TIPPING POINT: "The moment of critical mass, the threshold, the boiling point"

The tipping point is the critical point in an evolving situation that leads to a new and irreversible development. The term is said to have originated in the field of epidemiology when an infectious disease reaches a point beyond any local ability to control it from spreading more widely. A tipping point is often considered to be a turning point. The term is now used in many fields. Journalists apply it to social phenomena, demographic data, and almost any change that is likely to lead to additional consequences. Marketers see it as a threshold that, once reached, will result in additional sales. In some usage, a tipping point is simply an addition or increment that in itself might not seem extraordinary but that unexpectedly is just the amount of additional change that will lead to a big effect. In the butterfly effect of chaos theory , for example, the small flap of the butterfly's wings that in time leads to unexpected and unpredictable results could be considered a tipping point. However, more often, the effects of reaching a tipping point are more immediately evident. A tipping point may simply occur because a critical mass has been reached.

The Tipping Point: How Little Things Can Make a Big Difference is a book by Malcolm Gladwell, first published by Little Brown in 2000. Gladwell defines a tipping point as "the moment of critical mass, the threshold, the boiling point." The book seeks to explain and describe the "mysterious" sociological changes that mark everyday life. As Gladwell states, "Ideas and products and messages and behaviors spread like viruses do."

The three rules of epidemics

Gladwell describes the "three rules of epidemics" (or the three "agents of change") in the tipping points of epidemics.

"The Law of the Few", or, as Gladwell states, "The success of any kind of social epidemic is heavily dependent on the involvement of people with a particular and rare set of social gifts."According to Gladwell, economists call this the "80/20 Principle, which is the idea that in any situation roughly 80 percent of the 'work' will be done by 20 percent of the participants."(see Pareto Principle) These people are described in the following ways:

Connectors are the people who "link us up with the world ... people with a special gift for bringing the world together." They are "a handful of people with a truly extraordinary knack [... for] making friends and acquaintances". He characterizes these individuals as having social networks of over one hundred people. To illustrate, Gladwell cites the following examples: the midnight ride of Paul Revere, Milgram's experiments in the small world problem, the "Six Degrees of Kevin Bacon" trivia game, Dallas businessman Roger Horchow, and ChicagoanLois Weisberg, a person who understands the concept of the weak tie. Gladwell attributes the social success of Connectors to "their ability to span many different worlds [... as] a function of something intrinsic to their personality, some combination of curiosity, self-confidence, sociability, and energy."

Mavens are "information specialists", or "people we rely upon to connect us with new information." They accumulate knowledge, especially about the marketplace, and know how to share it with others. Gladwell cites Mark Alpert as a prototypical Maven who is "almost pathologically helpful", further adding, "he can't help himself". In this vein, Alpert himself concedes, "A Maven is someone who wants to solve other people's problems, generally by solving his own". According to Gladwell, Mavens start "word-of-mouth epidemics" due to their knowledge, social skills, and ability to communicate. As Gladwell states, "Mavens are really information brokers, sharing and trading what they know".

Salesmen are "persuaders", charismatic people with powerful negotiation skills. They tend to have an indefinable trait that goes beyond what they say, which makes others want to agree with them. Gladwell's examples include California businessman Tom Gau and news anchorPeter Jennings, and he cites several studies about the persuasive implications of non-verbal cues, including a headphone nod study (conducted by Gary Wells of the University of Alberta and Richard Petty of the University of Missouri) and William Condon's cultural microrhythms study.

The Stickiness Factor, the specific content of a message that renders its impact memorable. Popular children's television programs such as Sesame Street and Blue's Clues pioneered the properties of the stickiness factor, thus enhancing the effective retention of the educational content in tandem with its entertainment value.

The Power of Context: Human behavior is sensitive to and strongly influenced by its environment. As Gladwell says, "Epidemics are sensitive to the conditions and circumstances of the times and places in which they occur." For example, "zero tolerance" efforts to combat minor crimes such as fare-beating and vandalism on the New York subway led to a decline in more violent crimes city-wide. Gladwell describes the bystander effect, and explains how Dunbar's number plays into the tipping point, using Rebecca Wells' novel Divine Secrets of the Ya-Ya Sisterhood, evangelistJohn Wesley, and the high-tech firm W. L. Gore and Associates. Gladwell also discusses what he dubs the rule of 150, which states that the optimal number of individuals in a society that someone can have real social relationships with is 150.

LOOKUP KEY

to Current

Global-Macro

Tipping Points

Roll mouse over Tipping Points below

for details on each.

