|

GLOBAL EQUITES versus GDP Expectations

Read More

"BEST OF THE WEEK " |

Posting Date |

Labels & Tags |

TIPPING POINT or 2013 THESIS THEME |

HOTTEST TIPPING POINTS |

|

|

Theme Groupings |

MOST CRITICAL TIPPING POINT ARTICLES TODAY |

|

|

|

We post throughout the day as we do our Investment Research for:

LONGWave - UnderTheLens - Macro |

|

|

|

|

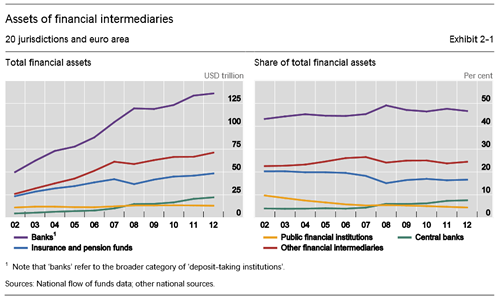

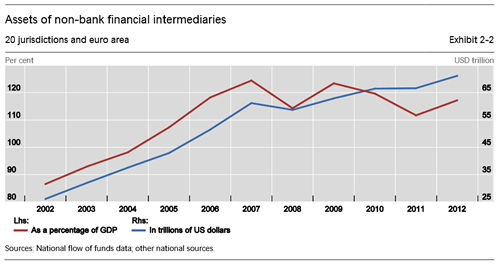

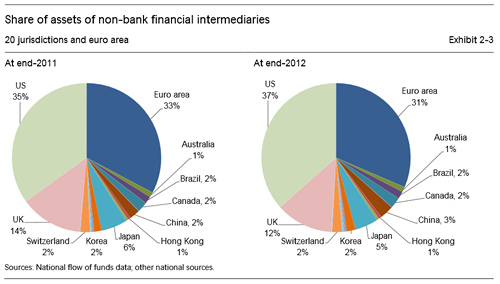

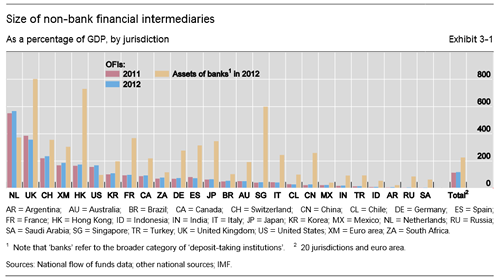

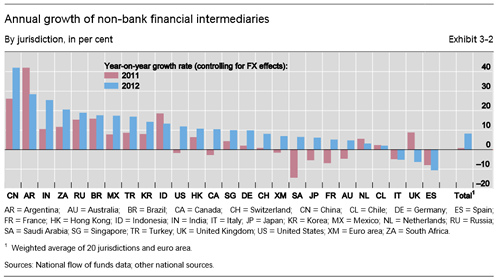

SHADOW BANKING - $71T and Now Bigger than the Global Economy

SIZING THE GLOBAL SHADOW BANKING SYSTEM

FSB's Global Shadow Banking Monitoring Report 2013 11-14-13 BIS

The main findings from the 2013 exercise are as follows :

- According to the ‘ macro mapping ’ measure , based on ‘ Other Financial Intermediaries ’(OFIs), non-bank financial intermediation grew by $5 trillion in 2012 to reach $71 trillion.

- By absolute size, advanced economies remain the ones with the largest non-bank financial systems.

- Globally OFI assets represent on average about 24% of total financial assets, about half of banking system assets and 117% of GDP. These patterns have been relatively stable since the crisis.

- OFI assets grew by +8.1% in 2012, helped by a general increase in valuation of global financial markets while bank assets were relatively stable as valuation effects were counterbalanced by shrinking balance sheets.

- The global growth trend of OFI assets masks considerable differences across jurisdictions, with growth rates ranging from -11% in Spain to +42 % in China.

- Emerging market jurisdictions showed the most rapid increases in non-bank financial system assets.

- Four emerging market jurisdictions had 2012 growth rates for non-bank financial intermediation above 20%. However, this rapid growth is from a relatively small base.

- While the non-bank financial system may contribute to financial deepening in these jurisdictions, careful monitoring is still required to detect any increases in risk factors (e.g. maturity transformation or leverage) that could arise from the rapid expansion of credit provided by the non-bank sector.

- Among the OFI sub-sectors that showed the most rapid growth in 2012 are real estate investment trusts (REITs) and funds (+30 %), other investment funds (+16%) and hedge funds (+11%).

- Of note that the growth rate for hedge funds should be interpreted with caution as the FSB macro-mapping exercise significantly underestimates the size of the hedge fund sector. The results of the recent IOSCO hedge fund survey provide a more accurate picture of the size of the hedge fund sector but do not provide an estimate of its growth

|

01-07-14 |

MACRO MONETARY |

GLOBAL MACRO |

SHADOW BANKING: Why the Fed Can't Stop Fueling The Shadow Bank

Why the Fed Can't Stop Fueling The Shadow Bank Kiting Machine 06-03-13 Bill Frezza via Menckenism blog

Fractional reserve banking is unlike most other businesses. It's not just because its product is money. It's because banks can manufacture their product out of thin air. Traditional commercial banks essentially create money through a well understood and time honored pyramiding of loans. Depositors who understand that their deposits are thereby placed at risk choose their banks accordingly.

