I

gave President Barrack Obama six months to roll-out his doomed Keynesian

policies, twelve months to discover they were flawed and eighteen months

to realize that the solution to America�s problems must lie within a

different economic framework. I had hoped by the end of twenty-four months to see

new policies closer to an Austrian economic philosophy emerge. I was

wrong.

I

gave President Barrack Obama six months to roll-out his doomed Keynesian

policies, twelve months to discover they were flawed and eighteen months

to realize that the solution to America�s problems must lie within a

different economic framework. I had hoped by the end of twenty-four months to see

new policies closer to an Austrian economic philosophy emerge. I was

wrong.

Though, even the Wall Street Journal recently featured an article on the

re-emergence of the Austrian School of Economic philosophy, it would

appear that President Obama�s administration still neither gets it, nor

I am afraid ever will. Key defections by his leading economic advisors,

talk of the need for QE II and a Stimulus II, and a political collapse

in public confidence suggests a growing awareness that Keynesian

policies are not working, as many predicted they wouldn�t. Obama's

exciting rhetoric of Hope and Change has left myself and the majority of

recent polled Americans disillusioned and disappointed. What I see the

administration failing to grasp is twofold:

I-America has a Structural problem, not a cyclical business cycle

problem. Though the cyclical business cycle was greatly worsened by the

financial crisis, I would argue that the structural problem facing the

US is actually a contributor to what caused the financial crisis.

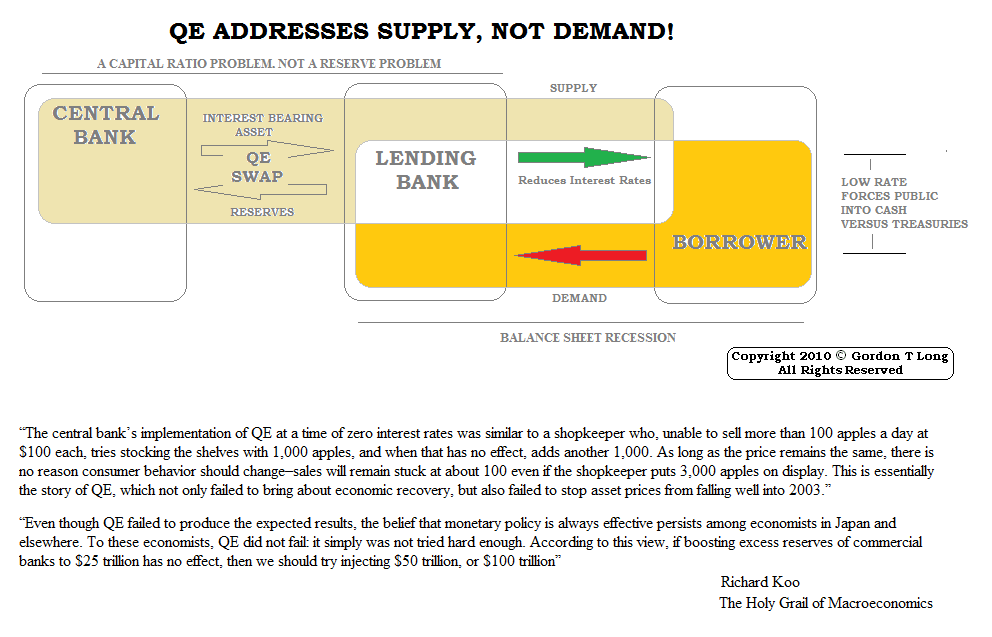

II- America has a Credit demand problem, not a Credit supply problem. It

isn�t that the banks won�t lend, but rather that few can any longer

afford or qualify (on any reasonably and historically sound basis) to

borrow.