KEY TO TIPPING POINTS

1 - Risk Reversal

2 - China Hard Landing

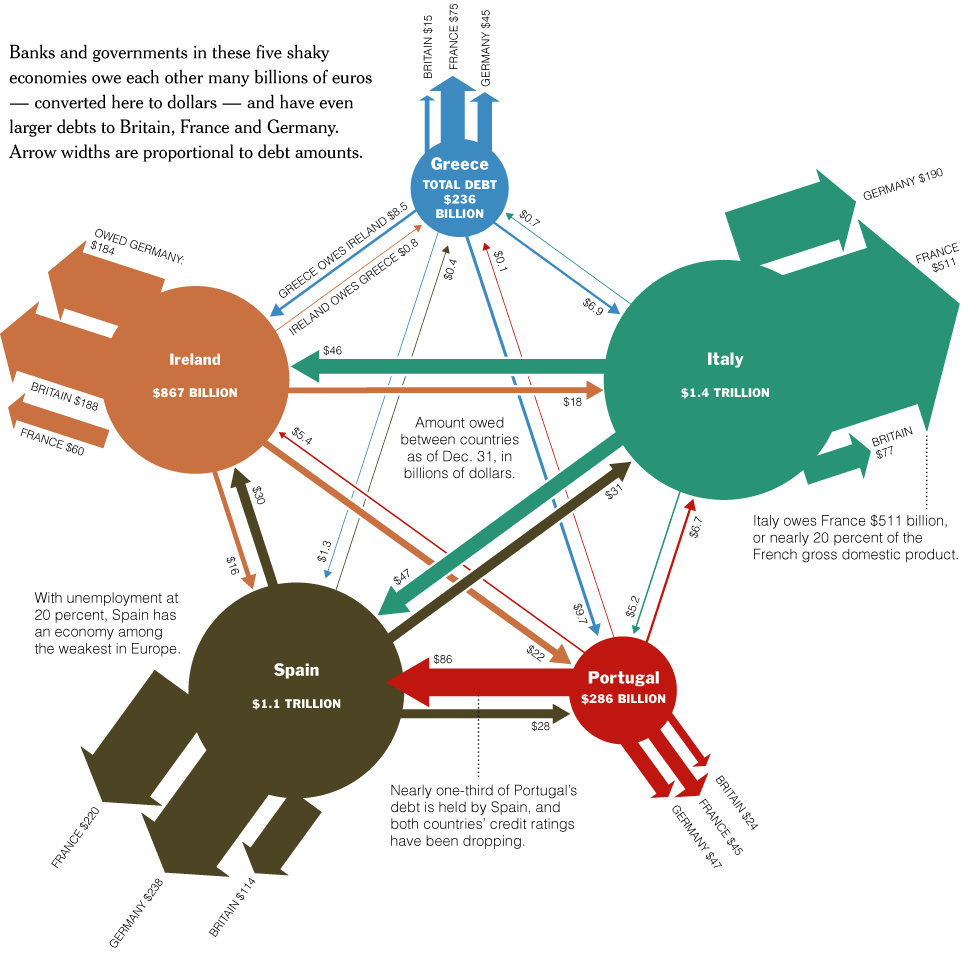

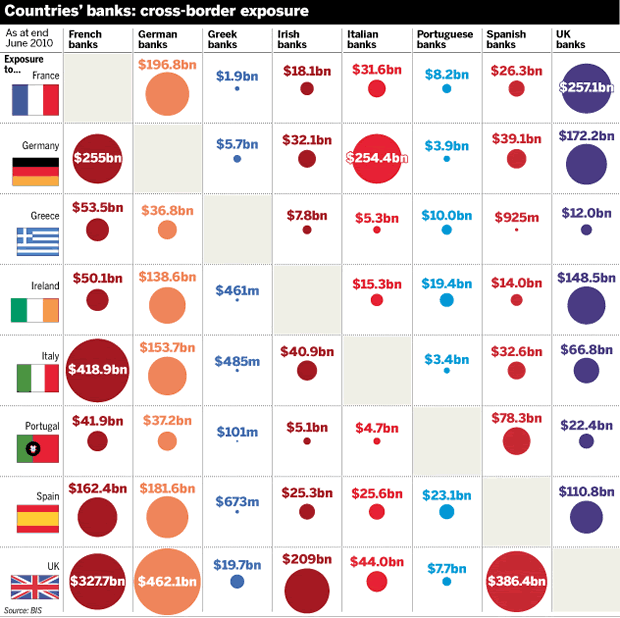

3- EU Banking Crisis

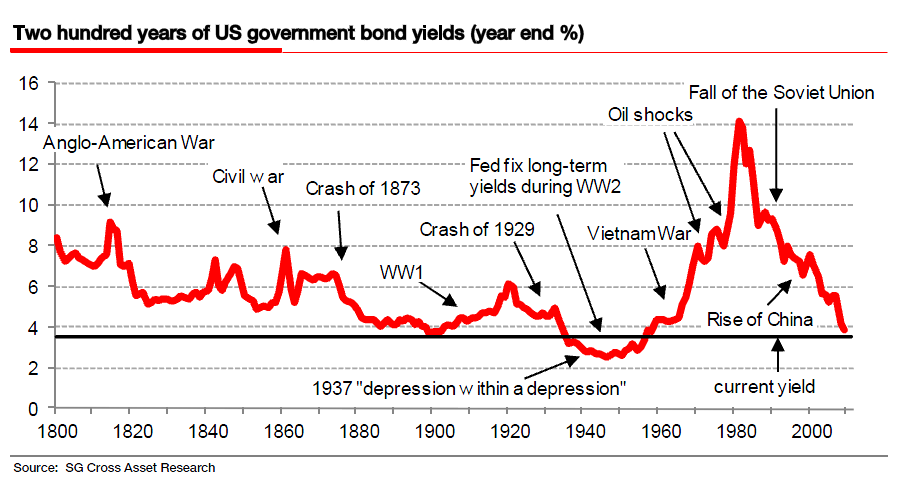

4- Bond Bubble

5 - Geo-Political Event

6 - Japan Debt Deflation Spiral

7 - US Stock Market Valuations

8 - Shrinking Revenue Growth Rate

9 - Credit Contraction II

10 - US Dollar

NEW Stagflation - Slow Growth & Personal Inflation

FAIR USE NOTICEThis site contains

copyrighted material the use of which has not always been specifically

authorized by the copyright owner. We are making such material available in

our efforts to advance understanding of environmental, political, human

rights, economic, democracy, scientific, and social justice issues, etc. We

believe this constitutes a 'fair use' of any such copyrighted material as

provided for in section 107 of the US Copyright Law. In accordance with

Title 17 U.S.C. Section 107, the material on this site is distributed

without profit to those who have expressed a prior interest in receiving the

included information for research and educational purposes.

If you wish to use

copyrighted material from this site for purposes of your own that go beyond

'fair use', you must obtain permission from the copyright owner.

DISCLOSURE Gordon T Long is not a registered advisor and does not give investment advice. His comments are an expression of opinion only and should not be construed in any manner whatsoever as recommendations to buy or sell a stock, option, future, bond, commodity or any other financial instrument at any time. While he believes his statements to be true, they always depend on the reliability of his own credible sources. Of course, he recommends that you consult with a qualified investment advisor, one licensed by appropriate regulatory agencies in your legal jurisdiction, before making any investment decisions, and barring that, we encourage you confirm the facts on your own before making important investment commitments.

Inverted chart of 30-year Treasury yields courtesy of Doug Short and Chris Kimble. As you can see, yields are at a "support" area that's held for 17 years.

If it breaks down (i.e., yields break out) watch out!