Under the bygone rules of free market capitalism, only one thing kept banks from creating an infinite amount of money, and that was fear of failure. Failure occurs when depositors come to believe that their bank has lent out too much manufactured money to too many dodgy borrowers and may not be able to cover depositors’ withdrawals. When this happens, depositors rush to reclaim their money while there is still some left, leading to the bank’s collapse.

Under free market capitalism, banks compete along a spectrum of risk and reward. Conservative banks offer a higher degree of safety by maintaining larger reserves, thereby manufacturing and lending out less money. Through word and deed they let depositors know that they lend to only the most creditworthy borrowers, who generally must post valuable collateral. These banks remain profitable because they successfully attract prudent depositors willing to accept lower rates of interest.

Banks of a more speculative bent offer a lower degree of safety, maintaining smaller reserves to create and lend out more money. Seeking higher returns, they often lend to less creditworthy borrowers who may put up poor quality collateral or none at all. These banks attract risk-taking depositors looking for a higher rate of interest. They can be very profitable during periods of economic expansion but often fall into distress during economic downturns.

Periodic bank failures remind depositors of the connection between risk and reward. When caveat emptor rules, smart depositors who pay attention make money and dumb depositors who don't lose theirs.

Because the latter outcome is intolerable in a democracy, we have government-provided deposit insurance and other taxpayer-financed backstops that shield most depositors from the risk of loss. In theory banks pay premiums to fund this insurance. In practice these premiums are not risk-based. Banks are not penalized for making riskier loans, in turn often leaving the premiums too low to finance payouts. This creates a huge moral hazard, as it frees depositors to seek the highest return without regard for safety.

Worse, it removes conservative banks’ competitive advantage. Under a government-guaranteed deposit insurance regime, conservative bankers who want to stay in business must take on more risk in order to pay the higher interest rates necessary to attract depositors. This often sets off a race to the bottom, which results in periodic banking crises.

After each of these crises, politicians promise taxpayers that it will never happen again. And each time it does, the government creates a new set of labyrinthine regulations that attempt to mimic the business judgment of conservative bankers. Minimum reserve requirements are established, which normally become the maximum as there is little advantage in exceeding them. And both depositors and the bankers themselves become complacent about the banks’ investments because it is so easy to privatize gains and socialize losses.

Banks also learn that competitive advantage can be obtained by either gaming the regulations or having cronies write them. As regulations get more intrusive and complex, politicians discover that they can be used to advance social policies, such as increasing home ownership among voters with poor credit, thereby increasing the risk on banks’ loan books.

This mixed economic system is the one that replaced free market capitalism in hopes that it would prevent bank failures. Despite, and some even say because of, a regulatory regime that discouraged conservative banking and rewarded reckless mortgage lending, the banking system crashed - again - in 2007-2008.

What is not widely appreciated is that the ensuing government bailouts allowed an underlying shadow banking system to not only survive but grow even larger. It is called the shadow banking system because it operates outside most government-regulated banking laws. This is primarily because regulations and accounting standards haven’t caught up with the practices of these banks, which are relatively new and poorly understood.

It was the seizing up of the commercial paper and repo markets that funds the shadow banking system that abruptly halted the flow of liquidity that kept the mortgage bubble propped up. This revealed the underlying insolvency of Fannie Mae, Freddie Mac, and many commercial banks stuffed with subprime mortgage securities accumulated under the mixed economic system described above.

Powered by an exclusive club of primary reserve dealers, a group that once included high flyers like Lehman Brothers, MF Global, and Countrywide Securities, these shadow banks work hand in glove with the Federal Reserve to manufacture money by pyramiding loans atop the base money deposits held in their Federal Reserve accounts.

To the frustration of Keynesians, and despite an unprecedented Quantitative Easing (QE) by the Federal Reserve, conventional commercial banks have broken with custom and have amassed almost $2 trillion in excess reserves they are reluctant to lend as they scramble to digest all the bad loans still on their books. So most of the money manufactured today is actually being created by the shadow banks. But shadow banks do not generally make commercial loans. Rather, they use the money they manufacture to fund proprietary trading operations in repos and derivatives. |

01-07-14 |

MACRO MONETARY |

GLOBAL MACRO |

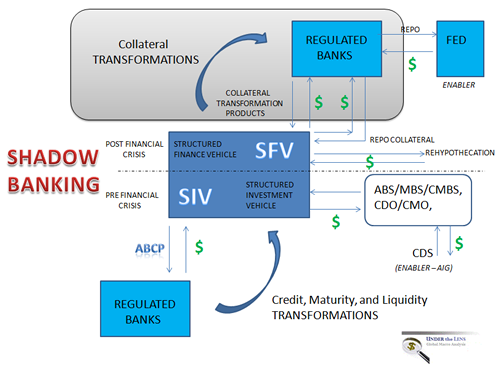

EMERGING WORLD: COLLATERAL TRANSFORMATIONS, REHYPOTHECATION & SFV's

ABOVE SCHEMATIC FROM : GLOBALIZATION TRAP by GordonTLong.com

It is critically important to distinguish the interconnectedness between banks and different types of shadow banking entities. Different shadow banking entities are associated with different risk factors such as credit intermediation, maturity transformation, and leverage.

