Axel Merk, Lance Roberts, F.William Engdahl, Catherine Austin Fitts, Bert Dohmen, David Chapman, Bill Laggner, Richard Duncan, Michael Snyder, John Williams, Rick Davies AND MORE...

STRATEGIC INVESTMENT INSIGHTS

Follow our FREE MACRO INSIGHT Articles & Research papers.

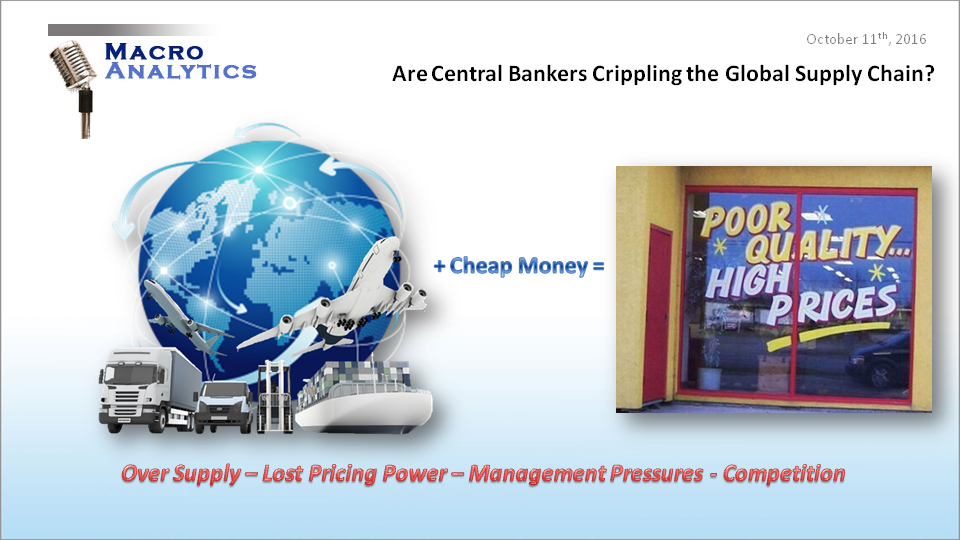

ARE CENTRAL BANKERS CRIPPLING THE GLOBAL SUPPLY CHAIN?

Charles Hugh Smith

Regular Co-Host:CHARLES HUGH SMITH , Author & Publisher of OfTwoMinds.com

ARE CENTRAL BANKERS CRIPPLING THE GLOBAL SUPPLY CHAIN?

Gordon T Long and Charles Hugh Smith begin 'pealing the onion' on a deteriorating global supply chain and what the root cause is.

Charles Hugh Smith & Gordon T Long

VIDEO: 35 Minutes - 21 Slides

SAMSUNG'S GALAXY BATTERY JUST THE TIP OF THE ICEBERG

Though the Samsung Galaxy Note 7 battery problem is presently receiving a tremendous amount of media and public attention, what few appreciate is that it is only the tip of the iceberg of cracks in the global supply chained as a result of unintended consequences of central bank monetary policies. In this 35 minute video Gordon T Long and Charles Hugh Smith begin 'pealing the onion' on a deteriorating global supply chain and what the root cause is.

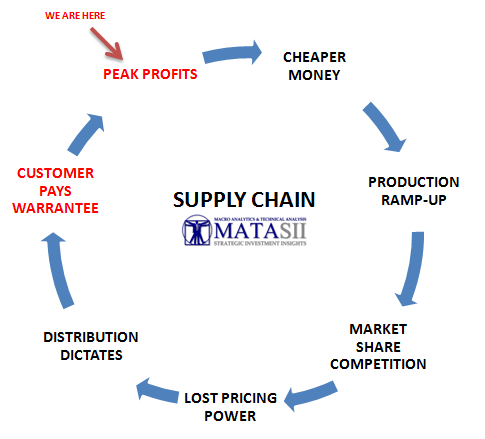

Economists have been preoccupied since the 2008 Financial Crisis with stimulating economic growth through policies which attempt to create Demand. It is debatable whether these Keynesian stimulus programs have succeeded, but what isn't debatable is that cheap money has exploded global supply!