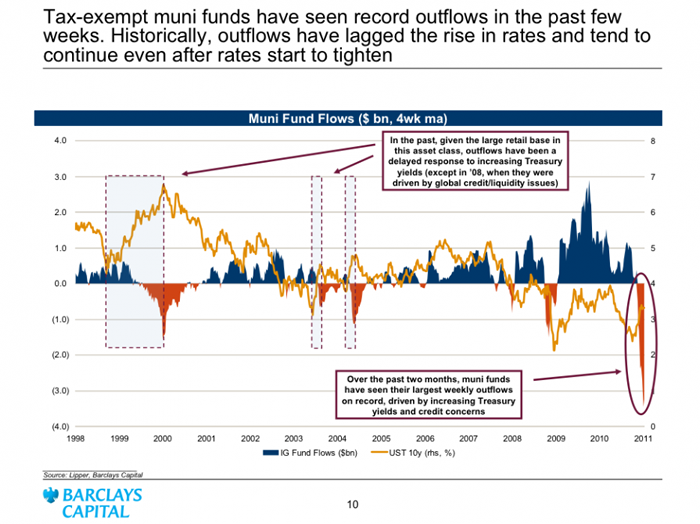

The state budget crisis will continue next year, and it could be worse than ever. That's part of what's freaking out muni investors, who last week dumped them like they haven't in ages.

States face a $112.3 billion gap for next year, according to the Center on Budget and Policy Priorities. If the shortfall grows during the year -- as it does in most years -- FY2012 will approach the record $191 billion gap of 2010. Remember, with each successive shortfall state budgets have become more bare.

Things could be especially bad if House Republicans push through a plan to cut off non-security discretionary funding for states, opening an additional $32 billion gap.

MUNI BOND OUTFLOWS

RISK REVERSAL

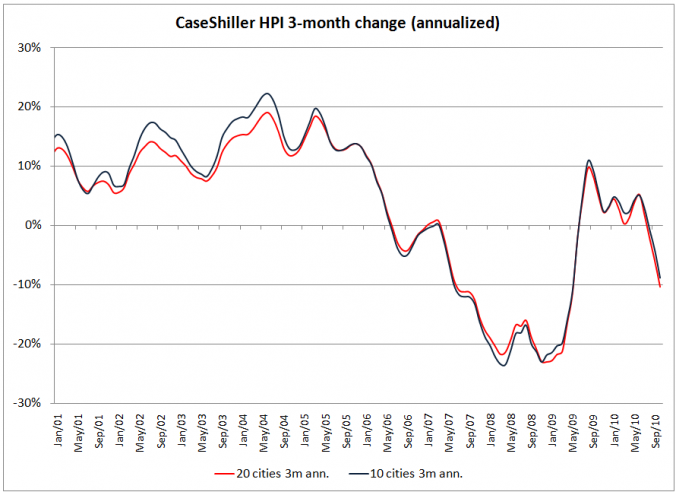

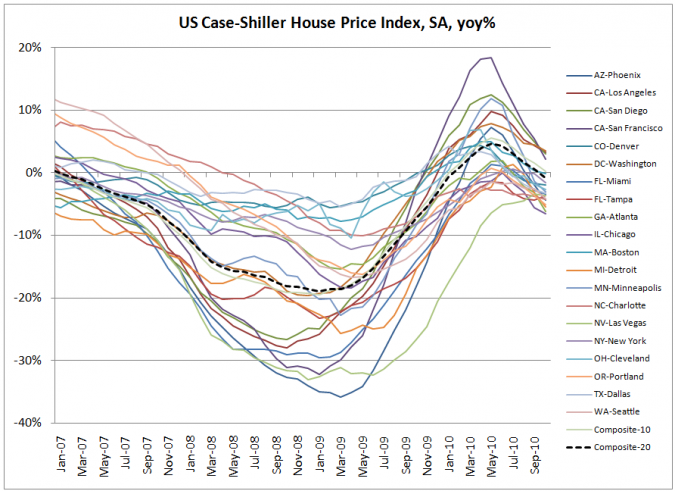

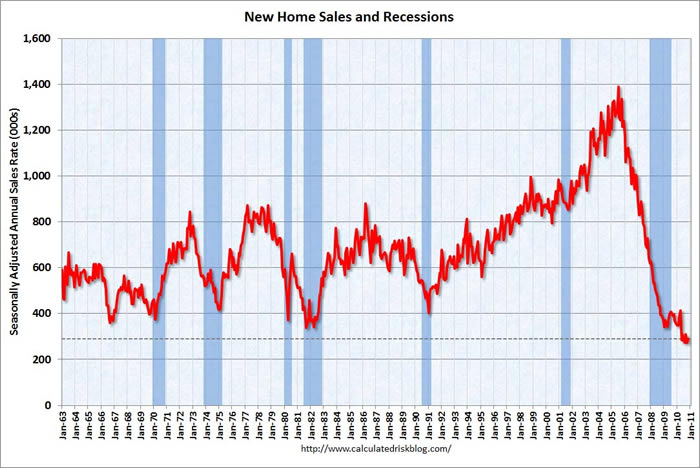

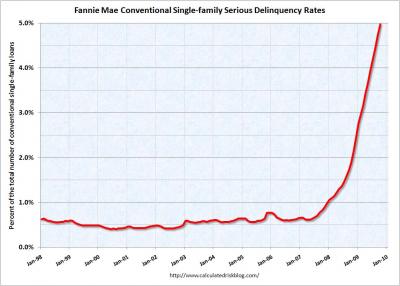

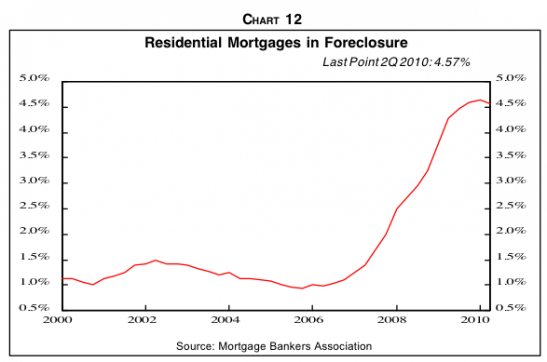

RESIDENTIAL REAL ESTATE - PHASE II

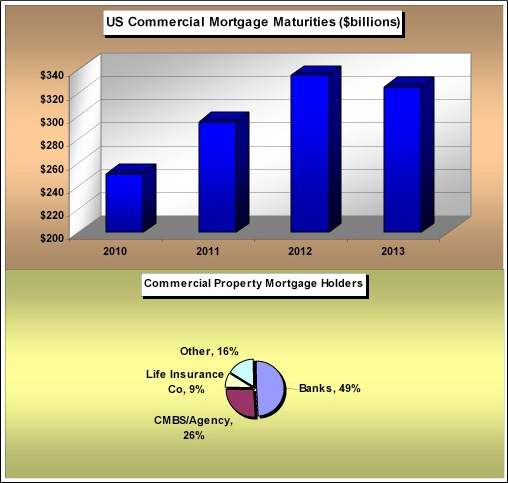

COMMERCIAL REAL ESTATE

2011 will see the largest magnitude of US bank commercial real estate mortgage maturities on record.

