EXTEND

& PRETEND:

Shifting Risk to the Innocent.

Markets never repeat themselves but they often rhyme. This rally feels

like the same sonnet we experienced in 1987. As in a sonnet, it is

following a strict rhyme scheme and specific structure.

In 1987 the rally began gaining steam in the spring when it already seemed

overbought and extended. The rally had initially started in October 1986

at DOW 1400, but during the spring of 1987 it began to accelerate. It not

only didn�t correct, but continued to gain momentum. Despite all the

pundits saying it was about to correct, it just kept going up. By early

fall the bears had capitulated and the public was scrambling to avoid

missing further gains. They were quickly rewarded as the market moved even

higher. No bad news, overextended fundamentals or technical warnings

could stop the rise. The DOW was soon over 2700 for an approximate 93%

rise.

Then suddenly in October 1987, out of nowhere, the crash hit. It was

stunning. The market gave back 22.6% in one day. What was later

called Black Monday left a pale over the US that was palpable. In a matter

of days the market surrendered the entire gains it had achieved over the

previous year.

Before you

write me off too quickly as trying to draw too close a comparison, let me

tell you why it really feels the same. It isn�t just the rise or rhyme;

it�s the reason for both.

Since March 2009 the current rally has moved from a 666 low on the S & P

500 to a recent high of 1220, for an 83% increase in just over a year. The

rises are similar to 1987 but so are the critical elements of risk and how

risk has been shifted to the innocent. Before I discuss how this risk has

shifted through Dynamic Hedging, Capital Arbitrage and Regulatory

Arbitrage, let me first briefly talk about the realities of risk versus

perceptions.

REALITIES OF RISK

USING

STATISTICS TO SHOW US HOW THE INNOCENT GET LULLED INTO GETTING 'MUGGED'!

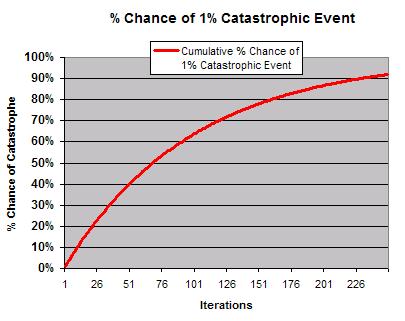

Let's say

there's a statistically unlikely event that takes place 1% of the time. As

an example, suppose, just for argument's sake, that if you go for a walk

in a particular Chicago neighborhood, statistically the police tell you,

1% of the time you will get mugged in this neighborhood.

So, if you

go out for a walk one time, you have a 99% chance of not getting mugged

and a 1% chance of getting hurt. But suppose you go out for one walk every

day for 10 days, the chance that you will get hit on one of those

occasions rises. The way it's calculated is by figuring the odds that the

LIKELY event will obtain at every single iteration and then subtracting

that from 100%. The equation is:

D

= 1-(1-P)^N

D

= 1-(1-P)^N

Where:

D=cumulative percentage chance of disaster

P= Percentage Chance of disaster on each opportunity (iteration)

N=number of iterations

So, if you

go out for 10 walks, your chance of getting into trouble is:

1-(1-.01)^10 = 9.6%.

And if you

go out for a walk every day for, say, 90 days, your chance of getting hurt

is

1-(1-.01)^90 = 59.5%.

The graph

above shows what the series looks like. (1)

And in

this scenario, if you go out for a walk every trading day of the year

(about 252 times) the odds are about 92% that you will meet your demise.

But the

funny thing about our human nature is that if, say, you went out for 252

walks in our Chicago neighborhood and came back 252 times, without having

had any violent encounters with our Chicago�s city folk, you would assume

that experience was teaching you that there was very little danger. Indeed

it might be, if you didn't already know the likelihood of getting mugged.

As human

beings we are especially primed to generalize from experience (that's

science), but most especially to generalize from our most recent

experiences (which is less reliable science--or anecdotal evidence). So,

the more walks we go on without getting mugged the less likely we FEEL it

to be that we will ever get mugged, irrespective of what statistics might

tell us. As our risk increases, statistically speaking, we feel safer

and safer.

We are all

familiar with the expression "tempting fate." One has to wonder if we

might be somewhere fairly far along on the curve charted above, feeling

safer and safer carrying all these economic loads, but with an ever

greater and greater chance of developing the incidence of one or another

severe, "dislocating," and "unlikely" event. (1)

LAW OF

COMPOUNDING NUMBERS

20% Gains

for 3 years then a 20% loss results in = 8.4% CAGR

20% Gains

for 3 years then a 35% loss results in = 2.9% CAGR

See the illusion?