PEAK PROFITS

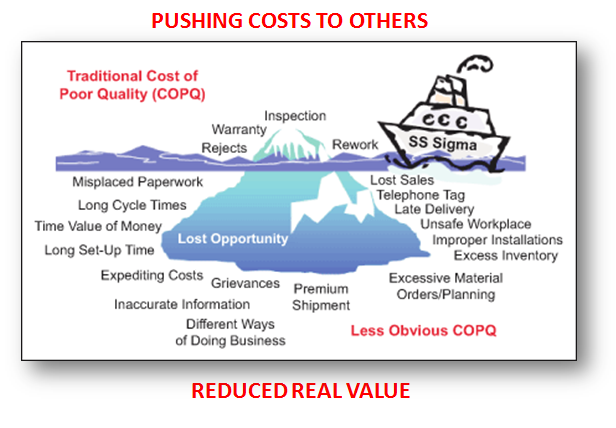

Though Corporate Profits are presently at all time highs, revenue growth and margins are rolling over and cashflows are falling. This has been placing incredible pressures through out the global supply chain. It is resulting in deteriorating product quality when considered in light of total cost of ownership and whether the customer is actually getting more for less or whether they are now receiving less for more!

WHAT WE CAN LEARN FROM WALMART, WELLS FARGO and PEAK PROFITS

The pressures big distribution players like Wal-Mart are placing on global product suppliers is well recognized. What is less recognized is how internal cultures are changing due to increasing pressures and demands. This issue has received the glare of the public spotlight through the deviant behavior of Wells Fargo. What we witnessed during testimony before congress because of the fraudulent creation of thousands of fictional accounts and the resulting firing of thousands of apparent guilty parties is that the top down pressures by executives to meet unrealistic goals is causing workers at all levels to "cheat"!

Senior executives are fired for not meeting quarterly financial goals even if the economy is slowing and profits are at historic levels. Something has to give somewhere and that "give" is occurring in the hidden bowels of product quality.

DETERIORATING QUALITY

Gordon's background allows him to critically examine the quality issues he has personally experienced over the last 6 weeks and what these examples are indicating. The examples highlighted include:

Marine Propulsion

Automotive Repair

Dell Hard Drives and HP NIC Cards

Gas Range Lighting

Healthcare

TV Programming

The conclusion is that this is only the initial waves of more to come.

In a conversation Gordon had with the head of Global Supply Chain for a major corporation he was told that focus had been taken off this critical area over the last few years but was now being urgently attended to. Samsung has added additional urgency as the public and regulators will be intolerant the next time such an event occurs..

PUSHING COSTS TO THE UNSUSPECTING

The cost of poor quality is now being pervasively felt across the entire supply chains. It beginning to reach out and impact all participants. It like a cancer which growths quietly and often it is to late when finally detected.

CONSUMERS GETTING LESS FOR MORE

WHAT WE NEED TO RECOGNIZE

In a “Bottoms Up”, Sound Money, Competitive, Capitalism Economy :

You Get MORE for LESS

In a “Top Down”, Manipulated, Over Regulated , Fiat Crony Economy:

You Get LESS for MORE

WHAT WE NEED TO UNDERSTAND

We are Steadily Getting Less and Less for More and More!

(Moving towards Statism)

Eventually You Get Nothing at the Cost of Everything

SPECIAL GUEST HOST:JOHN RUBINO, Author & Publisher of DollarCollapse.com

SIGNS OF PANIC!