A

STRUCTURAL PROBLEM

1) Trade

Balance: Insufficient Export/Import Ratio

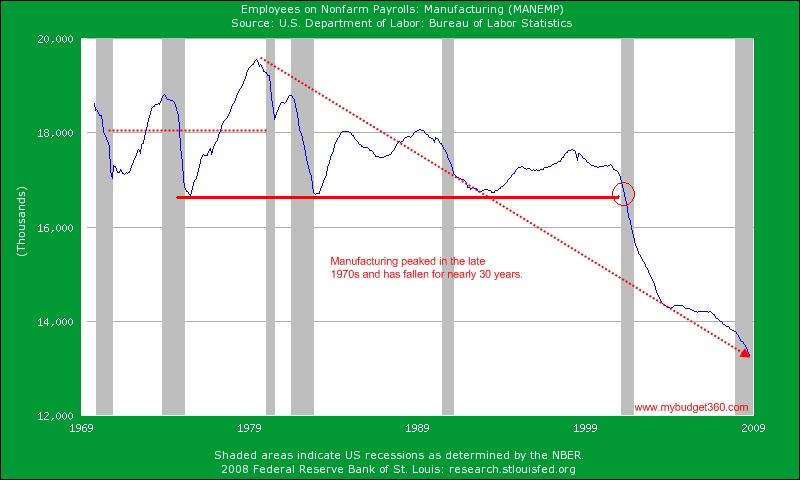

We are all painfully aware that the US has not produced sufficient

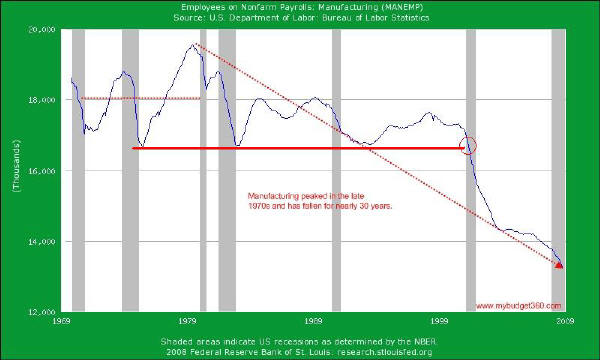

exportable product to support its standard of living for many years.

Manufacturing in the US has been in steady decline since the 1960�s and

the excess spending during the Vietnam War. It has been 50 years since

the US had a balanced budget (forget Clinton's social security slight

of hand). Over the last 10-15 years the US has seriously compounded

this problem by accelerating the de-industrializaton of America without

a strategy to replace salable export product. Corporate industrial

strategies of outsourcing, downsizing, and off-shoring were never

countered other than by an excess consumption splurge which fostered

massive real estate and retail expansion distortions.

Simply said: A US Service Economy that is based on

70% GDP consumer consumption does not pay the bills!

For a brief period of time following the dotcom implosion, the US

operated as a mercantile �Financial Economy� that turned out to have

been nothing more than a historic illusion.