Our government is doing us no favors with

an artificial extend and pretend strategy that makes us feel safer and

which consequentially starts the public spending and investing again.

Based on risk, it is both premature and dangerous to your financial

health.

DYNAMIC HEDGING

PORTFOLIO INSURANCE

When

the investigations were made by the government into the causes of the 1987

crash, it was discovered that it was primarily because of the wide

implementation of what was then called Portfolio Insurance. It was the

rage in the late 80�s as a way of removing risk from portfolios. At its

core, Portfolio Insurance involved trend following methodologies.

Consequentially, the more stocks moved up, the more your portfolio called

for more buying. It was self re-enforcing. It also worked in reverse and

consequentially the sudden crash. The investigations prompted the

introduction of circuit breakers into exchanges to limit downside moves in

any given period of time.

When

the investigations were made by the government into the causes of the 1987

crash, it was discovered that it was primarily because of the wide

implementation of what was then called Portfolio Insurance. It was the

rage in the late 80�s as a way of removing risk from portfolios. At its

core, Portfolio Insurance involved trend following methodologies.

Consequentially, the more stocks moved up, the more your portfolio called

for more buying. It was self re-enforcing. It also worked in reverse and

consequentially the sudden crash. The investigations prompted the

introduction of circuit breakers into exchanges to limit downside moves in

any given period of time.

SON-OF-PORTFOLIO INSURANCE

Though Portfolio lost its appeal after the 1987 crash, it was replaced by

what many at the time referred to as the son-of-portfolio insurance. It

was called Dynamic Hedging.

Dynamic hedging is a technique that is

widely used by

derivatives

dealers to

hedge

gamma

or

vega

exposures. Because it involves adjusting a hedge as the

underlier

moves�often several times a day�it is "dynamic. Dynamic hedging is

delta hedging of a non-linear position with

linear instruments like spot positions, futures or forwards.

The

deltas

of the non-linear position and linear hedge position offset, yielding a

zero delta overall. However, as the underlier's value moves up or down,

the delta of the non-linear position changes while that of the linear

hedge does not. The deltas no longer offset, so the linear hedge has to be

adjusted (increased or decreased) to restore the delta hedge. This

continual adjusting of the linear position to maintain a delta hedge is

called dynamic hedging. (2)

The

deltas

of the non-linear position and linear hedge position offset, yielding a

zero delta overall. However, as the underlier's value moves up or down,

the delta of the non-linear position changes while that of the linear

hedge does not. The deltas no longer offset, so the linear hedge has to be

adjusted (increased or decreased) to restore the delta hedge. This

continual adjusting of the linear position to maintain a delta hedge is

called dynamic hedging. (2)

Dynamic Hedging was a major contributor to the tech bubble run-up in the

late 1990�s, the 2002-2007 run-ups and the present rally. It is one of the

reasons this rally feels so similar and is being driven for similar

reasons. But there is more.

The risks are even greater today because Dynamic Hedging has allowed other

advancements to be layered on top of it.

With the post tech bubble crash in 2000 and the subsequent advent of the

housing bubble explosion from 2002 to 2007 we saw the emergence of Capital

Arbitrage.

CAPITAL ARBITRAGE

I am defining Capital Arbitrage here (as opposed to the slightly different

Regulatory Arbitrage) as the price difference in the cost of capital

through the reduction of risk via various methods including removing

debt obligations (risk) from the balance sheet. The price difference in

capital

costs is reflected in a lower interest coupon or basis point spread.

capital

costs is reflected in a lower interest coupon or basis point spread.

The advancements in securitization and financial engineering have allowed

this to happen in a dramatic fashion over the last decade.

Consequentially, the ability to extend credit prior to the financial

crisis was almost exponential in its growth - all of which was hedged

through Dynamic Hedging and through newer techniques such as Credit

Default Swaps (CDS). Capital arbitrage fostered yet another bubble until

the reversal once again happened and we had the expected explosive

momentum to the downside.

The table below is a simplified summary of a lot of the work outlined in

recent

Extend & Pretend series articles and the

Sultans of Swap series. It illustrates that almost all forms of

standard accounting practices & procedures have been circumvented through

modern Capital Arbitrage techniques. Whether Corporate accounting with its

cost /accrual structure, Financial and bank accounting with its reserve

and capital ratios or Government accounting with its cash account

accounting, it doesn�t matter, they have all been systematically

exploited.

There is only one goal, obscure debt

or financial obligations, commitments, guarantees or contingent

liabilities. This is to allow an improvement or maintenance in the cost of

capital and thereby allow further increases and gearing (leverage).