Excerpt below taken from: Why the Fed Can't Stop Fueling The Shadow Bank Kiting Machine Bill Frezza via Menckenism blog

Where does the pyramiding come from if shadow banks aren’t making loans that get redeposited to fuel the cycle? Securities held as collateral by counterparties in a repo contract can be rehypothecated by the lender to obtain additional loans. (So can securities held in customer accounts, unless their brokerage agreements expressly prohibit it. This was an unwelcome discovery by MF Global’s hapless clients, who saw their assets whooshed off to London where different brokerage rules allow such hypothecation.) Loans made against securities held as collateral can then be used to either buy more securities, which can be fed back into the repo market, or trade a bewildering array of complex synthetic derivatives.

If this sounds like circular check kiting that’s because it is, especially when you add in the issuance of commercial paper required to grease the wheels. The biggest difference is that an embezzler kiting checks does not have the support of a central bank providing steady injections of liquidity, beefing up balance sheets that create confidence in their debt instruments.

How much of the original high quality collateral must shadow banks hold in reserve should some of their derivatives implode, as many did during the last crisis? Zero. By repeatedly spinning the wheel, the top 25 U.S. banks have piled up over $200 trillion in leveraged bets atop a thinning wedge of collateral, claims to which are spread across an opaque and complex chain of counterparties residing in multiple legal jurisdictions. These collateral claims are co-mingled with an estimated $400 trillion to $1.3 quadrillion in notional outstanding derivatives made by other banks around the world, altogether amounting to more than 20 times global GDP.

Due to the fact that accounting standards have not kept up with these innovative practices, banks are not required to report the gross notional value of the outstanding derivative contracts on their books, only their net asset positions. These theoretical Value at Risk positions, which would only be netted out if all the contracts were unwound in an orderly manner—as one might unwind a check kiting scheme before getting caught—can only be realized in a liquidity crisis if the counterparty chains across which these contracts are hedged hold up.

These counterparty chains froze in spectacular fashion during the last financial crisis. After the collapse of Lehman Brothers and with the insolvency of AIG looming, a chorus of politicians, bankers, and bureaucrats browbeat the government into delivering a system-wide bailout. As a result, many reckless banks and bankers that should have been driven out of the market are back doing business as usual.

The largest banks learned that they need not worry about the possibility of bankruptcy. When the next crisis hits, all they have to do is shout “systemic collapse” and another bailout will appear. Being Too Big To Fail, they can maximize profits without having to hold reserves against the risk of counterparty failure, knowing that the taxpayer will always be there to make them whole.

The solution is not more regulations, which will never keep up with the financial wizards whose lobbyists end up writing these rules anyway. In addition, trades can be made anywhere in the world, so to be effective the regulations would have to be global. As long as governments continue to prop up failing banks, regulation will always be inadequate to mitigate the moral hazard that accompanies bailouts. And, ironically, the added costs of regulatory compliance will make it harder still for smaller and more prudent banks to compete.

True to form, Congress has not solved the TBTF problem but has actually made it worse, loading ever more regulations on commercial banks through Dodd-Frank. Meanwhile, taxpayer exposure to the banking system has grown even larger.

Optimists believe that as long as everyone remains calm and keeps believing everything is fine, then everything will be. Central planning advocates hope that the kiting scheme can be unwound by extending banking regulations to cover the shadow banks while the Fed somehow weans them off of Quantitative Easing. Cynics believe that asking Washington to get the situation under control is a hopeless quest, especially since few Congressmen have a clue what is really going on.