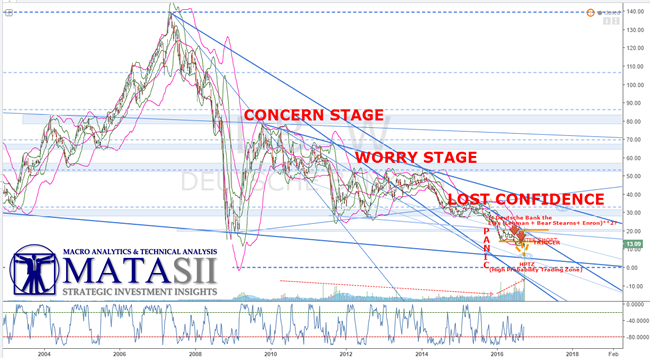

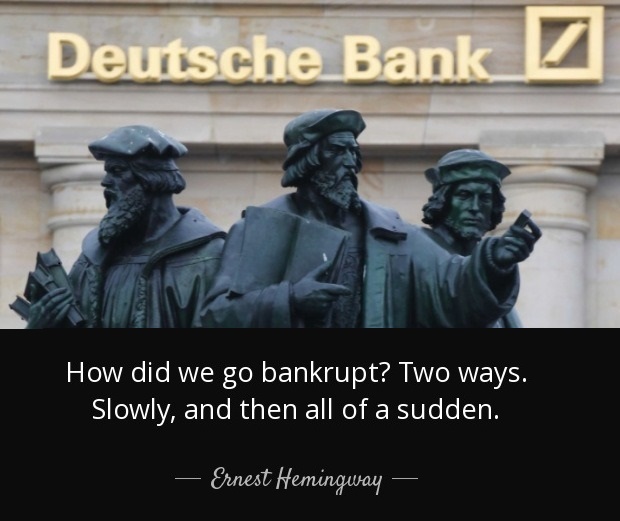

DEUTSCHE BANK

with John Rubino & Gordon T Long

Published 10-01-16

25 Minute Video

John Rubino and Gordon T Long discuss the unfolding mayhem in the European banking sector and specifically what is behind the panic selling in Deutsche Bank stock.

DEUTSCHE BANK - .... then all of a sudden!

Gordon T Long outlines:

"We have seen this coming for some time and is why in the spring we issued a feature report entitled "Is Deutsche Bank EU's (Lehman + Bear Stearns + Enron)**2? " We were pointing out that the Leverage at Lehman Bros, the Bond Portfolio's at Bear Stearns and the Derivatives at Enron which brought these corporations down, pales in comparison to Deutsche bank which sits on all three of these potential Tipping Points which can cause lost investor confidence and a bank run.

John Rubino says:

"We can stop watching the Italian Banks and start watching the German Banks. Counter-Intuitively the most rock solid banks, in the most rock solid country in Europe have become the biggest systemic risk in the global economy! Part of the reason is the German Banks have been doing in effect something called "Vendor Financing"!

"GERMANY IS ON THE HOOK FOR ITALY, SPAIN / PORTUGAL AND GREECE. WHICH MEANS THE PERIPHERAL COUNTRIES IN THE EUROZONE WHICH CAN'T FUNCTION AS CURRENTLY CONFIGURED ARE A MAJOR RISK FOR DEUTSCHE BANK".... It is becoming increasingly evident the peripherals can't pay back their debts!

People are beginning to understand that the pillars of all this debt may soon blow up!

What is looking like another European banking crisis could quickly become a currency crisis as it is likely to impair the Euro. This is even a bigger global issue as it would likely spill over into the bond market.

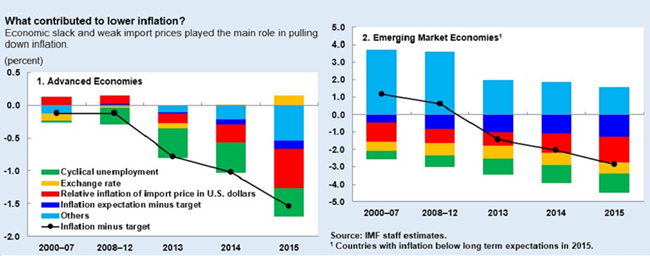

IMF WARNING: "Central Banks Losing the Deflation Fight"

Since the derivatives book of Deutsche Bank is bigger than the entire Eurozone economy it additionally means that deflationary pressures are going to cause major disruptions at some point when the underlying loans begin to default and debt rollover gets harder to secure.

"It is clear what they do next, proposals are now coming out of the woodwork from the easy money, Keynesian side of the spectrum which involves massive increases in money creation and government fiscal spending."

WHY ARE FOOD PRICES SUDDENLY FALLING?

Grocery prices have fallen for nine straight months and might possibly be a canary in the coal mine.

