SULTANS OF SWAP: Smoking Guns & the Sting!

There

are 7 stages to executing a successful sting operation. Whether this is

the modus operandi behind the Sultans of Swap operating in the $605

Trillion OTC Derivatives market or just simple coincidence, I will leave

it to you shrewd reader to determine. The seven stages do however

offer us an instructive theater guide to better understand these murky

instruments called Interest Rate Swaps.

There

are 7 stages to executing a successful sting operation. Whether this is

the modus operandi behind the Sultans of Swap operating in the $605

Trillion OTC Derivatives market or just simple coincidence, I will leave

it to you shrewd reader to determine. The seven stages do however

offer us an instructive theater guide to better understand these murky

instruments called Interest Rate Swaps.

For our

younger readers The Sting

is a 1973 American movie set in September 1936 (an era not too

dissimilar economically to present day) that involves a complicated

plot by two professional

grifters

(Paul Newman and Robert Redford) to con a mob boss Robert Shaw. The story

was inspired by real-life con games documented in �The Big Con: The

Story of the Confidence Man�. (Not to be confused with �The

Confidence Game� by Stephen Solomon documenting today�s Global Central

Banking structure and our own Federal Reserve).

The title phrase refers to the moment when a con artist finishes the

"play" and takes the

mark's

money. If a con game is successful, the mark does not realize he has been

"taken" (cheated), at least not until the con men are long gone

(Wikipedia)

The 7 steps of a successful Sting normally occur in 3 stages which we will

distinguish as Acts in today�s modern �play�. Now that you understand the

plot line, sit back, tightly hold onto your wallet and enjoy the �play�.

ACT I - SMOKING GUNS

Usually a caper or heist film will contain a

three-act plot. The first act usually

consists of the preparations for the heist: gathering conspirators,

learning about the layout of the location to be robbed, learning about

the alarm system, revealing innovative technologies to be used, and,

most importantly, setting up the plot twists in the final act. (Wikipedia)

1

-THE PLAYERS

1

-THE PLAYERS

Like any play we first need to introduce the actors. Who exactly are the

Sultans of Swap who play the $437 Trillion global Interest Rate Swap game?

There are many actors involved, all with their own motivations and sub

plots. We should pay close attention because like any good mystery the

answers are unravelled in the multitude of sub plots all happening

concurrently.

-

THE PATSY: The Counterparties A & B (shown to the right in a simple

interest rate swap structure) actually hold the OTC (Over-the-Counter)

contracts. We will refer to them as the �PATSY� or �PATSIES�. Like all

PATSIES they have an angle and think they are smarter than most. They have

just enough knowledge to be dangerous.

-

THE ACCOUNTANTS:

These are the third parties that administer the ongoing interest payment

stream exchanges. We include here also the major global law firms making

daunting fees for contract writing and consultation. We will refer to them

as a group called �THE ACCOUNTANTS�.

-

THE SPECULATORS:

These are the issuers and holders of CDS�s that protect against or

speculate on counterparty failure of the interest rate swap contract OR

the PATSY specifically. We will refer to them as �SPECULATORS�. It needs

to be fully understood that our SPECULATORS engage in naked shorting of

CDS�s in an unregulated OTC where no DTCC exists that acts as a matching

inventory custodian. Our SPECULATORS appear as sinister looking characters

in our fictional play.

-

THE PRODUCERS:

These are the magicians that put the OTC contract together, take a quick

fee and rapidly leave the scene in Act I as an apparent supporting actor.

We could call them the �magicians� but we will call them the PRODUCERS after the Broadway play

by the same name and possibly with similar motivations. You may recall

that the 2005 movie �The Producers� was

about two producers pulling a sting where they intentionally produced a

play expecting and planning for its failure. The TAKE was in the

failure. Broadway is only uptown from Wall Street and in the center of the

mid town Investment Banking crowd. Like a chicken & egg it is hard to tell

which was devised first � the evening theater entertainment or their daily

enterprising activities. (Note: We need to carefully watch the sub

plot of the PRODUCERS unfolding or we won�t see the sting coming).

after the Broadway play

by the same name and possibly with similar motivations. You may recall

that the 2005 movie �The Producers� was

about two producers pulling a sting where they intentionally produced a

play expecting and planning for its failure. The TAKE was in the

failure. Broadway is only uptown from Wall Street and in the center of the

mid town Investment Banking crowd. Like a chicken & egg it is hard to tell

which was devised first � the evening theater entertainment or their daily

enterprising activities. (Note: We need to carefully watch the sub

plot of the PRODUCERS unfolding or we won�t see the sting coming).

