisions, and barring that, you are

encouraged to confirm the facts on your own before making important

investment commitments.

� Copyright 2010 Gordon T Long. The information herein was obtained from

sources which Mr. Long believes reliable, but he does not guarantee its

accuracy. None of the information, advertisements, website links, or any

opinions expressed constitutes a solicitation of the purchase or sale of

any securities or commodities. Please note that Mr. Long may already have

invested or may from time to time invest in securities that are

recommended or otherwise covered on this website. Mr. Long does not intend

to disclose the extent of any current holdings or future transactions with

respect to any particular security. You should consider this possibility

before investing in any security based upon statements and information

contained in any report, post, comment or recommendation you receive from

him.

{kind=link}