"Ultra easy money and ultra aggressive fiscal policy hasn't worked and given us a 'rip roaring" inflationary boom that Keynesian economists say you should get from negative interest rates and trillion dollar per year government deficits. So if it hasn't worked yet and were already seeing growing pockets rollover into deflation than threat is catastrophic for an over leveraged society!"

When you owe huge amounts of money you want your currency to go down in value so you can pay off your debts in a less valuable currency. That is what the world's policy makers want.

WHAT IS HAPPENING IS WE ARE CREATING CONDITIONS WHEREBY WE ARE IN A TRAP WE CAN NEVER GET OUT IF INFLATION FAILS TO MATERIALIZE. DEBT WILL BECOME TO LARGE AND EXPENSIVE TO ROLL OVER IF WE FALL INTO A DEFLATIONARY ENVIRONMENT "

... there is much, much more in this 25 minute video discussion.

SPECIAL GUEST HOST:JOHN RUBINO, Author & Publisher of DollarCollapse.com

DO UNINTENDED CONSEQUENCES & BREIXT MIX?

with John Rubino & Gordon T Long

Published 06-17-16

39 Minute VIDEO

What are the consequences of BREXIT? Maybe more importantly, what will happen when BREXIT mixes with already existing Unintended Consequences of Central Bank Policies?

Unintended Consequences: “How Do I Get Away From Negative Yields?”

BREXIT

The British campaign featured assertions and allegations tossed around with little regard to the facts. Both sides played to emotion, and the most common emotion played upon was fear.

The margin of victory startled even proponents of a British exit. The “Leave” campaign won by 52 percent to 48 percent. More than 17.4 million people voted in the referendum on Thursday to sever ties with the European Union, and about 16.1 million to remain in the bloc.

IMMIGRATION & EU'S FAILURE TO DEAL WITH THE REFUGEE PROBLEM

“Take control,” resonated with voters who feel that the government is failing to regulate the inflow of people from Europe and beyond.While leaders of the Leave campaign spoke earnestly about sovereignty and the supremacy of Parliament or in honeyed tones about “the bright sunlit uplands” of Britain’s future free of Brussels, it was anxiety about immigration — membership in the European Union means freedom of movement and labor throughout the bloc — that defined and probably swung the campaign.

IMMIGRATION PRESSURES ON SERVICES: With net migration to Britain of 330,000 people in 2015, more than half of them from the European Union, Mr. Cameron had no effective response to how he could limit the influx. And there was no question that while the immigrants contributed more to the economy and to tax receipts than they cost, parts of Britain felt that its national identity was under assault and that the influx was putting substantial pressure on schools, health care and housing.

TURKEY: The Leave side warned that remaining would produce uncontrolled immigration, crime and terrorism, with hordes pouring into Britain from Turkey, a country of 77 million Muslims that borders Syria and Iraq and hopes to join the European Union

EU POLITICAL SPILLAGE

But the damage won’t likely be isolated to the U.K., the world’s fifth-largest economy. “A Brexit victory will also signal victory for populism in Europe,” said Mr. Kirkegaard. “This referendum has unleashed fairly destabilizing elements into the European project.”

Anti-establishment and far-right parties in Europe, like the National Front of Marine Le Pen in France, Geert Wilders’s party in the Netherlands and the Alternative for Germany party will celebrate the outcome. The depth of anti-Europe sentiment could be a key factor in national elections scheduled next year in the other two most important countries of the European Union, France and Germany.

Mr. Cameron felt pushed into announcing the referendum in 2013 by the anti-Europe wing of his own party, amplified by concerns among other Tories that U.K. Independence Party and Mr. Farage were cutting too sharply into the Conservative vote.

SPECIAL GUEST:MIKE ("Mish") SHEDLOCK , Publisher of the Global Economic Analysis Blogspot.com

An espoused self educated Austrian Economist, Mike Shedlock / Mish is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Read more at MishTalk.com

MISH'S MONTHLY MACRO UPDATE

26 Minute Video

Mish Shedlock lays out some of the Key Macro Messages in his extensive writings over the last month.