-

THE CON MEN:

These are the �Confidence Men� or �CONS� for short. Their role is make our

PATSIES feel confident. These are the Credit Rating Agencies who have

starred in previous plays (i.e. the Toxic Asset ratings associated with

the financial crisis) once again doing their mysterious and well

disclaimed ratings. In our play they are rating both the credit worthiness

of either PATSY and even the SPC (Structured Private Company) involved in

certain Sovereign Interest Rate Swaps (more on that later). Their

role allows either PATSY to feel comfortable that the other PATSY can pay

(we need to immediately recognize the difference between operative

words: can and will).

-

THE DIRECTORS: These are the SEC, CFTC & corresponding

international regulatory authorities. This group additionally includes

Legislative authorities such as the US House Financial Services Committee

and the US Senate Banking Committee that somehow are always overlooked but

are senior DIRECTORS in this play. All the DIRECTORS in our fictional play

are dressed as sleepy eyed police officers with little to no interest in

the shenanigans of the other actors throughout all three acts. The

DIRECTORS are seen to react to telephone calls that occur throughout our

play where there is a brief flurry of disorganized and short lived

attention. They are then seen to supervise the fallout of some exploding

financial event, before just as quickly returning to their ongoing siesta.

-

THE BANKSTERS:

These are the international banks making obscene fees and trading charges.

We are talking $35B in 2009 trading fees alone (6) for brokering these

swaps from parties desperate to re-align contract bets since the financial

tsunami arrived. We

will call them the �BANKSTERS�.

As in any mystery thriller the sub plots can make a simple story appear

more complex than it really is. We need to remember what the old carnival

�3 shells & a pea� game teaches - it is a sleight of hand & deception that

allows the trick to work.

Enter stage left our PRODUCERS and PATSIES.

2- THE

SET-UP

The

Set-Up must achieve two objectives: Establish the NEED and create

CONFIDENCE.

The

Set-Up must achieve two objectives: Establish the NEED and create

CONFIDENCE.

THE NEED

� Debt

Addiction

The ideal

need is one that is addictive. Drugs, Alcohol and Tobacco are three of the

clearer examples. Like pushers conning children into using drugs for the

first time, the PRODUCERS must convince the PATSIES there is no danger.

Everyone is doing it and it will make life better.

Our

addiction of choice in this sting is Debt. Whether Consumer, Corporate or

Sovereign Debt, western economies have become addicts over the last 30

years � there can be little disputing this fact. It did not happen by

chance. To those trafficking in debt the Holy Grail is Sovereign debt.

This is due to both its size and its ability to guarantee debt payments

based on a legal authority to tax. It has the law and enforcement powers

behind it.

John

Perkins has authored a series of books from �Confessions of an Economic

Hit Man� in 2004 to �Hoodwinked� in 2009, laying out his

personal involvement in intentionally establishing false economic

justifications for large sovereign infrastructure projects around the

globe. Whether you believe his assertions that it was at the behest of

elements within the US government, we can clearly see is he was up front

and involved in perpetrating the plans & justifications upon which

governments in third world countries could secure massive levels of debt

based on fraudulent economic justifications. Even those who weren�t

addicted because they didn�t have the ability to borrow were drawn into

the game by agents that would free foreign leaders from debt constraint.

Debt obligations through the hands of these pushers quickly flowed like

drugs to an addict and liquor to an alcoholic.

In

more developed countries with legacy social entitlement programs we are

seeing massive social entitlements continuing to only get larger, more

generous and more underfunded. None is more obvious than in Greece,

Portugal, Italy, Spain (PIGS) and across Western & Eastern Europe

where the unquenchable thirst for more debt has reached the terminal stage

that all substance abusers will eventually find them if all restrictions

to drugs (lending) are removed.

In

more developed countries with legacy social entitlement programs we are

seeing massive social entitlements continuing to only get larger, more

generous and more underfunded. None is more obvious than in Greece,

Portugal, Italy, Spain (PIGS) and across Western & Eastern Europe

where the unquenchable thirst for more debt has reached the terminal stage

that all substance abusers will eventually find them if all restrictions

to drugs (lending) are removed.

Enter

stage right the CON MEN to join the others on the stage.