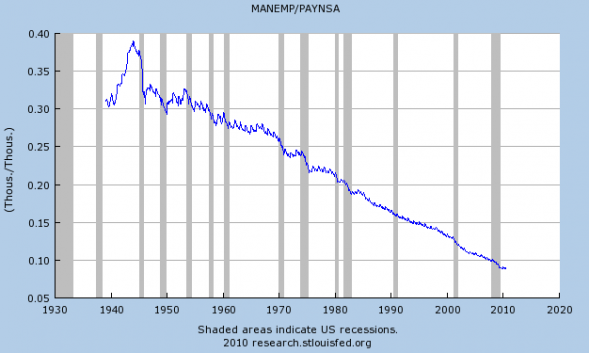

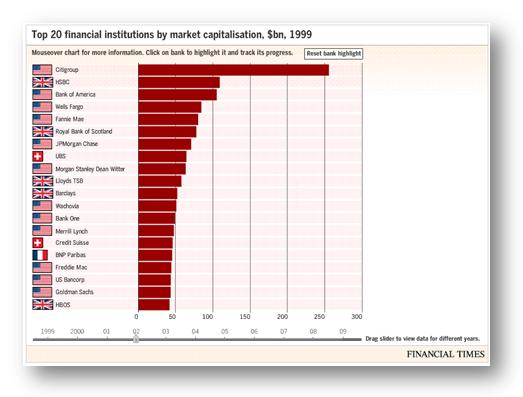

1999

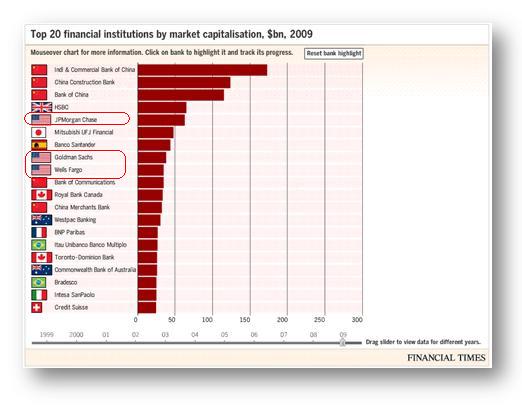

2009

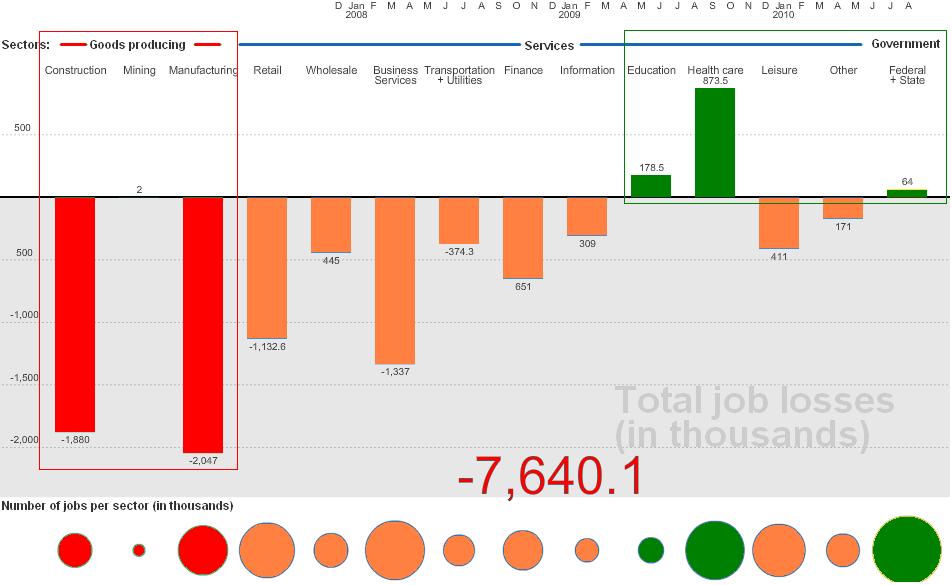

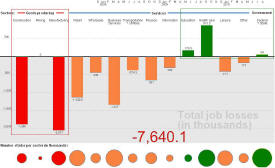

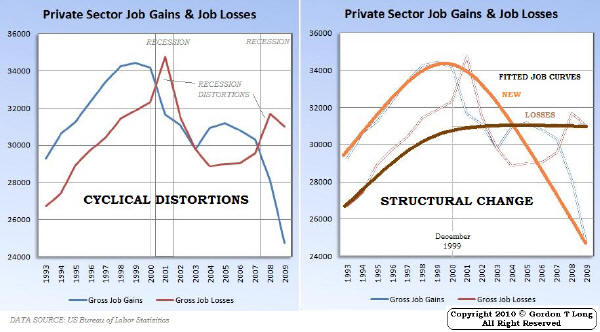

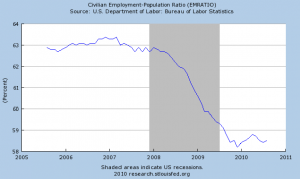

As the graphs below clearly show, since late 1999 with the

surge in the adoption of the internet, unemployment in the US has

spiked. Clerical, manufacturing and almost any job that could be further

automated through networking advancements were replaced.

2)

Creative Destruction: Slowing Innovation Rate

In my recent paper

INNOVATION: What Made America Great is now Killing Her!

, I described

how

the dotcom bubble ushered in a change in America that is still

reverberating through the nation and around the globe. The Internet

unleashed productivity opportunities of unprecedented proportions in

addition to new business models, new ways of doing business and

completely new and never before realized markets. Ten years ago there

was no such position as a Web Master; having a home PC was primarily for

word processing and creating spreadsheets; Apple made MACs and ordering

on-line was a quaint experiment for risk takers.