2012 should be a top tick record setter for bank CRE maturities looking both backward and forward over the half decade ahead at least.

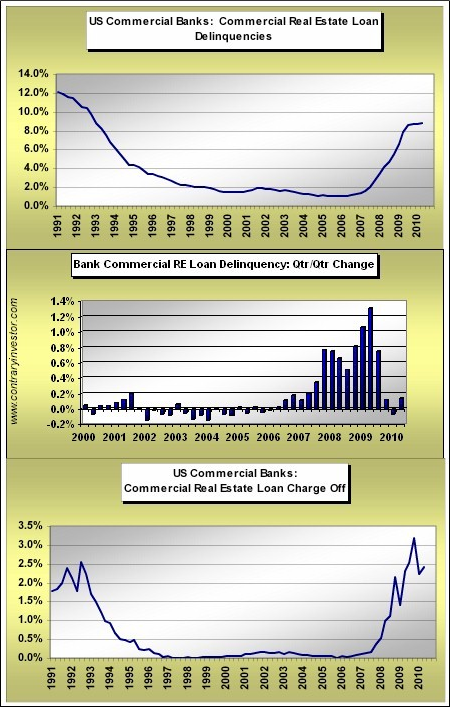

Will this be an issue for an industry that has been supporting reported earnings growth in part by reduced loan loss reserves over the recent past? In 2010, approximately $250 billion in commercial real estate mortgage maturities occurred. In the next three years we have four times that much paper coming due.

Will CRE woes, (published or unpublished) further restrain private sector credit creation ahead via the commercial banking conduit?

Wiil the regulators force the large banks to show any increase in loan impairment. Again, given the incredible political clout of the financial sector, I doubt it.

We have experienced one of the most robust corporate profit recoveries on record over the last half century. We know reported financial sector earnings are questionable at best, but the regulators will do absolutely nothing to change that.

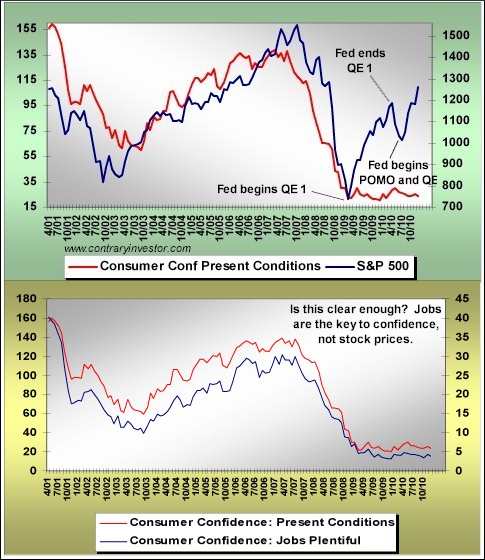

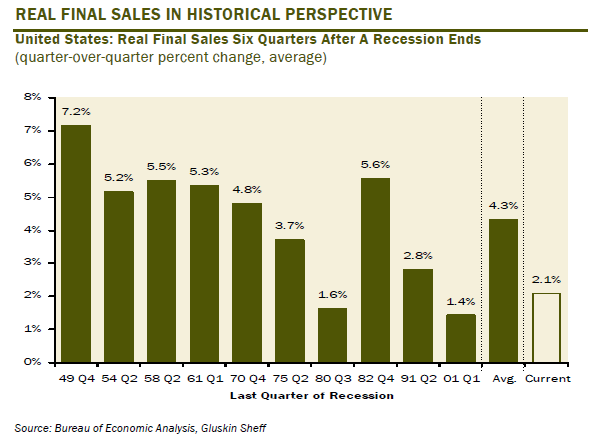

So once again we find ourselves in a period of Fed sponsored asset appreciation. The thought, of course, being that if stock prices levitate so will consumer confidence. Which, according to Mr. Bernanke will lead to increased spending and a virtuous circle of economic growth. Oh really? The final chart below tells us consumer confidence is not driven by higher stock prices, but by job growth.

CHRONIC UNEMPLOYMENT

Job Creation Pressures

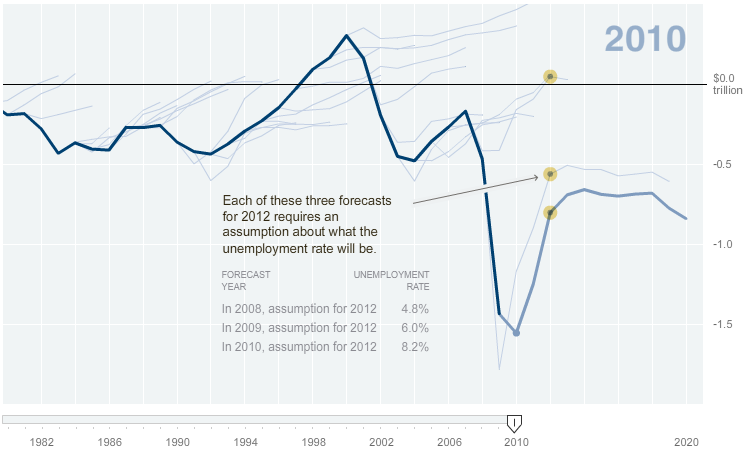

In case readers in western countries see the riots of the unemployed in North Africa and Middle East to be their problem, we might want to consider briefly the chronic unemployment in the US. If you examine the consistent and dramatic US budget forecasting misses, you see it is primarily associated with not correctly forecasting unemployment correctly. 2008 assumption for 2012 was 4.8%. In 2009 it was 6.0% for 2012. Now it is 8.2% for 2012. Want to bet it will be over 10% in 2012? These are the 'official' numbers. In reality US unemployment is between 17 - 23%.

It must be appreciated that many of the issues are not unique to the US.

The advent of IT networking, as witnessed through the Internet, has altered the way work is performed and the amount of labor required to support productive commerce in a monumental fashion.

Schumpeter's Creative Destruction has seen by orders of magnitude more jobs displaced than created.

The problem is the inability to recognize the Systemic Shift that is occurring and the inability of nations any longer to create jobs to match population growth.