CREATING

CONFIDENCE

� The

�AAA�

In �The

Swaps that Swallowed Your Town�, the New York Times on 03-05-10

illustrated how Interest Rate Swaps were shrewdly peddled to US

municipalities, school districts, sewer systems and other tax-exempt debt

issuers. In this world of the intersection of Derivatives and Municipal

debt financing, the sales pitch they report �(the peddlers)

accentuated the positives in them. �Derivative products are unique in the

history of financial innovation,� gushed a pitch from

Citigroup

in November 2007 about a deal entered into by the Florida Keys Aqueduct

Authority. Another selling point: �Swaps have become widely accepted by

the rating agencies as an appropriate financial tool.� And, the

presentation said, �they can be easily unwound�

(1).

The ratings agencies were at the center of the collapse in the

mortgage securitization collapse because of the perceptions that the

rating agencies rated CDO (Collateralized Debt Obligations) and all the

other toxic waste as AAA. In the interest rate swap play the credit rating

agencies rate the sovereign debt based on what the balance sheet shows

them. They would likely argue that even if they are fully aware of off

balance sheet activities their duties are to appraise only what is before

them, what the accounting standards of a particular sovereign outlines and

specifically how those standards interpret �contingent liabilities�. (More

on this subject as our play unfolds). Armed with the newly arrived CON

MAN�s credit rating on both PATSIES, with the assurances of the PRODUCERS,

and with the help of the now present ACCOUNTANTS, our PATSIES feel

confident that risks are manageable based on everything they have heard

from the experts present on stage.

3-

THE HOOK

3-

THE HOOK

The hook

is about the Timing and Rationalization of the Sting.

The

BANKSTERS join the large crowd of actors now performing complex magical

acts before the PATSIES on stage.

Like any

addiction it takes an event to initiate the addiction. The event delivers

both Timing & Rationalization.

Whether it

is a third world leader clinging to power by offering expensive populist

solutions, declining revenue bases due to failing industrial policy,

geo-political defense requirements, a natural disaster, economic

strategies like Dubai�s opulent extravagances or membership in the

European Union with its Maastricht Agreement requirements etc, etc., these

are the justifications, excuses or motivations for the loan and expanding

debt.

This list

and endlessly more justifications have always existed. Getting the money

historically has been the constraining element. No more constraints thanks

to our Sultans of Swap.

4- THE

TALE

The Tale

is the presentation of the OFFER.

With all

our actors seated at the table in the center of the stage we hear the

quiet whispers as the plan is secretly divulged.

From the

endless list of timing & rationalizations we will select just one to

overhear in our fictional play which is garnering a lot of investor &

media attention � The European Union Experiment.

According

to the Maastricht Agreement and the EU

Stability & Growth Pact (SGP) a condition of entry and ongoing membership

is the adherence to fiscal deficits of no more than 3% of GDP and total

debt of no more than 60% of GDP. It is now emerging that members were

creative in their accounting to facilitate membership, and then even more

creative to allow for existing debt compounding and the increases due to

additional populist programs.

The audience tentatively listens as the whispered plans are unveiled:

GREECE

GREECE

We form a PPP (Public Private Partnership) under the direction of a PPI

(Public Private Initiative). We form a SPC (Special Purpose Company).

Through the contractual use of a legal opus magnum called a Novation

Agreement the Greek government exchanges fixed interest streams for

floating interest rate streams and in so doing receives cash up front with

a bubble payment at the termination of the Interest Swap Agreement.

Presto, we have an off balance sheet debt without any impact to Greece�s

sovereign debt rating. It is much more involved than this and I therefore

refer you to:

SULTANS OF SWAP: Explaining $605 Trillion in Derivatives!

and

SULTANS OF SWAP: Fearing the Gearing!

which outlines this structure as specifically applied at Kitlos PLC

(SPC) in Greece.

Reggie Middleton at the

BoomBustBlog.com has done some truly tenacious

digging and has unearthed the following further smoking guns:

�According

to people familiar with the matter interviewed by

China Securities Journal, Goldman Sachs Group Inc. did as many as 12

swaps for Greece from 1998 to 2001, while Credit Suisse was also involved

with Athens, crafting a currency swap for Greece in the same time frame.

Under its "off-market" swap in 2001, Goldman agreed to convert yen and

dollars into euros at an artificially favorable rate in the future. This

helped Greece to use that "low favorable rate" when it recorded its debt

in the European accounts-pushing down the country's reported debt load.

Moreover,

in exchange for the good deal on rates,

Greece had to pay Goldman (the amount wasn't revealed).

And since the payment would count against

Greece's deficit, Goldman and Greece came up with another twist: Goldman

effectively loaned Greece the money for the payment, and Greece repaid

that loan over time.