Meanwhile uncertainty hangs over the system since bankruptcy laws, which differ from country to country, have not kept up with %20trillion%20in%20excess%20reserves%20they%20are%20reluctant%20to%20lend%20as%20they%20scramble%20to%20digest%20all%20the%20bad%20loans%20still%20on%20their%20books.%20So%20most%20of%20the%20money%20manufactured%20today%20is%20actually%20being%20created%20by%20the%20shadow%20banks.%20But%20shadow%20banks%20do%20not%20generally%20make%20commercial%20loans.%20Rather,%20they%20use%20the%20money%20they%20manufacture%20to%20fund%20proprietary%20trading%20operations%20in%20repos%20and%20derivatives.%20%20Where%20does%20the%20pyramiding%20come%20from%20if%20shadow%20banks%20aren%E2%80%99t%20making%20loans%20that%20get%20redeposited%20to%20fuel%20the%20cycle?%20Securities%20held%20as%20collateral%20by%20counterparties%20in%20a%20repo%20contract%20can%20be%20rehypothecated%20by%20the%20lender%20to%20obtain%20additional%20loans.%20%28So%20can%20securities%20held%20in%20customer%20accounts,%20unless%20their%20brokerage%20agreements%20expressly%20prohibit%20it.%20This%20was%20an%20unwelcome%20discovery%20by%20MF%20Global%E2%80%99s%20hapless%20clients,%20who%20saw%20their%20assets%20whooshed%20off%20to%20London%20where%20different%20brokerage%20rules%20allow%20such%20hypothecation.%29%20Loans%20made%20against%20securities%20held%20as%20collateral%20can%20then%20be%20used%20to%20either%20buy%20more%20securities,%20which%20can%20be%20fed%20back%20into%20the%20repo%20market,%20or%20trade%20a%20bewildering%20array%20of%20complex%20synthetic%20derivatives.%20%20If%20this%20sounds%20like%20circular%20check%20kiting%20that%E2%80%99s%20because%20it%20is,%20especially%20when%20you%20add%20in%20the%20issuance%20of%20commercial%20paper%20required%20to%20grease%20the%20wheels.%20The%20biggest%20difference%20is%20that%20an%20embezzler%20kiting%20checks%20does%20not%20have%20the%20support%20of%20a%20central%20bank%20providing%20steady%20injections%20of%20liquidity,%20beefing%20up%20balance%20sheets%20that%20create%20confidence%20in%20their%20debt%20instruments.%20%20How%20much%20of%20the%20original%20high%20quality%20collateral%20must%20shadow%20banks%20hold%20in%20reserve%20should%20some%20of%20their%20derivatives%20implode,%20as%20many%20did%20during%20the%20last%20crisis?%20Zero.%20By%20repeatedly%20spinning%20the%20wheel,%20the%20top%2025%20U.S.%20banks%20have%20piled%20up%20over%200%20trillion%20%20in%20leveraged%20bets%20atop%20a%20thinning%20wedge%20of%20collateral,%20claims%20to%20which%20are%20spread%20across%20an%20opaque%20and%20complex%20chain%20of%20counterparties%20residing%20in%20multiple%20legal%20jurisdictions.%20These%20collateral%20claims%20are%20co-mingled%20with%20an%20estimated%200%20trillion%20to%20href=".3%20quadrillion%20in%20notional%20outstanding%20derivatives%20made%20by%20other%20banks%20around%20the%20world,%20altogether%20amounting%20to%20more%20than%2020%20times%20global%20GDP.%20%20Due%20to%20the%20fact%20that%20accounting%20standards%20have%20not%20kept%20up%20with%20these%20innovative%20practices,%20banks%20are%20not%20required%20to%20report%20the%20gross%20notional%20value%20of%20the%20outstanding%20derivative%20contracts%20on%20their%20books,%20only%20their%20net%20asset%20positions.%20These%20theoretical%20Value%20at%20Risk%20positions,%20which%20would%20only%20be%20netted%20out%20if%20all%20the%20contracts%20were%20unwound%20in%20an%20orderly%20manner%E2%80%94as%20one%20might%20unwind%20a%20check%20kiting%20scheme%20before%20getting%20caught%E2%80%94can%20only%20be%20realized%20in%20a%20liquidity%20crisis%20if%20the%20counterparty%20chains%20across%20which%20these%20contracts%20are%20hedged%20hold%20up.%20%20These%20counterparty%20chains%20froze%20in%20spectacular%20fashion%20during%20the%20last%20financial%20crisis.%20After%20the%20collapse%20of%20Lehman%20Brothers%20and%20with%20the%20insolvency%20of%20AIG%20looming,%20a%20chorus%20of%20politicians,%20bankers,%20and%20bureaucrats%20browbeat%20the%20government%20into%20delivering%20a%20system-wide%20bailout.%20As%20a%20result,%20many%20reckless%20banks%20and%20bankers%20that%20should%20have%20been%20driven%20out%20of%20the%20market%20are%20back%20doing%20business%20as%20usual.%20%20The%20largest%20banks%20learned%20that%20they%20need%20not%20worry%20about%20the%20possibility%20of%20bankruptcy.%20When%20the%20next%20crisis%20hits,%20all%20they%20have%20to%20do%20is%20shout%20%E2%80%9Csystemic%20collapse%E2%80%9D%20and%20another%20bailout%20will%20appear.%20Being%20Too%20Big%20To%20Fail,%20they%20can%20maximize%20profits%20without%20having%20to%20hold%20reserves%20against%20the%20risk%20of%20counterparty%20failure,%20knowing%20that%20the%20taxpayer%20will%20always%20be%20there%20to%20make%20them%20whole.%20%20The%20solution%20is%20not%20more%20regulations,%20which%20will%20never%20keep%20up%20with%20the%20financial%20wizards%20whose%20lobbyists%20end%20up%20writing%20these%20rules%20anyway.%20In%20addition,%20trades%20can%20be%20made%20anywhere%20in%20the%20world,%20so%20to%20be%20effective%20the%20regulations%20would%20have%20to%20be%20global.%20As%20long%20as%20governments%20continue%20to%20prop%20up%20failing%20banks,%20regulation%20will%20always%20be%20inadequate%20to%20mitigate%20the%20moral%20hazard%20that%20accompanies%20bailouts.%20And,%20ironically,%20the%20added%20costs%20of%20regulatory%20compliance%20will%20make%20it%20harder%20still%20for%20smaller%20and%20more%20prudent%20banks%20to%20compete.%20%20True%20to%20form,%20Congress%20has%20not%20solved%20the%20TBTF%20problem%20but%20has%20actually%20made%20it%20worse,%20loading%20ever%20more%20regulations%20on%20commercial%20banks%20through%20Dodd-Frank.%20Meanwhile,%20taxpayer%20exposure%20to%20the%20banking%20system%20has%20grown%20even%20larger.%20%20Optimists%20believe%20that%20as%20long%20as%20everyone%20remains%20calm%20and%20keeps%20believing%20everything%20is%20fine,%20then%20everything%20will%20be.%20Central%20planning%20advocates%20hope%20that%20the%20kiting%20scheme%20can%20be%20unwound%20by%20extending%20banking%20regulations%20to%20cover%20the%20shadow%20banks%20while%20the%20Fed%20somehow%20weans%20them%20off%20of%20Quantitative%20Easing.%20Cynics%20believe%20that%20asking%20Washington%20to%20get%20the%20situation%20under%20control%20is%20a%20hopeless%20quest,%20especially%20since%20few%20Congressmen%20have%20a%20clue%20what%20is%20really%20going%20on.%20%20Meanwhile%20uncertainty%20hangs%20over%20the%20system%20since%20bankruptcy%20laws,%20which%20differ%20from%20country%20to%20country,%20have%20not%20kept%20up%20with%20hyper-hypothecation.%20Moreover,%20the%20government%E2%80%99s%20handling%20of%20the%20auto%20bailout%20shows%20that%20investors%20cannot%20rely%20on%20existing%20bankruptcy%20law%20even%20when%20it%20speaks%20clearly%20on%20an%20issue.%20Therefore,%20no%20one%20really%20knows%20who%20will%20have%20first%20dibs%20on%20the%20collateral%20when%20the%20music%20stops.%20And%20just%20what%20are%20those%20high%20quality%20assets?%20Sovereign%20bonds%20and%20mortgage%20CDOs,%20which%20are%20themselves%20subject%20to%20precipitous%20losses.%20%20As%20the%20debate%20drags%20on%20and%20global%20economic%20conditions%20worsen,%20the%20growing%20pyramid%20is%20being%20kept%20afloat%20by%20the%20easy%20money%20policies%20of%20central%20banks%20too%20frightened%20to%20withdraw%20their%20support%20lest%20a%20stock%20market%20correction%20trigger%20a%20cascade%20of%20margin%20calls%20that%20brings%20down%20the%20whole%20system%E2%80%94much%20like%20last%20time.%20%20%20All%20this%20money%20creation%20has%20not%20yet%20generated%20much%20visible%20consumer%20price%20inflation.%20This%20is%20partly%20because%20official%20inflation%20measures%20are%20suspect%20but%20mostly%20because%20the%20bulk%20of%20the%20new%20money%20being%20created%20is%20flowing%20into%20financial%20assets%20and%20not%20the%20consumer%20economy.%20This%20has%20inflated%20asset%20bubbles%20to%20levels%20impossible%20to%20justify%20based%20on%20underlying%20economic%20conditions,%20in%20particular%20the%20stock%20market%20where%20investors%20have%20fled%20in%20search%20of%20yield.%20No%20one%20knows%20when%20the%20bubble%20will%20pop,%20but%20when%20it%20does%20a%20donnybrook%20is%20going%20to%20break%20out%20over%20that%20thin%20wedge%20of%20collateral%20whose%20ownership%20is%20spread%20across%20counterparties%20around%20the%20world,%20each%20looking%20for%20relief%20from%20their%20own%20judges,%20politicians,%20bureaucrats,%20and%20taxpayers.%20%20When%20that%20happens%20and%20the%20clamor%20for%20regulation,%20nationalization,%20confiscation,%20and%20demonization%20arises%20there%20is%20only%20one%20thing%20we%20can%20be%20sure%20of.%20The%20disaster%20will%20once%20again%20be%20blamed%20on%20a%20free%20market%20capitalism%20that%20has%20not%20existed%20in%20this%20country%20for%20over%20100%20years.">hyper-hypothecation. Moreover, the government’s handling of the auto bailout shows that investors cannot rely on existing bankruptcy law even when it speaks clearly on an issue. Therefore, no one really knows who will have first dibs on the collateral when the music stops. And just what are those high quality assets? Sovereign bonds and mortgage CDOs, which are themselves subject to precipitous losses.