Regular Co-Host:CHARLES HUGH SMITH , Author & Publisher of OfTwoMinds.com

with Charles Hugh Smith & Gordon T Long

31 Minutes - 21 Slides

Charles Hugh Smith and Gordon T Long share their thinking on current financial developments in China.

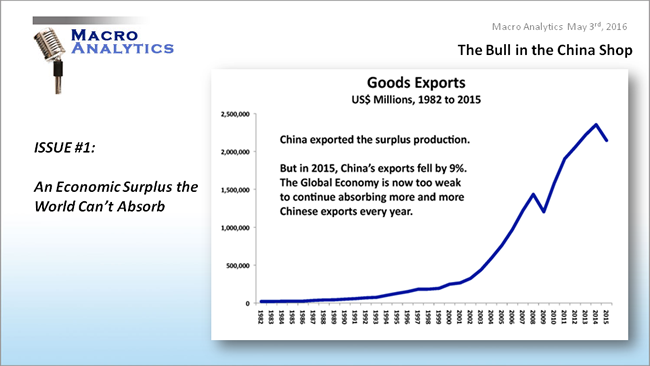

ISSUE #1 - The World Can No Longer Absorb China's Surplus

The good news is that China produces more than it consumes. This is the opposite of the US which consumers more than it produces.

The bad news is that the world can no longer absorb China's surplus (Production minus Consumption). Global trade has slowed dramatically impacting Chinese exports. The problem is further compounded since China as the new global economic engine, has become the dominate importer of other countries production.

The root cause stems from a "tapped" out American consumer and the "gutting" of the US middle class - the long time global economic engine.

This economic slowdown has left China with falling growth in FX reserves and has forced the selling of FX reserves to sustain elevated run-rates which were financing massive infrastructure expansion and investment. Construction has been a major employer and absorber of a growing Chinese worker force even though recently more and more have been employed building ghost cities and malls to keep workers employed.

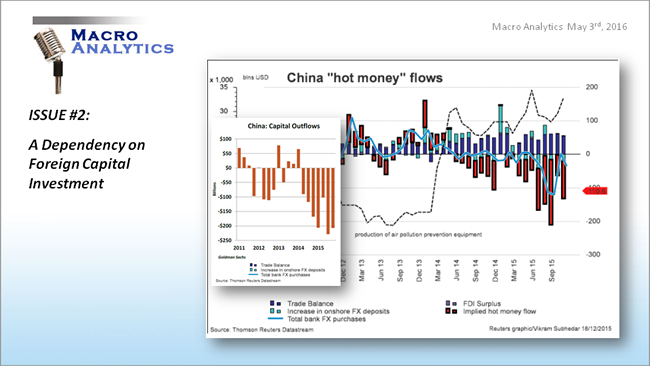

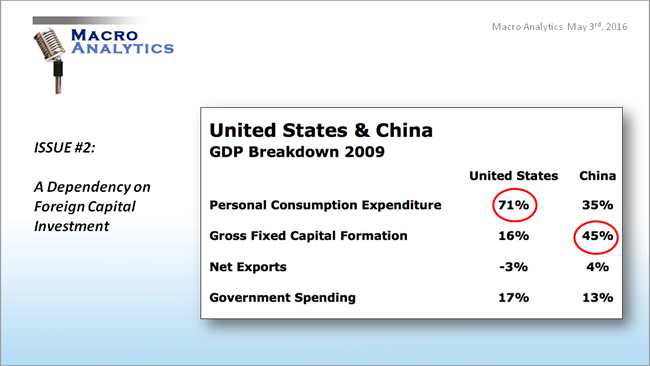

ISSUE #2 - Insufficent New Capital Formation

Additionally, Capital movement has reversed in China. China now faces a "capital flight" versus new Capital Formation coming into the country which has been powering the Chinese Manufacturing and Industrial explosion over the decade and half.

CONSEQUENCE - China Likely Needs to Devalue the Yuan

The consequence is that China needs to stop capital flight and increase exports and foreign capital investment the country is so dependent on.

China has only a limited number of options which Charles Hugh Smith and Gordon T Long spell with aid of 21 charts.

There is much, much more in this 31 minute video discussion.