And the

two sides structured the loan as another kind of swap. So, the deal didn't

add to Greece's debt under EU rules. Consequently,

Greece's total debt as a percentage of GDP fell from 105.3% to 103.7%, and

its 2001 deficit was reduced by a tenth of a percentage point in GDP

terms, according to people close to Goldman�. (2)

ITALY

�As discussed in a recent

ZeroHedge article, a 1996 Italian currency swap, arranged by J.P.

Morgan, allowed Italy to receive large payments upfront that helped keep

its deficit in line, with the downside of greater payments later. In

addition, to curbing their current deficits, countries are now using these

swap agreements to push off their loan liabilities (related to swap

agreements) to a later date through securitization, and Greece is one such

example.

Under the 2001 deal brokered by Goldman, Greece swapped dollar and

yen-denominated debt for Euros at below-market exchange rates. The result

was that the country got paid �1 billion ($1.35 billion) upfront on the

swap in exchange for an obligation to buy the swaps back later. In 2005,

this obligation was in turn securitized as part of a 20-year debt issue,

further pushing off the day of reckoning.

Moreover, one of the key reasons why such manipulations continued is the

apparent ignorance of the EU's Eurostat, which knew enough about these

deals to tighten the rules governing their accounting-albeit only after

they had served their purpose - the Ponzi! When Italy's then-Prime

Minister Romano Prodi miraculously achieved a four-percentage-point

improvement in Italy's budget deficit in time to usher the country into

the common currency, Italy's use of accounting gimmicks was widely

discussed, and then promptly ignored. As at that time, everyone was only

too eager to look the other way in the drive to get the single currency up

and running.

It wasn't until 2008, a decade after the deals became popular, that

Eurostat was able to revise its rules to push countries to include swaps

in their debt and deficit calculations. Still, todate too little is known

about countries' continued exposure to the deals that are already out

there.

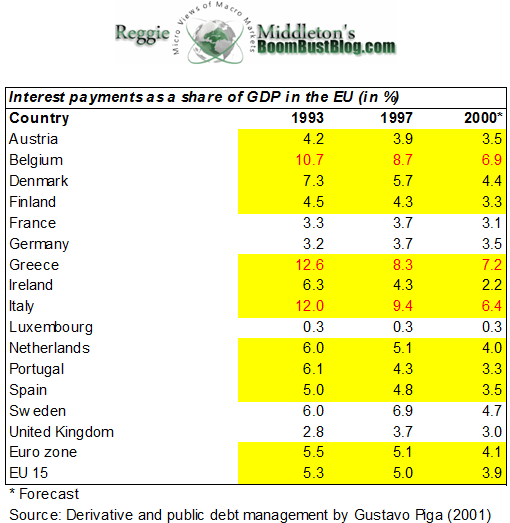

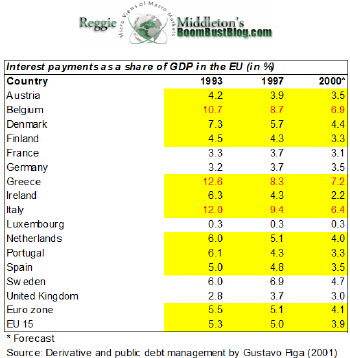

Overall,

though there is less evidence to support that there are more such swap

deals that happened during the late 90's until early part of this decade,

the data to the right showing a sharp decline in interest payments as a

percentage of GDP particularly for Belgium (apart from Greece and Italy),

hints that there are considerably more of these deals to be discovered.

The question is, will they be discovered before or after the respective

sovereign issues record debt to the

Overall,

though there is less evidence to support that there are more such swap

deals that happened during the late 90's until early part of this decade,

the data to the right showing a sharp decline in interest payments as a

percentage of GDP particularly for Belgium (apart from Greece and Italy),

hints that there are considerably more of these deals to be discovered.

The question is, will they be discovered before or after the respective

sovereign issues record debt to the suckers sovereign fixed income

investors.

Notice the extremely supercalifragilisticexpealidocious reductions

Belgium, Greece and Italy have made in their interest payments from 1993

to 2000 in this graphic made pre-2000. If one didn't know better, one

would have thought these countries actually used magic to make such

reductions. Italy practically cut their debt service (projected, of

course) in half. It really makes one wonder. I'm just saying...