As the debate drags on and global economic conditions worsen, the growing pyramid is being kept afloat by the easy money policies of central banks too frightened to withdraw their support lest a stock market correction trigger a cascade of margin calls that brings down the whole system—much like last time.

All this money creation has not yet generated much visible consumer price inflation. This is partly because official inflation measures are suspect but mostly because the bulk of the new money being created is flowing into financial assets and not the consumer economy. This has inflated asset bubbles to levels impossible to justify based on underlying economic conditions, in particular the stock market where investors have fled in search of yield. No one knows when the bubble will pop, but when it does a donnybrook is going to break out over that thin wedge of collateral whose ownership is spread across counterparties around the world, each looking for relief from their own judges, politicians, bureaucrats, and taxpayers.

When that happens and the clamor for regulation, nationalization, confiscation, and demonization arises there is only one thing we can be sure of. The disaster will once again be blamed on a free market capitalism that has not existed in this country for over 100 years.

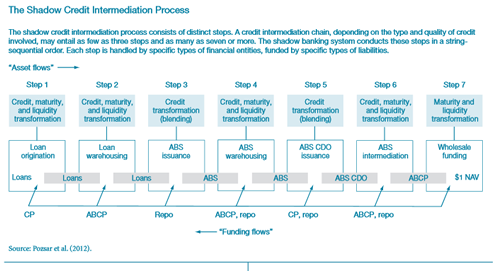

SHADOW BANKING - NEW YORK FEDERAL RESERVE - The Definitive Work on Shadow Banking & The Financial Crisis

Shadow banks are best thought along a spectrum. Each of the seven steps involved in the shadow credit intermediation process were performed by many different types of shadow banks, with varying asset mixes, funding strategies, amounts of capital and degrees of leverage.