REGULATORY

ARBITRAGE

Today

we have layered yet another layer of risk onto the already existing

structure. It is called Regulatory Arbitrage.

Today

we have layered yet another layer of risk onto the already existing

structure. It is called Regulatory Arbitrage.

Regulatory arbitrage

is any transaction that has little or no economic impact on a financial

institution while either increasing its capital or decreasing its required

capital. Just as trading

arbitrage

identifies and exploits inconsistencies in market prices, regulatory

arbitrage identifies and exploits inconsistencies in capital regulations.

Regulatory arbitrage undermines the effectiveness of capital regulations.

It is one of the primary motivators for regulators to continually improve

capital requirements. (3)

This new strategy is again intended to remove risks but in this case you

are transferring it to a sovereign government in a number of fashions.

Whether debt or contingent liability obligations, the strategy involves

the sovereign government assuming responsibility and being forced to

create the credit to further the arbitrage.

It is highly sophisticated with many elements but like the previous

stages, it will end badly and likely violently. This time the probability

is that it ends when sovereign governments fail or are unable to attract

investors at satisfactory rates (i.e. Greece now having to pay over 9% on

10 Year Treasuries versus an expected 3.5%). Credit rating downgrades and

forced increases in collateral calls will be the catalyst. We are now

seeing just the tip of this iceberg throughout the southern European

countries (PIIGS).

�TOO BIG TO FAIL or are they TOO BIG TO SAVE?�

We have �saved� the following by the public assuming the liabilities after

all the profits were earned and distributed.

1.

Fannie Mae / Freddie Mac Agencies 1.5 - 2+T

2.

AIG 180B

3.

GM / GMAC 45B

4.

TARP � Banks 700B

5.

FDIC � Regional Banks ??

===

~ $3 Trillion

CONCLUSION

When markets stop functioning any algorithm breaks down.

Trading algorithms are based on certain fundamental assumptions that have

proven invalid over long

periods of time. The false assumptions include:

1.

Continuous market

liquidity

2.

Continuity of markets

3.

Counterparty Risk

The exposure these �discontinuities� create is well respected but to my

knowledge it is still not able to be modeled effectively. The trick

therefore is to make as much money as possible before �time� delivers the

proverbial �fat tail�. In layman�s language, as former Citigroup CEO

Charles Prince so famously quipped� it is a game of musical chairs and

�you must get up and dance while the music is playing�. If you don�t

�dance� your competitor will have the competitive advantage to be able to

use an improved stock price to take you out. It forces fiduciary risk

taking. As in a child�s game, it takes enforced rules or the cheating

begets cheating.

If the Legislators and Regulators won�t address excessive fiduciary risk

taking � then the market will in a violent and unexpected fashion - with

the innocent as the casualties.

Sign Up for the next release in the

Extend & Pretend series:

Commentary

SOURCES:

(1) John Hussman�s Analysis � (Unable to find link � noted it years ago

� sorry John)

(2)

Dynamic Hedging

� The Risk Glossary.com

(3)

Regulatory Arbitrage

� The Risk Glossary.com

The

last Extend & Pretend article:

EXTEND & PRETEND - Uncle Sam, You Sly Devil!

Gordon T Long

Tipping Points

Mr. Long is a former senior group executive with IBM & Motorola, a

principle in a high tech public start-up and founder of a private venture

capital fund. He is presently involved in private equity placements

internationally along with proprietary trading involving the development &

application of Chaos Theory and Mandelbrot Generator algorithms.

Gordon T Long is not a registered advisor and does not give investment

advice. His comments are an expression of opinion only and should not be

construed in any manner whatsoever as recommendations to buy or sell a

stock, option, future, bond, commodity or any other financial instrument

at any time. While he believes his statements to be true, they always

depend on the reliability of his own credible sources. Of course, he

recommends that you consult with a qualified investment advisor, one

licensed by appropriate regulatory agencies in your legal jurisdiction,

before making any investment decisions, and barring that, you are

encouraged to confirm the facts on your own before making important

investment commitments.

� Copyright 2010 Gordon T Long. The information herein was obtained from

sources which Mr. Long believes reliable, but he does not guarantee its

accuracy. None of the information, advertisements, website links, or any

opinions expressed constitutes a solicitation of the purchase or sale of

any securities or commodities. Please note that Mr. Long may already have

invested or may from time to time invest in securities that are

recommended or otherwise covered on this website. Mr. Long does not intend

to disclose the extent of any current holdings or future transactions with

respect to any particular security. You should consider this possibility

before investing in any security based upon statements and information

contained in any report, post, comment or recommendation you receive from

him.