According to DERIVATIVES AND PUBLIC DEBT MANAGEMENT by

Gustavo Piga, "The political stakes of the 1997 budget package

were enormous. Therefore, it was no surprise that many countries were

accused of �creative window-dressing' in their budget through the use of

accounting tricks to reach the desired goal. One contentious item was

interest expenditure, which is the interest expense that governments

sustain to finance their deficit and roll over their debt. Interest

expenditure represents a high percentage of public spending and GDP in the

European Union. It is highly variable over time, especially when compared

to other components of the budget. Because of its relevance and because it

is subject only to minimal scrutiny during budget law discussions (and

many times even after its realization during the fiscal year), interest

expenditure is an ideal target for reaching fiscal stabilization goals

without incurring excessive political protest or opposition". (2)

Reuters leaves little to speculation when it reported on March 11, 2010

Forget Greece:

Italy Derivatives Bomb also ticking

Many

local governments eager to cut financing costs for years rushed to sign

up for complex derivatives contracts, even when the terms were in

English. But some cities, facing big losses when interest rates go up,

are now trying to pull out of derivatives and suing the international

and local banks that arranged the deals.

In a

test case, a judge in Milan will decide in coming weeks whether to try

13 people and four banks -- UBS (UBSN.VX),

Deutsche Bank (DBKGn.DE),

Germany's Depfa and JPMorgan Chase & Co (JPM.N)

-- on aggravated fraud charges. The case stems from a derivatives swap

over a 1.68 billion euro ($2.28 billion) 30-year bond, the biggest

issued by an Italian city.

Milan,

Italy's financial capital, is facing a 100 million euro loss on the

deal, city officials say. Milan is also suing the banks for 239 million

euros in overall liabilities.

In the

southern region of Puglia, prosecutors are seeking to bar Merrill Lynch,

a unit of Bank of America Corp (BAC.N),

from government contracts for two years. The move stems from derivatives

losses from 870 million euros in regional bonds.

JPMorgan, UBS and Deutsche have denied wrongdoing, and Depfa has

declined comment. Merrill has not commented.

MAKE THE

SWITCH

Almost

500 small and large Italian cities are facing mark-to-market losses of

2.5 billion euros on the contracts, according to the Bank of Italy.

Analysts say that figure will balloon when interest rates go up. Most of

the contracts involved switching fixed rates on loans to variable ones

with banks.

"With

the economic crisis, the problem has been lessened a bit (with lower

rates) ... But in fact with a rate rise it becomes an even worse

problem," said Fabio Amatucci, an expert on local government

finances at Milan's Bocconi University.

The

European Central Bank is expected to start hiking rates at the end of

this year or early next year.

U.S. and

European officials are looking into how U.S. investment bank Goldman

Sachs Group Inc (GS.N)

may have helped Greece disguise the size of its budget deficit through

the use of cross-currency derivatives in 2001.

The

Italian deals differ somewhat from the Greek case since the instruments

were usually for switching rates on loans, but Italy stands out because

of the vast number of cities, regions and public entities -- even a

theater association -- that turned to them from 2001 to 2008.

The Bank

of Italy put the notional value of derivatives contracts at 24.1 billion

euros in June 2009. However, Il Sole 24 Ore business newspaper on

Thursday cited Treasury data to put the overall figure at 35.5 billion

euros -- a third of local governments' debt -- when wider

criteria were used.

Although

central bank figures show 467 local governments had derivatives

contracts at the end of September, Amatucci believes the real number

could be around 3,000 as more deals emerge.

The

government banned new contracts in 2008 pending new rules. Economy

Minister Giulio Tremonti has said there is "no effect" from derivatives

held by local governments.

LOOSEN

UP

Local

governments rushed into derivatives in part because they helped ease the

rigidity of a 2001 law that bars taking on new debt except to finance

investment.

But another

big draw was the upfront payment many cities got in advance for signing

revamped agreements, usually done without a bidding process,

analysts said.

Renegotiated deals shoved back payment and costs in a "political

manipulation" of signings, said Giampaolo Gialazzo with the Tiche

consultancy in Treviso.

Revised

deals also carried increasingly restrictive terms and higher costs

for municipalities and other local governments.

"Greece

did nothing more than get itself money right away and then pay it back

slowly. Local administrations in Italy did the same thing," said

Massimiliano Palumbaro with CFI Advisors in Pescara. Pescara, a southern

Italian city, itself took out a total of 108 million euros in interest

rate swaps and is suing UniCredit SpA (CRDI.MI)

and BNL, a unit of France's BNP Paribas (BNPP.PA),

over them. UniCredit had no comment, while BNL had no immediate comment.

When

rates are low, as they were when many contracts were agreed, local

authorities using a variable rate could find their costs shrinking.

However, when rates rose, officials would find themselves owing more

money.