CLICK TO ENLARGE

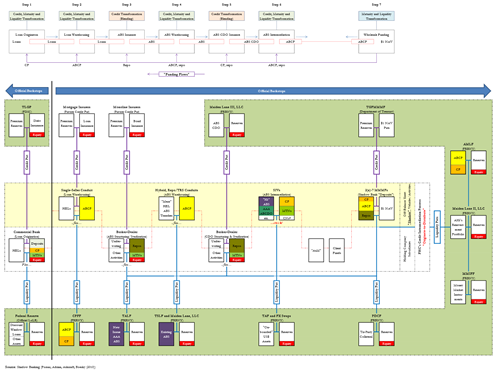

The Post-Crisis Backstop of the Shadow Banking System - Pozsar, Adrian, Ashcraft, Boesky (2010)

Once private sector credit and liquidity put providers' ability to make good on their "promised" puts came into question, a run began on the shadow banking system. Central banks generally ignored the impairment of such important pillars of the shadow banking system as mortgage insurers or monoline insurers. Once the crisis gathered momentum, however, central banks became more engaged.

The series of 13 liquidity facilities implemented by the Federal Reserve and the guarantee schemes of other government agencies essentially amount to a 360º backstop of the shadow banking system. The 13 facilities can be interpreted as functional backstops of the shadow credit intermediation process. Thus,

- CPFF is a backstop of loan origination and warehousing;

- TALF is a backstop of ABS issuance;

- TSLF and Maiden Lane, LLC are backstops of th e system's securities w arehouses (broadly speaking);

- Maiden Lane III, LLC is a backstop of the credit puts sold by AIG-FP on AB S CDOs;

- TAF and FX sw aps are backstops of and facilitated the orderly "on-boarding" of formerly off-balance sheet ABS intermediaries (many of them run by European banks who found it hard to swap FX for dollars); and finally,

On the funding side,

- PDCF is a backstop of the tri-party repo system (a "platofrm" where MMMFs (and other funds) fund broker-dealers and large hedge-funds) and the

- AMLF, MMIFF and Maiden Lane II, LLC are backstops of various forms of regulated and undregulated money market intermediaries.

- Furthermore, the Treasury Department's Temporary Guarantee Program of MMMFs was an additional form of backstop for money market intermediaries. This program, together with the FDIC's TLGP can be considered modern day equivalents of deposit insurance.

Only a few types of entities were not backstopped by the crisis, and some attempts to fix problems might have exacerbated the crisis . Examples include not backstopping the monolines early on in the crisis (this might have tamed the destructiveness of delevera ging) and the failed M-LEC which ultimately led to a demarcation line between bank-affiliated and standalone ABS intermediaries (such as LPFCs or credit hedge funds) as recipients and non-recipients of official liquidity. These entities failed too early on in the crisis to benefit from the liquidity facilities rolled out in the wake of the bankruptcy of Lehman Brothers, and their demise may well have accelerated and deepened the crisis, while also necessitating the creation of TALF to offset the shrinkage in balance sheet capacity for ABS from their demise.

CLICK TO ENLARGE

These appendixes, which depict graphically the processes described in the article, offer a comprehensive look at the shadow banking system and its many components.

- Map : The Shadow Banking System www.newyorkfed.org/research/economists/adrian/1306adri_map.pdf

- Appendix 1 : The Government-Sponsored Shadow Banking System www.newyorkfed.org/research/economists/adrian/1306adri_A1.pdf

- Appendix 2 : The Credit Intermediation Process of Bank Holding Companies www.newyorkfed.org/research/economists/adrian/1306adri_A2.pdf

- Appendix 3 : The Credit Intermediation Proc ess of Diversified Broker-Dealers www.newyorkfed.org/research/economists/adrian/1306adri_A3.pdf

- Appendix 4 : The Independent Specialists-Base d Credit Intermediation Process www.newyorkfed.org/research/economists/adrian/1306adri_A4.pdf

- Appendix 5 : The Independent Specialists-Base d Credit Intermediation Process www.newyorkfed.org/research/economists/adrian/1306adri_A5.pdf

- Appendix 6 : The Spectrum of Shadow Banks within a Spectrum of Shadow Credit Intermediation www.newyorkfed.org/research/economists/adrian/1306adri_A6.pdf

- Appendix 7 : The Pre-Crisis Backstop of the Sh adow Credit Intermediation Process www.newyorkfed.org/research/economists/adrian/1306adri_A7.pdf

- Appendix 8 : The Post-Crisis Backstop of the Shadow Banking System www.newyorkfed.org/research/economists/adrian/1306adri_A8.pdf

|

01-07-14 |

MACRO MONETARY |

GLOBAL MACRO |

| MOST CRITICAL TIPPING POINT ARTICLES THIS WEEK - December 29th - January 4th |

|

|

|

| RISK REVERSAL |

|

|

1 |

| JAPAN - DEBT DEFLATION |

|

|

2 |

| BOND BUBBLE |

|

|

3 |

EU BANKING CRISIS |

|

|

4 |

| SOVEREIGN DEBT CRISIS [Euope Crisis Tracker] |

|

|

5 |

| CHINA BUBBLE |

|

|

6 |

GREAT REFLATION

ASSET VALUATIONS - Risk And Reality In The US Economy

"We're at the end of Asset Inflation and that will dawn on the market very soon."