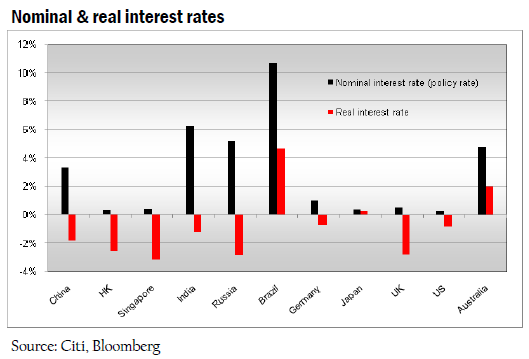

There are 3 major inflationary drivers underway.

1- Negative Real Interest Rates Worldwide - with policy makers' reluctant to let their currencies appreciate to market levels. If no-one can devalue against competing currencies then they must devalue against something else. That something is goods, services and assets.

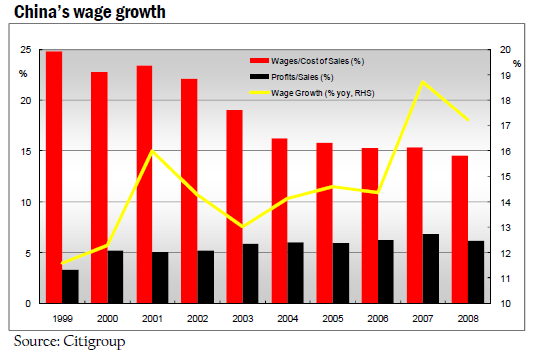

2- Structural Shift by China- to a) Hike Real Wages, b) Slowly appreciate the Currency and c) Increase Interest Rates.

3- Ongoing Corporate Restructuring and Consolidation - placing pricing power increasingly back in the hands of companies as opposed to the consumer.

FOOD PRICE PRESSURES

"Surging food and energy costs are stoking emerging-market inflation that’s serious enough to topple governments." - Nouriel Roubini

The United Nations reckons countries spent at least $1 trillion on food imports in 2010, with the poorest paying as much as 20 percent more than in 2009. These increases are just getting started. In January, world food prices rose to another record on higher dairy, sugar and grain costs. Unlike the food-price spike of 2008, this one may be more secular than cyclical. Asia alone, for example, will have another 140 million mouths to feed over the next four years. Add that to almost 3 billion people in the fast-growing region and you have a recipe for booming demand.

What’s killing households surviving on a few dollars a day is price volatility. If you spend almost half of your income to fill bellies, a 10 percent surge in cooking oil, wheat or chili peppers is devastating. It’s hard enough to pay rent and handle health-care costs today, never mind investing in education. Obviously, the poorer the country the bigger the percentage food is of disposable income. Food increases and volatility devastates the poor but it also cripples the middle class.

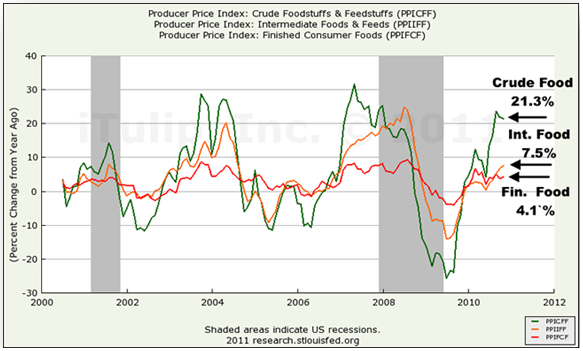

Eric Janzen at iTulip.com has an interesting chart which he explains in the context of the US middle class consumer: and QE II fallout. The costs of the Fed’s pro-inflation policies are largely born by the middle class. High food and gasoline prices, often dismissed by statisticians as too volatile to include in the CPI, are included in the producer price indexes, and the trend is clearly up. Food may only represent 16% of personal consumption expenditures (PCE) for US consumers as a whole, but 4.1% food price inflation, with 7.5% intermediate food price inflation in the pipeline, is a big deal for a family making $50,000 a year. That’s down 4% from $52,000 ten years ago.

The United Nations Food and Agriculture Organization (FAO) reported on March 3rd, 2011 that Global food prices rose for the eighth straight month in February. The FAO Food Price Index – a measure of basic food prices at the international level – averaged 236 points in February, up 2.2 per cent from January, the highest record in real and nominal terms, since the Rome-based agency started monitoring prices in 1990. The prices of all commodity groups monitored increased again last month, except for sugar, FAO noted in a news release.

Also, global cereal prices have increased sharply with export prices of major grains up at least 70 per cent from February 2010, owing to a decline in world cereal production last year and growing demand. The Cereal Price Index, which includes prices of main food staples such as wheat, rice and maize, rose by 3.7 per cent in February to 254 points – the highest level since July 2008. The FAO is forecasting global wheat production to rise by around 3 per cent this year if there is a recovery in major producers of the Commonwealth of Independent States.

In an article also published on March 3rd, the IMF commodities economists wrote that: “'The world may need to get used to higher food prices'. The economists said that a large part of the surge in food prices was related to temporary factors, such as the weather. “Nevertheless, the main reasons for rising demand for food reflect structural changes in the global economy that will not be reversed,” they added." Last week, the US Department of Agriculture forecast nominal record farm-gate prices for corn, wheat and soybeans in the crop year that begins with the 2011 harvests, predicting that the tightness in the markets would “not be entirely mitigated over the course of one or even two growing seasons”.

CBOT March corn futures on March 2nd touched a 2½-year high of $7.325 a bushel, up 95 per cent over the past 12 months and just 4 per cent lower than the all-time high of 2008. The FAO’s index of global food prices, which tracks the cost of cereals, oils, meat, dairy and sugar, has risen 40 per cent since June and is 5 per cent higher than its June 2008 peak, during the height of a global food crisis that sparked riots in countries from Egypt to Bangladesh.

In the IMF article, called “Rising prices on the menu”, the economists argued that the most important explanation for rising food prices was the changing diets of consumers in emerging economies. “Since the turn of the century, food prices have been rising steadily – except for declines during the global financial crisis in late 2008 and early 2009 – and this suggests that these increases are a trend and don’t just reflect temporary factors,” they said. “Policymakers – particularly in emerging and developing economies – will likely have to continue confronting the challenges posed by food prices that are both higher and more volatile than the world has been used to.”