Milan

has argued, as have many other local administrations, that the contracts

were murky, carried hidden costs and banks had failed to explain them.

However,

a source close to the issue said Milan could not argue that it was

ignorant about derivatives since the 2005 swap replaced a contract that

had been renegotiated repeatedly.

The city

also has wide securities markets experience given its joint control of

listed utility A2A (A2.MI),

the source said.

With

banks putting in place a complex deal that had to be overseen for 30

years with hefty back-office costs, "the city could not expect that the

banks were going to take that position for free," said the source.

Despite

the court cases, Milan is still interested in derivatives. The city

council said on Wednesday it was studying a switch from a variable rate

on the contract to a fixed one.

PORTUGAL

�Portugal

has also been known for years to take advantage of derivatives contracts

to dress up its budget numbers in the late 1990s.

In a recent press article (Debt

Deals Haunt Europe) Deutsche Bank's spokesman Roland Weichert

commented that the bank has executed currency swaps on behalf of Portugal

between 1998 and 2003. He also said that Deutsche Bank's business with

Portugal included "completely normal currency swaps" and other business

activity, which he declined to discuss in detail. He also added that the

currency swaps on behalf of Portugal were within the "framework of

sovereign-debt management," and the trades weren't intended to hide

Portugal's national debt position (yeah okay!). Though the Portuguese

finance ministry declined to comment on whether Portugal has used currency

swaps such as those used by Greece, They said Portugal only uses financial

instruments that comply with European Union rules.� (3) The Portugal

comment begs the whole issue of �Framework of Sovereign Debt Management �.

What it is and how exactly it aligns with standard international

accounting practices as it relates specifically to �contingent

liabilities� � but we digress and will return to this briefly.

We could go from Spain to France and other EU countries operating under

the Eurostat framework guidelines and see the same thing. We could discuss

the Millennium Dome Project in the UK. We could discuss Dubai World and

the hidden amount of debt recently discovered (and still being

discovered), but let�s skip over the pond to the USA to see if this is

just an isolated European �TALE� being told.

US - NY STATE MUNICIPALS

In The

Swaps That Swallowed Your Town the New York Times shows that

there is widespread use of Interest Rates swaps across US Municipalities

with extremely negative consequences now showing up that were not

understood when the PRODUCERS and BANKSTERS made their presentations.

Though I failed to see clear proof in their examples of the adoption of

the Novation agreement being used in Europe, this doesn�t necessarily mean

it is not being used or there is a derivation being employed in the US.

What I found interesting was that the CEO of an advisory firm on this

subject is quoted as saying �We need transparency where Wall Street

discloses not only the risks but also calculates the potential costs

associated with those risks. If you just ask issuers to disclose, even in

a footnote, the maximum possible loss or gain from the swap, they probably

wouldn�t do it.� (1) The audience must surely notice that the DIRECTORS

in our play are now completely asleep on stage though another frustrated

call is heard from Harry Markopolos over the stage loud speaker.

And here ladies and gentleman � watch closely � we have the sleight of

hand mentioned earlier.

Everything is aimed at getting debt off the balance sheet. Whether through

SPE (Special Purpose Entities) of various descriptions or conduits such as

SIV (Structured Investment Vehicle) the shell game is all about avoiding

the �d� word or Debt.

A LOAN is a debt and must be accounted as A LIABILITY.

A GUARANTEE is not a loan! It is a CONTINGENT Liability.

A Guarantee is something that accountants refer to as a �contingent

liability�. The operative word here is �contingent�.

This quickly gets extremely tricky to quantify in its simplest form

without adding the complexity of layers of structures and parties around

it. It becomes a game of assessed probabilities. The results of the

probabilities determine the amount of contingent liabilities to be accrued

as a debt liability. Then there is the question of timing. What event

might trigger this and when should the liability treatment be reflected.

As

an illustrative example, what were the chances of housing correcting 15%

when we hadn�t seen housing go down in neither our lifetime or our

possibly our parents? Many considered it unlikely and therefore either

minimal or no contingencies were allowed.

As

an illustrative example, what were the chances of housing correcting 15%

when we hadn�t seen housing go down in neither our lifetime or our

possibly our parents? Many considered it unlikely and therefore either

minimal or no contingencies were allowed.