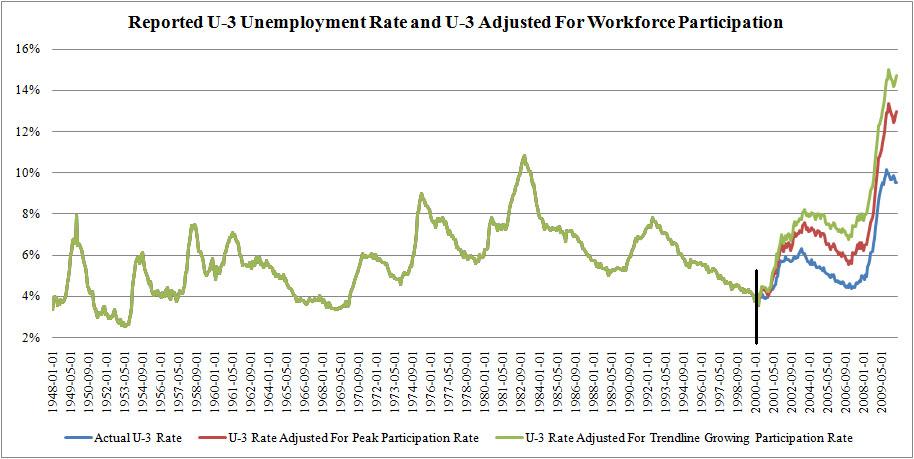

In 1997 prior to the �go-go� Dotcom era unfolding, America�s

unemployment was less than half of what it is today at 4.7%. At that

time the US added 3 Million net jobs which reflected the creation of

33.4 Million new positions while obsolescing or cutting 30.4 Million old

positions. Job losses occurred in old vocations such as typists,

secretaries, filing clerks, switchboard operators etc. Hired were new

occupations such as C++ programmers, web masters, database managers,

network analysts, etc.

As our research chart above however illustrates, the additions have

fallen off precipitously while the job losses have stayed relatively

flat. In 2009 job losses were 31M and only slightly larger than 1997,

which would be expected with further internet application development.

New job creation however was only 24.7M which is dramatically lower than

the 33.4 in 1997.

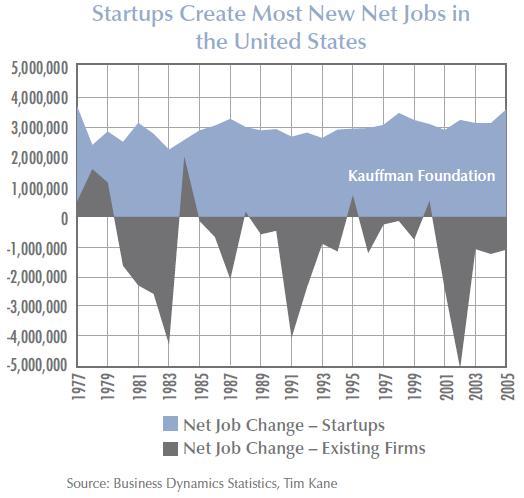

Over 98% of all jobs created in America have traditionally been created

by companies with less then 500 employees. Recent research by

the Kaufman Foundation

shows that in fact new start ups versus existing businesses dominated

the creation of new positions.

America�s slowing ability to innovate which is reflected in published

research papers, patents issued and numbers of college graduates with

advanced math and science degrees has seriously fallen behind. I laid

out the seriousness of this problem in my early 2010 paper:

America - Innovate or Die!