SPECIAL GUEST:MIKE ("Mish") SHEDLOCK , Publisher of the Global Economic Analysis Blogspot.com

An espoused self educated Austrian Economist, Mike Shedlock / Mish is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Read more at MishTalk.com

MISH'S MONTHLY MACRO UPDATE

34 Minute Video

Mish Shedlock lays out some of the Key Macro Messages in his extensive writings over the last month.

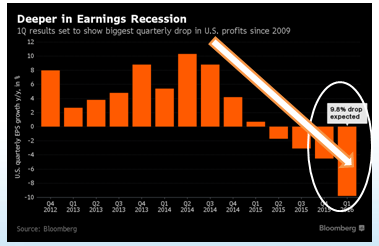

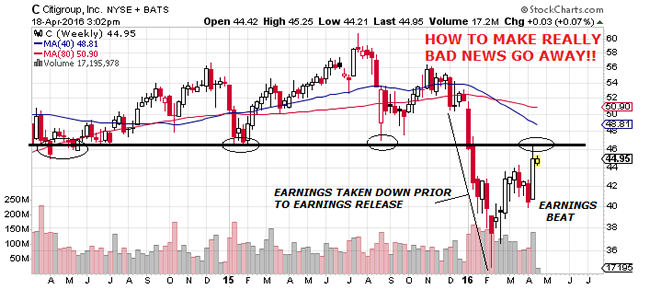

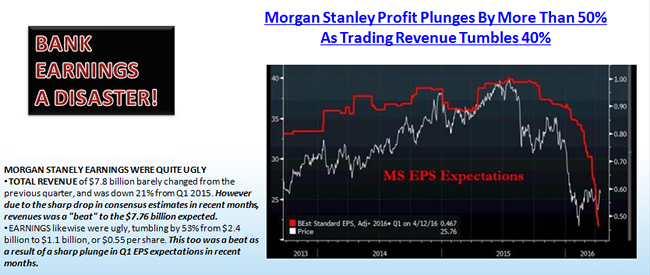

EARNINGS ACTUALLY MATTER? OR ARE THEY JUST TOO BAD TO IGNORE?

John Rubino

SPECIAL GUEST HOST:JOHN RUBINO, Author & Publisher of DollarCollapse.com

EARNINGS ACTUALLY MATTER?

OR ARE THEY

JUST TOO BAD TO IGNORE?

with John Rubino & Gordon T Long

Published 04-19-16

32 Minute VIDEO

Bank profits are in trouble!. Don't be fooled by the "beat analyst estimates" charade, because that is exactly what it is. First quarter bank earnings can only be described as an unmitigated disaster.

With the aid of 24 charts, John Rubino and Gordon T Long discuss what they see in this 32 minute video, what is important to be aware of and what is being hidden from public scrutiny.

THE EARNINGS' SEASON CHARADE

John Rubino recaps the situation as:

"I think this is hilarious so far! It is the season where banks are reporting earnings and they are reporting really bad numbers Y-o-Y. Citigroup's earnings were down 28% Y-o-Y with a double digit drop in revenue. It is pretty well the same for the Bank of America, JP MorganChase, Wells Fargo BUT the headline in Bloomberg and other major media outlets are oh "Citigroup beats expectations!"

That is the headline because Wall Street plays this game with their big client accounts where when things are headed south the analysts on Wall Street lower earnings projections even faster than earnings are actually dropping, so the companies can say "yes, we lost money and made less money than we did a year ago BUT we beat Wall Street expectations!". THAT becomes the headline.

The only positive headline out there for the big banks are when the results are horrendous! "

John goes on to say that:

"Year seven in a recovery banks should be reporting phenomenal numbers - they should be reporting 'blowout numbers! This is the point of the cycle when lots of people are borrowing, interest rates are down, funding is cheap for the banks - the bankS should be doing really well!" Instead, the banks are rolling over big time. Their earnings are probably (when all is said and done), they are going to be looking at a low single digit decline in Y-o-Y earnings."