Bloomberg recently reported that: "If you want to see how extreme the effects of surging food prices are becoming, look to wealthy Japan. So big are the increases that economists are buzzing about them pushing deflationary Japan toward inflation. Yes, rising costs for commodities such as wheat, corn and coffee might do what trillions of dollars of central-bank liquidity couldn’t. Yet the economic consequences of increasing food prices pale in comparison with the social ones. Nowhere could the fallout be greater than Asia, where a critical mass of those living on less than $2 a day reside. It might have major implications for Asia’s debt outlook. It may have even bigger ones for leaders hoping to keep the peace and avoid mass protests. What a difference a few months can make. Back in, say, October, the chatter was about Asia’s vulnerability to Wall Street’s woes. Now, governments in Jakarta, Manila and New Delhi are grappling with their own subprime crisis of sorts. This one reflects a toxic mix of suboptimal food stocks, exploding demand, wacky weather and zero interest rates around the globe. "

US STOCK MARKET VALUATIONS

WORLD ECONOMIC FORUM

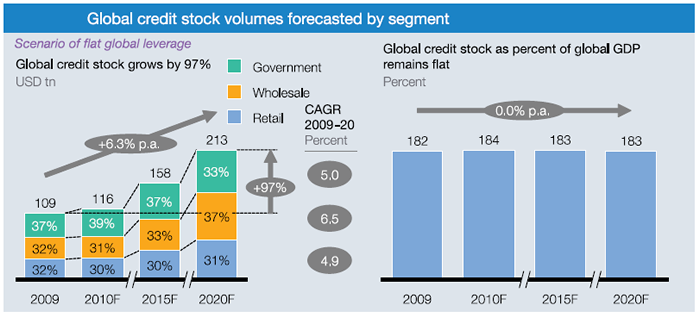

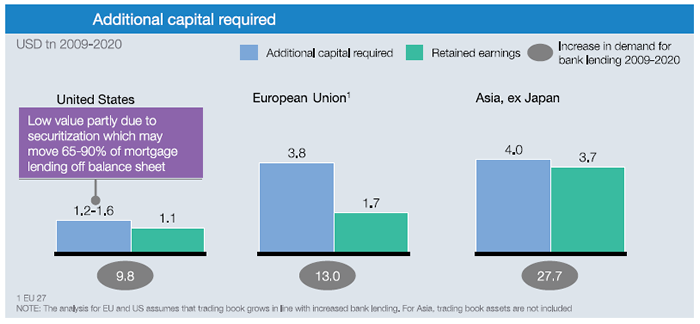

Potential credit demand to meet forecast economic growth to 2020

The study forecast the global stock of loans outstanding from 2010 to 2020, assuming a consensus projection of global

economic growth at 6.3% (nominal) per annum. Three scenarios of credit growth for 2009-2020 were modelled:

• Global leverage decrease. Global credit stock would grow at 5.5% per annum, reaching US$ 196 trillion in 2020. To

meet consensus economic growth under this scenario, equity would need to grow almost twice as fast as GDP.

• Global leverage increase. Global credit stock would grow at 6.6% per annum, reaching US$ 220 trillion in 2020.

Likely deleveraging in currently overheated segments militates against this scenario.

• Flat global leverage. Global credit stock would grow at 6.3% per annum to 2020, tracking GDP growth and reaching

US$ 213 trillion in 2020 – almost double the total in 2009. This scenario, which assumes that modest

deleveraging in developed markets will be offset by credit growth in developing markets, provides the primary credit

growth forecast used in this report.

Will credit growth be sufficient to meet demand?

Rapid growth of both capital markets and bank lending will be required to meet the increased demand for credit – and it is

not assured that either has the required capacity. There are four main challenges.

Low levels of financial development in countries with rapid credit demand growth. Future coldspots may result from the

fact that the highest expected credit demand growth is among countries with relatively low levels of financial access. In

many of these countries, a high proportion of the population is unbanked, and capital markets are relatively undeveloped.

Challenges in meeting new demand for bank lending. By 2020, some US$ 28 trillion of new bank lending will be

required in Asia, excluding Japan (a 265% increase from 2009 lending volumes) – nearly US$ 19 trillion of it in China

alone. The 27 EU countries will require US$ 13 trillion in new bank lending over this period, and the US close to US$

10 trillion. Increased bank lending will grow banks’ balance sheets, and regulators are likely to impose additional capital

requirements on both new and existing assets, creating an additional global capital requirement of around US$ 9 trillion

(Exhibit vi). While large parts of this additional requirement can be satisfied by retained earnings, a significant capital gap in

the system will remain, particularly in Europe.

The need to revitalize securitization markets. Without a revitalization of securitization markets in key markets, it is doubtful

that forecast credit growth is realizable. There is potential for securitization to recover: market participants surveyed by

McKinsey in 2009 expected the securitization market to return to around 50% of its pre-crisis volume within three years.

But to rebuild investor confidence, there will need to be increased price transparency, better data on collateral pools, and

better quality ratings.

The importance of cross-border financing. Asian savers will continue to fund Western consumers and governments:

China and Japan will have large net funding surpluses in 2020 (of US$ 8.5 trillion and US$ 5.7 trillion respectively), while

the US and other Western countries will have significant funding gaps. The implication is that financial systems must

remain global for economies to obtain the required refinancing; “financial protectionism” would lock up liquidity and stifle

growth.

US$ RESERVE CURRENCY

SocGen crafts strategy for China hard-landing

Société Générale fears China has lost control over its red-hot economy and risks lurching from boom to bust over the next year, with major ramifications for the rest of the world.

Société Générale said China's overheating may reach 'peak frenzy' in mid-2011

- The French bank has told clients to hedge against the danger of a blow-off spike in Chinese growth over coming months that will push commodity prices much higher, followed by a sudden reversal as China slams on the brakes. In a report entitled The Dragon which played with Fire, the bank's global team said China had carried out its own version of "quantitative easing", cranking up credit by 20 trillion (£1.9 trillion) or 50pc of GDP over the past two years.

- It has waited too long to drain excess stimulus. "Policy makers are already behind the curve. According to our Taylor Rule analysis, the tightening needed is about 250 basis points," said the report, by Alain Bokobza, Glenn Maguire and Wei Yao.