Add to this confusion a slew of accounting standards with various

interpretations and rulings (ias

37 contingent liabilities,

ifrs contingent liabilities

,

fasb contingent liability,

us gaap contingent liabilities,

Government Accounting Standards

Advisory Board,

contingent liabilities disclosure etc.) and you end up in very

murky waters - Waters not too dissimilar to those associated with toxic

assets in the financial crisis where it was nearly impossible to value

Level 1 bank Capital Ratios � Mark-to-Market was Mark-to-Model or more

aptly Mark-to-Myth. This is the same problem with a slightly different

twist. There is the same consistent concern about debt appearing on an

asset / liability ledger.

5- THE

WIRE

The bookie

operation was a wire service in the movie �The Sting� and it was central

in pulling off the story�s heist. In our play we have an electronic wire

service but it runs between the BANKSTERS and some of the PRODUCERS. It is

called the OTC or Over-the-Counter trading. This is how all $605 Trillion

Derivatives, including $437 Trillion in Interest Rate Swaps, are traded.

No regulations. No standards. No supervision. No audits. They are

completely private, restricted and proprietary. There is no sheriff or

watch dog. It is the Wild West without a sheriff in town. The boys can

shoot it up all they want. Similar to the DTC & Naked Shorting, Dark

Pools, High Frequency Trading etc., it is ripe for creative enterprise.

Just the kind of secrecy I believe people serving time at �Sing-Sing� like

things.

If you

thought the play was getting complicated when we discussed the Novation

agreement and assessing Contingent Liabilities, let�s add the twist that

all these private contracts are traded. The poor auditors must have their

heads spinning. Which auditor in which country you astutely ask? As Johnny

Depp famously drawls in the mob crime flick �Donnie Brasco� to

explain handling transactions like this � �Forget about it!�

Even an

old fashion Bookie wire operation in the 1930�s had more supervision than

the modern day OTC.

THE SPREAD

or �the

vig�

The

difference between the bid and the ask on an open exchange is the spread.

According to Wikipedia the spread or

Vigorish,

or simply the vig, also known as juice or

the take, is the amount charged by a

bookmaker,

or bookie, for his services.

What we have on the closed non transparent OTC is no visibility to either

the Bid nor Ask. Only the BANKSTERS trade on this info. Therefore the

spread is more accurately called

the vig.

This is

completely different to electronic trades today on the NYSE and Nasdaq

where spreads have become negligible with many �spread men� being forced

out of the business. So what is the the vig or the

take on the trades where the PATSIES are desperate to get out from

under trades that have went bad since the financial crisis occurred?

According

to Bloomberg in a March 1, 2010 report:

�The five largest U.S. derivatives dealers, including

JPMorgan Chase & Co.,

Goldman Sachs Group

Inc. and

Bank of America Corp.,

were on pace through the third quarter to record as much as

$35 billion in revenue last year from trading unregulated derivatives

contracts, according to company reports collected by the Federal Reserve

and people familiar with banks� income sources.� (3)

In our

modern day world of Trillions being bantered around daily we need to think

about this number. It borders on the completely insane! It is bigger than

the GDP of a vast majority of the member countries of the United Nations.

It almost makes us feel compassion for our poor desperate duped PATSIES.

�Bookmakers use this

(the vig) concept to make money on their wagers regardless of the

outcome. Because of the vigorish concept, bookmakers should not have an

interest in either side winning in a given sporting event. They are

interested, instead, in getting equal action on each side of the event. In

this way, the bookmaker minimizes his risk and always collects a small

commission from the vigorish. The

bookmaker will normally adjust the

odds,

or line, to attract equal action on each side of an event. -

Wkipedia

CDS�s

(CREDIT DEFAULT SWAPS)

The OTC

also trades CDSs (Credit Default Swaps) which allows our PATSY to feel

confidence that they are protected if something should go wrong and the

counterparty they are contracted with is unable to pay. CDS�s are thought

as insurance but they have none of the protection of insurance where

collateral is posted for potential payouts.

What

insurance company would allow you to buy fire insurance on someone else�s

house? Insurance companies knowing it is their money at risk on a claim

would be concerned it might foster bad behavior. Since you look

particularly desperate they might suspect you of being what our former

Harvard MBA trained President (who stood watch during this era), so

eloquently erudiated as an �evil doer�. You cannot have an exchange where

people know (other than the regulated exchange itself) who is on the other

side of a trade. It leads to deviant and unfair behavior. CDS (Credit

Default Swaps) are the case in point. These instruments, which former New

York Insurance Commissioner Eric Dinallo in testimony before congress,

related there was a disagreement about who was the supervisory authority

on these instruments when they first surfaced. Both the NY Insurance

Commission and the CFTC (Commodities Futures Trading Commission) felt they

were not their responsibility and agreed with the NY Gaming Commission who

felt they more appropriately fell under their purview. That tells you

about all you really need to know about CDSs to understand our play. But

there is more � unfortunately.