Risk And Reality In The US Economy 12-24-13 Saxo Bank via ZH

The US economy is stabilizing, but it's not truly recovering. That's the view of Saxo Bank's Chief Investment Officer, Steen Jakobsen. Following the Fed's tapering news, Steen says the risk is that we trade on perception and not reality. Clearly, the outgoing Fed Chairman, Ben Bernanke, wanted to send a signal to the markets.

Global equity markets, notably in the States, have been hitting record highs for weeks; but Steen warns "we're coming to the end of that cycle."

- Actual growth in America is well below the average rate of the past 60 years and

- Job creation too is lagging.

- People may be starting to feel more confident but that's still not translating into significantly higher employment or wages.

"We're at the end of asset inflation," he says, and that "will dawn on the market very soon."

� �

|

01-06-14 |

US

CANARIES |

19 - US Stock Market Valuations |

GREAT REFLATION

HOUSING - The Real Cost of Buying a Home 6.7 X Average Salary

Spot The Paradox 12-24-13 Zero Hedge

Based on the median real income, home prices have never been more unaffordable at a stunning 6.7x average salary.

|

01-06-14 |

US CATALYST-HOUSING |

26 - Rising Inflation Pressures & Interest Pressures |

| TO TOP |

| MACRO News Items of Importance - This Week |

GLOBAL MACRO REPORTS & ANALYSIS |

|

|

|

US ECONOMIC REPORTS & ANALYSIS |

|

|

|

| CENTRAL BANKING MONETARY POLICIES, ACTIONS & ACTIVITIES |

|

|

|

|

|

|

|

| Market |

| TECHNICALS & MARKET |

|

|

|

PATTERNS - Mid Term Election Year Pattern

MID TERM ELECTION YEAR PATTERN

This follows very closely our 2014 Technical Pattern Outlook

SOURCE: Chart of the Day 12-24-13

The chart illustrates how the stock market has performed during the average mid-term election year. Since 1950, the first nine months of the average mid-term election year have tended to be subpar (see thick blue line). That subpar performance was then followed by a significant year-end rally. One theory to support this behavior is that investors abhor uncertainty. To that end, investors tend to pull back prior to an election when the outcome is unknown. Beginning in early October, however, the outcome of the election becomes increasingly apparent and investors respond by positioning their portfolios accordingly.

|

01-06-14 |

PATTERNS |

|

PATTERNS - Sornette's Log-Periodic Model Prediction

Peak Speculation And The Ides Of January 14th 01-05-14 Via John Hussman,

Confidence abounds. Last week, Investor’s Intelligence reported a surge in advisory sentiment to the highest bullish percentage since October 19, 2007. John Hussman notes that NAAIM reported that the 3-week average equity exposure among its members increased to the highest level on record. Given the unfortunate resolution of similarly extreme overvalued, overbought, overbullish, rising-yield periods in history, it's almost mind-boggling that investors actually expect the present speculative run to end well. The accelerating pitch and shallowing corrections of the recent advance are worth noting.

Via John Hussman,

Based on the fidelity of the recent advance to this price structure, we estimate the “finite-time singularity” of the present log-periodic bubble to occur (or to have occurred) somewhere between December 31, 2013 and January 13, 2014. That does not mean that prices must immediately crash – only that the dynamics will then lend themselves to a great deal of potential instability, if prior log-periodic bubbles in equity and commodity markets across history are any indication. It bears repeating that our own defensiveness is driven by a broad ensemble of evidence, not simply price dynamics, not simply valuations, not simply sentiment, but the “full catastrophe” – which includes the fact that strong economic, speculative and monetary enthusiasm has historically been quite a contrary indicator for stocks.

The chart below shows the current position of the S&P 500. The light red line shows the log-periodic price trajectory that most closely approximates the present overvalued, overbought, overbullish, Fed-induced speculative run since 2010. While the initial gains from the 2009 low until about mid-2010 represented what we view as a move from reasonable valuation to full valuation (our stress-testing “miss” was not on valuation grounds), I expect little, if any of the market’s gains since 2010 to be retained by investors over the completion of this market cycle. Despite very short-run uncertainties about market direction, I should note that we now estimate negative prospective total returns for the S&P 500 on every horizon of less than 7 years.

And this is what Hussman said in 2007...

“Wall Street remains exuberant about economic prospects. Last week brought a 6-year high in consumer confidence, evidently supporting the idea that the consumer remains strong and the economic expansion remains intact. Unfortunately, if you examine the data, you'll quickly discover that consumer confidence is a lagging indicator, well explained by past movements in GDP, employment, and capacity utilization. Worse, for the stock market, it's a contrary indicator.

This is a fact that I've noted at both extremes, not only in early 2000 when new highs in consumer confidence supported a defensive position, but conversely in the early 1990's, when new lows in consumer confidence supported a leveraged position in stocks. High levels of economic optimism are regularly observed at the peaks of both U.S. and foreign economic expansions.

This includes the general consensus of individuals, businesses, politicians, central bank officials and notoriously – economists. That shouldn't be surprising. It's the very nature of a peak that it can't be produced except by unusual optimism.”