"Finance at this late stage of Capitalism is now the biggest part of the economy, so you can't have banks shrinking, reporting losses or lower numbers Y-o-Y, laying people off or pulling back on lending and at the same time have a growing economy! They are mutually exclusive when banks are such a large part of the economy."

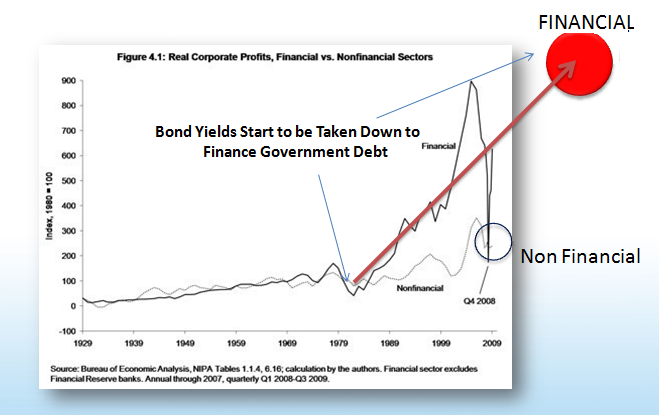

THE FINANCIALIZATION 'GIG' IS UP!

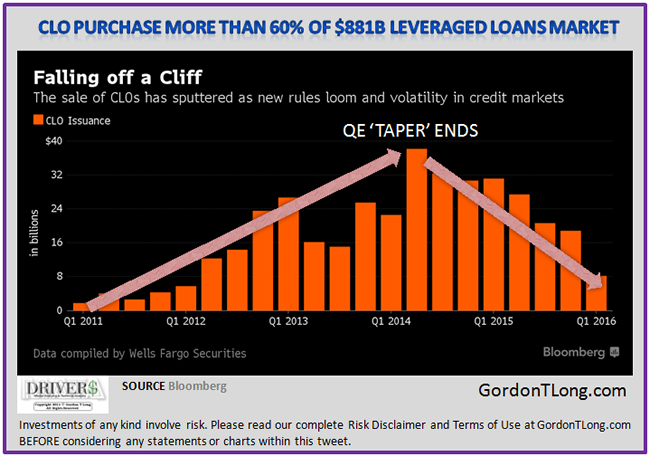

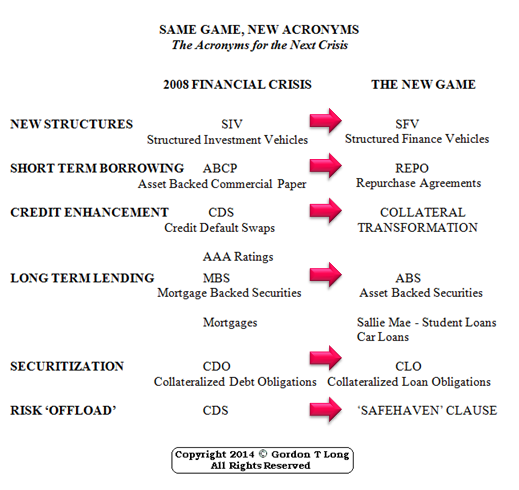

Gordon T Long illustrates that through the growth of Financialization, 45% of the equity markets today are Financials. Their spectacular earnings growth is historic and unprecedented and now excessive debt lending, encumbered collateral and rapidly growing non-performing loans are signalling troubles are looming.

Of particular concern to Gord is problems in the Leveraged Loans area which is critical to sustaining the growth in Collateralized Loan Obligations (CLOs) which has been steradily weakening. The Shadow Banking industry and bank earnings are critically tied to CLO growth and their extremely profitable fees.

Gord points out that it was the collapse of CDO's that brought the banking industry to its knees in 2008. One the acronyms have changed and the loan problem. It isn't CDO mortgages today but rather CLOs and Student Debt, Auto Debt and Corporate Leverage Debt.

.... there is much, much more in this fascinating 32 minute video exchange..

Financiers Skim Profits While Main Street Stagnates

Charles Hugh Smith

Regular Co-Host:CHARLES HUGH SMITH , Author & Publisher of OfTwoMinds.com

.

with Charles Hugh Smith & Gordon T Long

27 Minutes - 21 Slides

Charles Hugh Smith and Gordon T Long share their thinking on why the middle class in America has been experiencing a steady decline in their real standard of living over the last four decades and why the decline has recently accelerated. Their is a fundamental reason why productivity is falling while corporate profits soar and the employment participation rates falls.