- The Politiburo may be tempted to put off hard decisions until the leadership transition in 2012 is safe. "The skew of risks is very much for an extended period of overheating, and therefore uncontained inflation," it said. Under the bank's "risk scenario" - a 30pc probability - inflation will hit 10pc by the summer. "This would cause tremendous pain and fuel widespread social discontent," and risks a "pernicious wage-price spiral".

- The bank said overheating may reach "peak frenzy" in mid-2011. Markets will then start to anticipate a hard-landing, which would see non-perfoming loans rise to 20pc (as in early 1990s) and a fall in bank shares of 50pc to 75pc over the following 12 months. "We think growth could slow to 5pc by early 2012, which would be a drama for China. It would be the first hard-landing since 1994 and would destabilise the global economy. It is not our central scenario, but if it happens: commodities won't like it; Asian equities won't like it; and emerging markets won't like it," said Mr Bokobza, head of global asset allocation. However, it may bring down bond yields and lead to better growth in Europe and the US, a mirror image of the recent outperformance by the BRICs (Brazil, Russia, India and China).

- Diana Choyleva from Lombard Street Research said the drop in headline inflation from 5.1pc to 4.6pc in December is meaningless because the regime has resorted to price controls on energy, water, food and other essentials. The regulators pick off those goods rising fastest. The index itself is rejigged, without disclosure. She said inflation is running at 7.6pc on a six-month annualised basis, and the sheer force of money creation will push it higher. "Until China engineers a more substantial tightening, core inflation is set to accelerate.

- The longer growth stays above trend, the worse the necessary downswing. China's violent cycle could be highly destabilising for the world." Charles Dumas, Lombard's global strategist, said the Chinese and emerging market boom may end the same way as the bubble in the 1990s. "The basic strategy of the go-go funds is wrong: they risk losing half their money like last time."

- Société Générale said runaway inflation in China will push gold higher yet, but "take profits before year end".

- The picture is more nuanced for food and industrial commodities. China accounts for 35pc of global use of base metals, 21pc of grains, and 10pc of crude oil. Prices will keep climbing under a soft-landing, a 70pc probability. A hard-landing will set off a "substantial reversal". Copper is "particularly exposed", and might slump from $9,600 a tonne to its average production cost near $4,000. Chinese real estate and energy equities will prosper under a soft-landing,

- The bank likes regional exposure through the Tokyo bourse, which is undervalued but poised to recover as Japan comes out of its deflation trap. If you fear a hard landing, avoid the whole gamut of Chinese equities. It will be clear enough by June which of these two outcomes is baked in the pie.

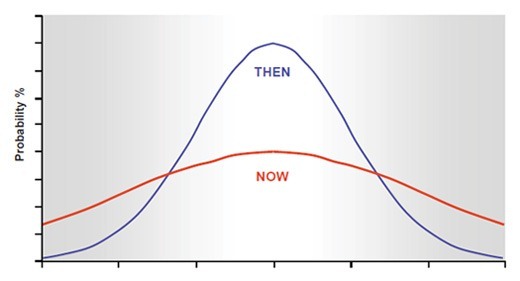

PIMCO'S NEW NORMAL: According to PIMCO, the coiners of the term, the new normal is also explained as an environment wherein “the snapshot for ‘consensus expectations’ has shifted: from traditional bell-shaped curves – with a high likelihood mean and thin tails (indicating most economists have similar expectations) – to a much flatter distribution of outcomes with fatter tails (where opinion is divided and expectations vary considerably).” That is to say, the distribution of forecasts has become more uniform (as per Exhibit 1).

The end of cheap oil, or more exactly of the indirect control of oil prices through the protection afforded to the oil monarchies, has apparently arrived.

In my concluding article to the Extend and Pretend series: Stage I Comes to an End! in July 2010, I warned of a US False Flag event specifically coming in the Middle East. As I see pictures of the massive amphibious assault ship USS Kearsarge now off the coast of Libya and headlines of a possible US invasion of Libya, I am reminded of what I wrote in July 2010.

"Looking forward, now that all of Europe is gripped in austerity, (and make no mistake - this very same austerity is coming to the US on very short notice with crashing popularity ratings for all political parties), has the political G-8/20 elite focused a little too much on a 'Falkland War'? Is war precisely the diversion that Europe and soon America hope to use in order to deflect anger from policies such as ....

Is there a Gallup or some other polling "unpopularity" threshold that the G-20 is waiting for before letting loose all those aircraft carriers recently parked [1] next to the Persian Gulf, the Israeli jets in Saudi Arabia [2] or the recent US troop buildup [3] on the Iran border? [4]"

Picture below: " Defense Secretary Gates just announced that two amphibious US assault ships were loaded and bound to Libya." - Business Insider

SOCIAL UNREAST

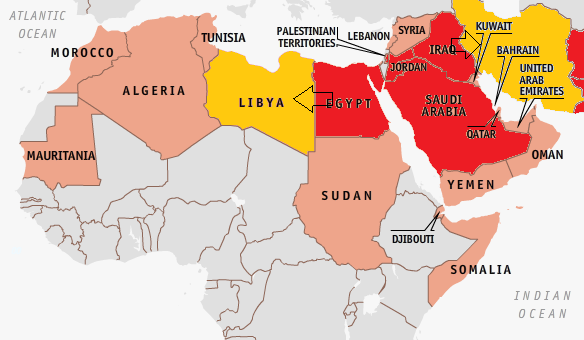

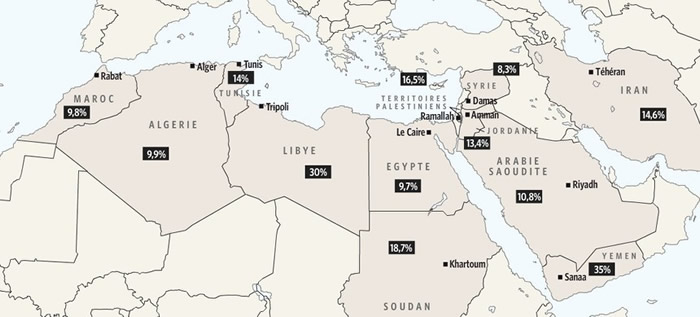

The map below from the Economist shows the members of the Arab League. Since Tunisians rose up and ejected their leader, Zine el-Abidine Ben Ali, who had ruled the country for 23 years, the scent of jasmine has spread through the Arab world. Egyptian protesters ousted their president, Hosni Mubarak, in just 18 days, after three decades under his rule. More recently Algeria, Libya, Yemen, Jordan, and Bahrain have all seen brave demonstrations by people fed up with being denied a voice and a vote. It gets worse and more violent each day.