Hussman Weekly Market Comment, 08/06/07 Strong Economic Optimism (… is a Contrary Indicator)

Sound familiar?

|

01-06-14 |

PATTERNS |

|

| COMMODITY CORNER - HARD ASSETS |

|

PORTFOLIO |

|

| COMMODITY CORNER - AGRI-COMPLEX |

|

PORTFOLIO |

|

| SECURITY-SURVEILANCE COMPLEX |

|

PORTFOLIO |

|

|

|

|

|

| THESIS Themes |

2013 - STATISM |

|

|

|

2012 - FINANCIAL REPRESSION |

|

|

|

2011 - BEGGAR-THY-NEIGHBOR -- CURRENCY WARS |

|

|

|

2010 - EXTEND & PRETEND |

|

|

|

| THEMES |

| NATURE OF WORK -PRODUCTIVITY PARADOX |

|

|

|

| GLOBAL FINANCIAL IMBALANCE - FRAGILITY & INSTABILITY |

|

|

|

| CENTRAL PLANINNG -SHIFTING ECONOMIC POWER |

|

|

|

| SECURITY-SURVEILLANCE COMPLEX -STATISM |

|

|

|

| STANDARD OF LIVING -GLOBAL RE-ALIGNMENT |

|

|

|

| CORPORATOCRACY -CRONY CAPITALSIM |

|

|

|

CORRUPTION & MALFEASANCE -MORAL DECAY - DESPERATION, SHORTAGES.. |

|

|

|

| SOCIAL UNREST -INEQUALITY & BROKEN SOCIAL CONTRACT |

|

|

|

| CATALYSTS -FEAR & GREED |

|

|

|

| GENERAL INTEREST |

|

|

|

| TO TOP |

Learn more about Gold & Silver-Backed, Absolute Return Alternative Investments

with these complimentary educational materials |

Tipping Points Life Cycle - Explained

Click on image to enlarge

|

YOUR SOURCE FOR THE LATEST

GLOBAL MACRO ANALYTIC

THINKING & RESEARCH

|

�

|

| TERMS OF USE |

Gordon T Long is not a registered advisor and does not give investment advice. His comments are an expression of opinion only and should not be construed in any manner whatsoever as recommendations to buy or sell a stock, option, future, bond, commodity or any other financial instrument at any time. Of course, he recommends that you consult with a qualified investment advisor, one licensed by appropriate regulatory agencies in your legal jurisdiction, before making any investment decisions, and barring that, we encourage you confirm the facts on your own before making important investment commitments.

THE CONTENT OF ALL MATERIALS: SLIDE PRESENTATION AND THEIR ACCOMPANYING RECORDED AUDIO DISCUSSIONS, VIDEO PRESENTATIONS, NARRATED SLIDE PRESENTATIONS AND WEBZINES (hereinafter "The Media") ARE INTENDED FOR EDUCATIONAL PURPOSES ONLY.

The Media is not a solicitation to trade or invest, and any analysis is the opinion of the author and is not to be used or relied upon as investment advice. Trading and investing can involve substantial risk of loss. Past performance is no guarantee of future returns/results. Commentary is only the opinions of the authors and should not to be used for investment decisions. You must carefully examine the risks associated with investing of any sort and whether investment programs are suitable for you. You should never invest or consider investments without a complete set of disclosure documents, and should consider the risks prior to investing. The Media is not in any way a substitution for disclosure. Suitability of investing decisions rests solely with the investor. Your acknowledgement of this Disclosure and Terms of Use Statement is a condition of access to it. Furthermore, any investments you may make are your sole responsibility.

THERE IS RISK OF LOSS IN TRADING AND INVESTING OF ANY KIND. PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS.

Gordon emperically recommends that you consult with a qualified investment advisor, one licensed by appropriate regulatory agencies in your legal jurisdiction, before making any investment decisions, and barring that, he encourages you confirm the facts on your own before making important investment commitments.

|

DISCLOSURE STATEMENT

|

Information herein was obtained from sources which Mr. Long believes reliable, but he does not guarantee its accuracy. None of the information, advertisements, website links, or any opinions expressed constitutes a solicitation of the purchase or sale of any securities or commodities.

Please note that Mr. Long may already have invested or may from time to time invest in securities that are discussed or otherwise covered on this website. Mr. Long does not intend to disclose the extent of any current holdings or future transactions with respect to any particular security. You should consider this possibility before investing in any security based upon statements and information contained in any report, post, comment or recommendation you receive from him. |

|

FAIR USE NOTICE This site contains

copyrighted material the use of which has not always been specifically

authorized by the copyright owner. We are making such material available in

our efforts to advance understanding of environmental, political, human

rights, economic, democracy, scientific, and social justice issues, etc. We

believe this constitutes a 'fair use' of any such copyrighted material as

provided for in section 107 of the US Copyright Law. In accordance with

Title 17 U.S.C. Section 107, the material on this site is distributed

without profit to those who have expressed a prior interest in receiving the

included information for research and educational purposes.

If you wish to use

copyrighted material from this site for purposes of your own that go beyond

'fair use', you must obtain permission from the copyright owner.

COPYRIGHT © Copyright 2010-2011 Gordon T Long. The information herein was obtained from sources which Mr. Long believes reliable, but he does not guarantee its accuracy. None of the information, advertisements, website links, or any opinions expressed constitutes a solicitation of the purchase or sale of any securities or commodities. Please note that Mr. Long may already have invested or may from time to time invest in securities that are recommended or otherwise covered on this website. Mr. Long does not intend to disclose the extent of any current holdings or future transactions with respect to any particular security. You should consider this possibility before investing in any security based upon statements and information contained in any report, post, comment or recommendation you receive from him.

|

|

{kind=link}

{kind=link}