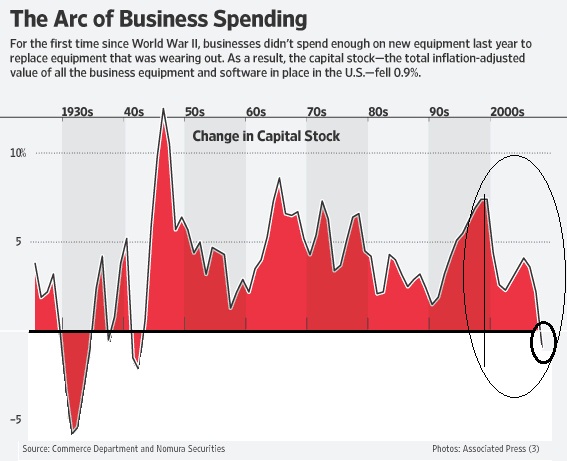

It is more than a little disconcerting that after 13 Trillion in

stimulus measures we see business spending on capital investment STILL

shrinking in the US.

It can�t be any clearer, the US has a structural problem. The

administration can not possibly fail to realize this. My sense is they

just don't know what to do about it.

A

DEMAND PROBLEM

According to the

Federal Reserve's latest quarterly survey

of banks' lending practices recorded during July 2010, �for the first

time since 2006, banks are making commercial and industrial loans more

available to small firms, with about one-fifth of large domestic banks

having eased lending standards. This offset a net tightening of

standards by a small fraction of other banks." Also, for the past six

months, banks have continued easing lending to large and mid-sized

firms. What's more, banks also reported that they stopped cutting

existing lines of credit for commercial and industrial firms for the

first time since the Fed added the question in its survey in January

2009. As for consumer loans, banks also reported easing standards for

approving loans.

Credit is available, but demand remains flat.

Asked in the

July survey

how demand for commercial and industrial loans has changed over the past

three months, 61% of banks responded "about the same," while 9% said

"moderately weaker." While it was good news that 30% responded

"moderately stronger," it's not exactly a surge in demand. Even in a

slowly recovering economy, the growing distaste for credit among our

debt-weary public has hampered the way for new purchases and

investments.

This isn't all that is surprising. The latest economic indicators paint

a very exhausted consumer: In the years leading up to the financial

crisis, he bought too much house and too many cars. The consumer is in

burn-out mode, more focused on either saving or paying down credit card

debt than buying more appliances and gadgets.

The amount consumers owed on their credit cards during the three months

ending in June dropped to its lowest levels in more than eight years,

indicating that cardholders continue to pay off balances in the

uncertain economy, according to TransUnion's

second quarter credit card statistics.

The average combined debt for bank-issued credit cards fell by more than

13% to $4,951 over the previous year. This represented the first

three-month period where credit card debt fell below $5,000 since the

three months ending in March 2002. Meanwhile, personal savings have

risen to 6.4% of after-tax incomes, about three times higher than it was

in 2007.

Perhaps what the Fed's quarterly report is really saying is this:

"There's a growing distaste for credit. The American consumer is the

child who ate too much and spoiled his dinner. And even if you hand him

his favorite meal on a silver platter, he's just not that hungry.�

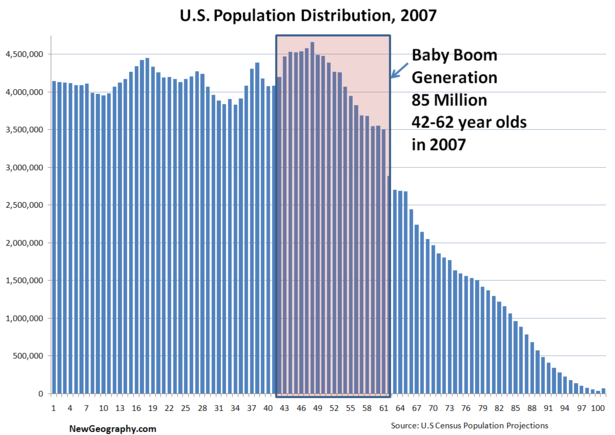

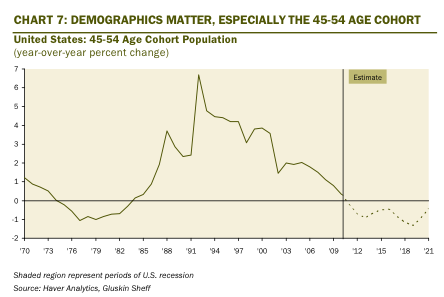

Another obvious but seldom highlighted factor affecting demand is

shifting demographics. The Baby Boomer generation is no longer the

consumption engine it has been to the US economy.