It needs to be fully appreciated that our SPECULATORS in our play are

engaged in naked shorting of CDS�s in this unregulated OTC where no DTCC

exists that acts as a matching inventory custodian. There is no limit to

the number of short transactions that can be sold. For those familiar with

shorting you know you get cash upfront when you short. The cash can then

be used to fund buying Option PUTs while additionally selling the PATSIES

bonds short. The number of strategy permutations is limitless. In a $605

Trillion pool you can do a lot of splashing around.

It would

be remiss of me not to say that CDS� can have an important role to play,

but not without a regulated exchange and capital requirements on those

selling these instruments. AIG is your blatant example of what the fall

out is!

What has

been the reaction by our DIRECTORS? � You guessed it � they are still in

the midst of their siesta on the side of our stage!

INTERMISSION

OLD

SAYING:

�When you

owe the bank

$100,000

and can�t pay you have a problem. When you owe the bank 100M

($100,000,000)

and can�t pay the bank has a problem�

TODAYS

VERSION:

When the

banks owe 100B

($100,000,000,000)

and can�t pay the banks have a problem. When the Banks owe 1T

($1,000,000,000,000)

and can�t pay the taxpayer has a problem�

INTERMISSION

Sign Up for the next release in the

Sultans of Swap series:

Sultans

To be

continued with:

ACT II �

THE STING

The second act is the heist itself. With rare exception, the heist will

be successful, though some number of unexpected events will occur.

ACT III �

THE GET AWAY

The third act is the unraveling of the plot. The characters involved in

the heist will be turned against one another or one of the characters

will have made arrangements with some outside party, who will interfere.

Normally, most of or all the characters involved in the heist will end

up dead, captured by the law, or without any of the loot; however, it is

becoming increasingly common for the conspirators to be successful,

particularly if the target is portrayed as being of low moral standing,

such as

casinos,

corrupt organizations or individuals, or fellow criminals.

SOURCES

(1) 03-05-10

The Swaps that Swallowed Your Town

the New York Times

(2) 03-03-10

Smoking Swap Guns Are Beginning to Litter

EuroLand, Sovereign Debt Buyer Beware! Reggie Middleton

Reggie Middleton at the

BoomBustBlog.com

(3) 03-01-10

Frank, Peterson Vow to Eliminate Provision Keeping Swaps Opaque

Bloomberg

(4)

03-08-10

Default Protection Is Lowest in Six Weeks as Greece Calms

BL

(5) 02-10-09

CSPAN Rep Paul Kanjorski Reviews the

Bailout Situation

Wkipedia:

http://en.wikipedia.org/wiki/The_Sting The Sting

Wikipedia:

http://en.wikipedia.org/wiki/Heist_film A Heist Film

03-03-10

Smoking

Swap Guns Are Beginning to Litter EuroLand, Sovereign Debt Buyer Beware!

FREE

Additional Research Reports at Web Site:

Tipping Points

Gordon T Long

Tipping Points

Mr. Long is a former senior group executive with IBM & Motorola, a

principle in a high tech public start-up and founder of a private venture

capital fund. He is presently involved in private equity placements

internationally along with proprietary trading involving the development &

application of Chaos Theory and Mandelbrot Generator algorithms.

Gordon T Long is not a registered advisor and does not give investment

advice. His comments are an expression of opinion only and should not be

construed in any manner whatsoever as recommendations to buy or sell a

stock, option, future, bond, commodity or any other financial instrument

at any time. While he believes his statements to be true, they always

depend on the reliability of his own credible sources. Of course, he

recommends that you consult with a qualified investment advisor, one

licensed by appropriate regulatory agencies in your legal jurisdiction,

before making any investment decisions, and barring that, we encourage you

confirm the facts on your own before making important investment

commitments.

� Copyright 2010 Gordon T Long. The information herein was obtained from

sources which Mr. Long believes reliable, but he does not guarantee its

accuracy. None of the information, advertisements, website links, or any

opinions expressed constitutes a solicitation of the purchase or sale of

any securities or commodities. Please note that Mr. Long may already have

invested or may from time to time invest in securities that are

recommended or otherwise covered on this website. Mr. Long does not intend

to disclose the extent of any current holdings or future transactions with

respect to any particular security. You should consider this possibility

before investing in any security based upon statements and information

contained in any report, post, comment or recommendation you receive from

him