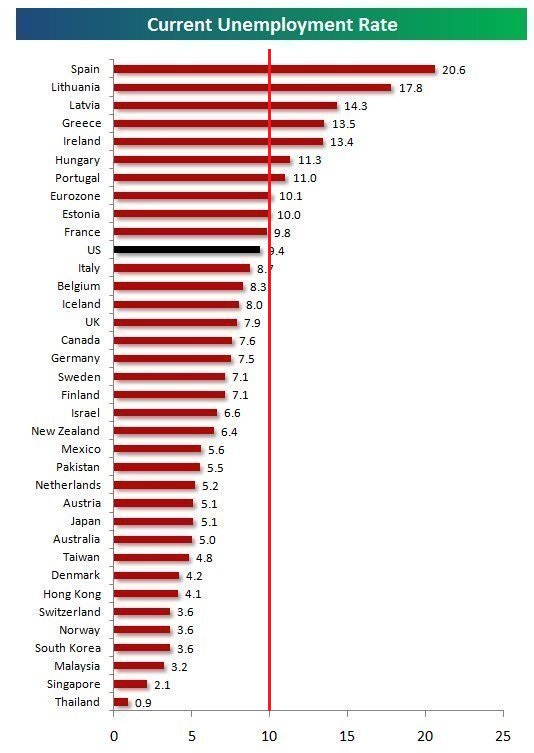

10% UNEMPLOYMENT THRESHOLD

Before we look below the headlines and media sound bites, it would be informative to step back and look at global unemployment rates. The chart below is based on the 'official' numbers as consolidated 01/2011by BMGBullion.

I have drawn a vertical line at 10% unemployment as a reference point. What is quickly evident is that:

1- Countries above 10% unemployment have experienced significant and well documented social unrest, primarily because of poor economic conditions.

2- Countries in the range of 10% are reporting sporadic events that show borderline indicators of social unrest.

3- Countries with low unemployment are politically stable with minimal social tensions.

What you will also notice from this chart is that not a single Arab League country is represented. This is possibly because of their smaller GDP levels.

I believe the root of the Arab problem is their relatively small GDP growth in relation to their growing populations.

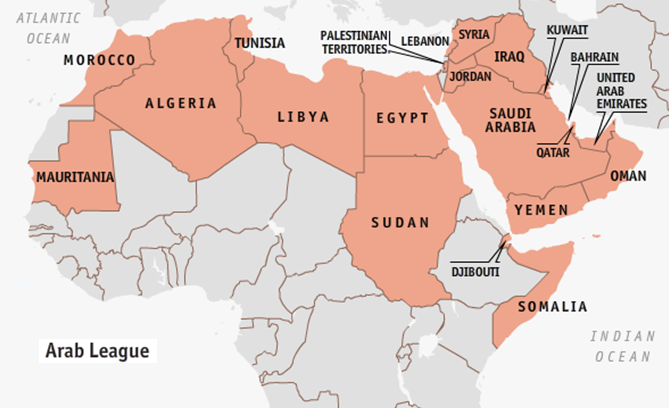

So what is the unemployment situation in the Arab League nations?

JOBS, FRUSTRATIONS & BEING ABLE TO EXIST

Frustrated and angry is the best way to describe the situation the above statistics foster - a situation ripe for a spark to set it off.

Forget the spin that every country wants to put on these protest events:

United States and EU: This is a pro-democracy movement!!!

Iran: This is an Islamic revolution!!

China: These are riots instigated by minorities!!!

Russia: This is a protest against America!!!

It is about being able to exist.

It is about unemployment, rising prices and the ability to make a person's life better for their family.

Call it social inequality, low personal income levels, corruption or whatever. None of this incites the masses until they are hungry, worried about their families' future and have nothing to lose.

As futurist Gerald Celente regularly says: "When people have nothing to lose, they lose it!"

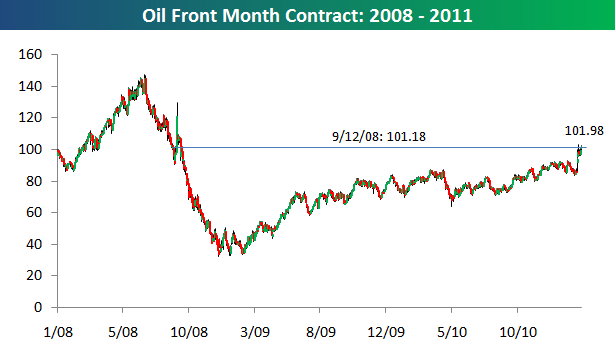

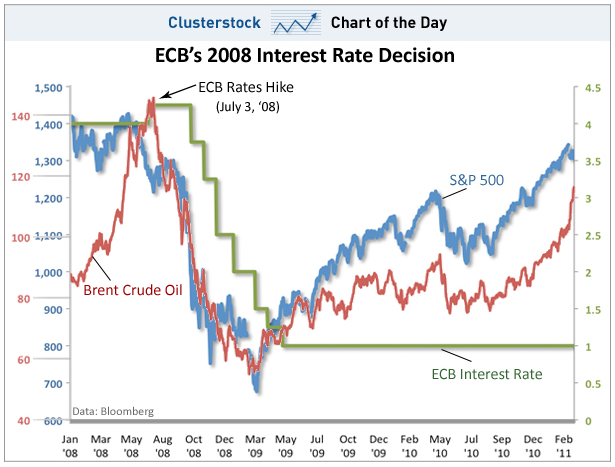

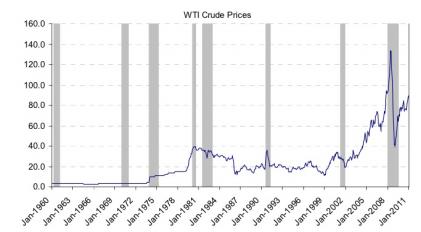

FAIT D'ACCOMPLI - Another Oil Shock?

Now that we are reeling - here comes the knockout punch!

Without exception, a significant increase in oil prices has precipitated a recession.

The solution has been to always reduce interest rates. This time rates are near zero

2015 THESIS: FIDUCIARY FAILURE

2015 THESIS: FIDUCIARY FAILURE