We have a generation that, as has been predicted for some time, is

reducing its expenses but it may be even more dramatic than forecasted.

With home housing prices no longer being the wealth generation vehicle

they had expected it to be, stocks not delivering the returns they had

been told to expect for the 'long term� investor and medical expenses

climbing above their worst budgeted targets, the baby boomers are being

forced to cut back even further than the expected demographics were

warning about.

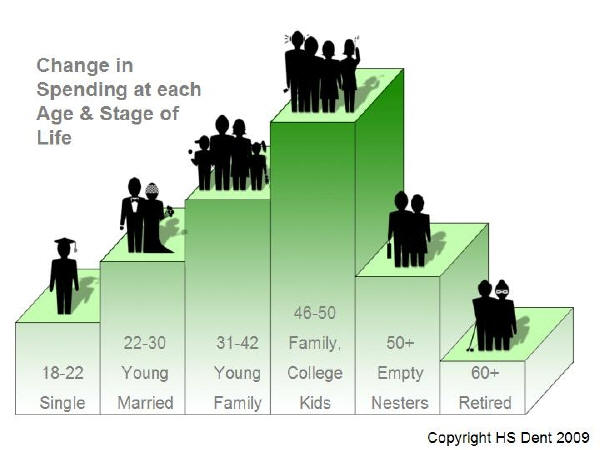

The demand for credit to finance new acquisitions is not the same

priority it was only a few years ago. Harry Dent's extensive

demographic research

lays this out in indisputable detail.

All

Federal Reserve and Government actions are about increasing credit

supply. None effectively address

demand.

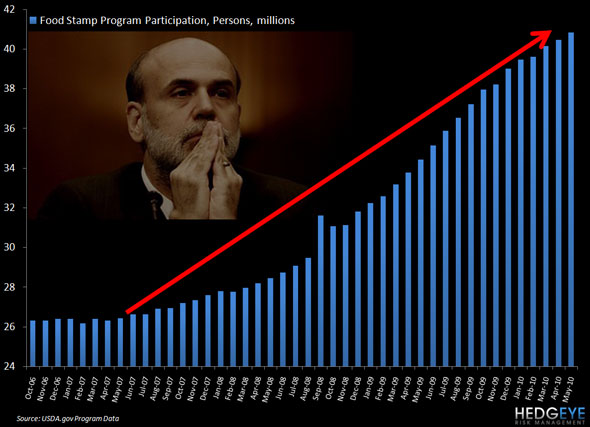

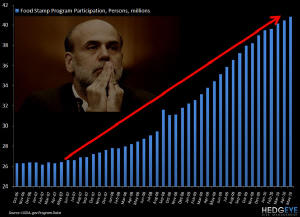

THE RESULT

|

40.8 Million Americans on Food Stamps |

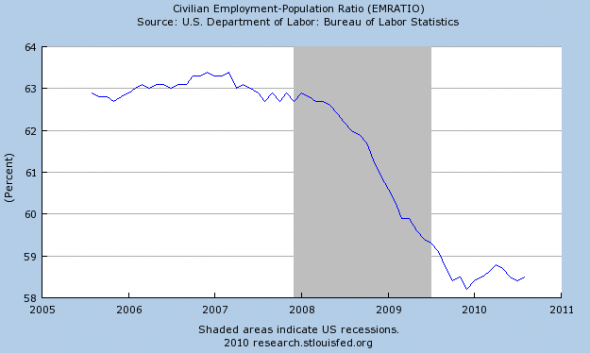

Employment at unprecedented lows |

|

|

|

Expect it to get worse until the administration finally realizes that we

have both a structural and demand problem facing America, not a cyclical

business cycle and credit availability problem. I personally don't

believe for a minute that the Obama Administration haven't come to

realize something is wrong. The White House simply doesn't know what to

do about it. They are doing the only thing our Washington political

machine knows what to do - throw money and credit at the problem, which

is precisely what got us into this problem in the first place.