THE "CRIPPLED" CAPITALIST SYSTEM

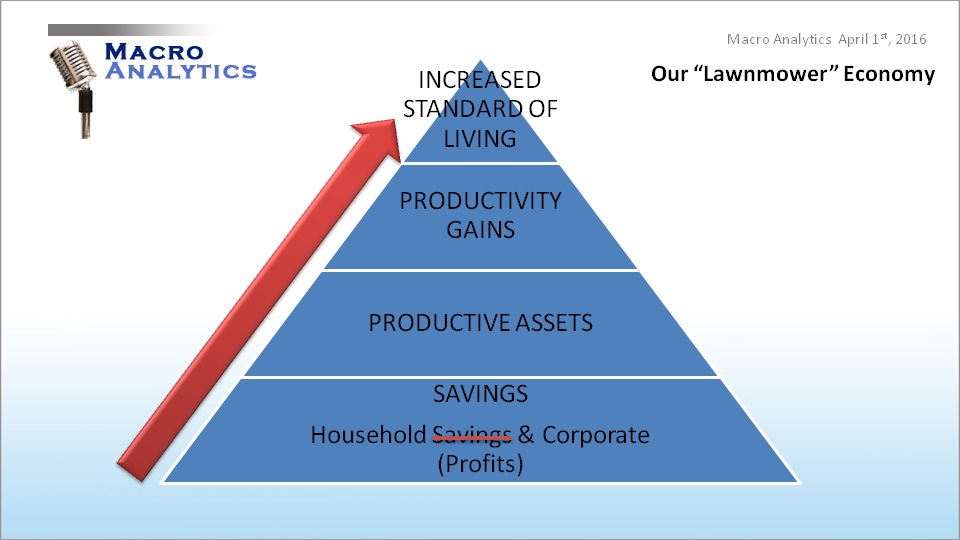

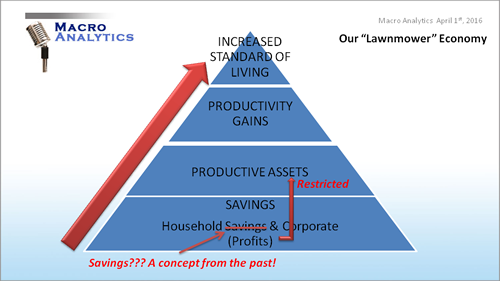

The Capitalist System is based on the construct that savings are invested into productive assets which increase productivty and in turn increase the standard of living of the whole society within which it operates. This mechanism has worked well for a century and and half. It no longer is working.

Savings come from two sources:

Household Savings

Corporate Profits

Today Household savings borders on being an extinct concept and what there is of it, is invested in financial securities. Therefore savings to be invested into productive assets comes primarily from corporate profits or "Wall Street" financing. We would argue that the capital is no longer flowing into productive assets but rather being directed to other venues which are unproductive and fail to increase the standard of living for society. Be assured how22$100M going to change in their lives?

In fact three approaches today are skimming billions of dollars of that "savings" from investment that will lead to rising standards of livings. This is one of the reasons that standards of living are falling for the vast majority of Americans.

Three of those major skimming mechanism are analysed in this video:

High Frequency Trading (HFT)

Stock Buybacks

The "Carry" Trade

A FINANCIALIZED ECONOMY FLOWS PROFITS TO THE FINANCIAL SECTOR

There is nothing wrong with making profits. However, there is something wrong in an economy when those profits don't flow into productive assets but rather "circularly" flow back into financial products.

THE FINANCIALIZATION "SKIM" IS KILLING THE MIDDLE CLASS IN AMERICA

This insidious and effectively "unsupervised" process has resulted in:

THE RESULTS

Falling Real Incomes

The Wealthiest Now Almost Eclusively ReapThe Benefits

The Middle Class Has Effectively Been "Gutted"

There is much, much more in this 27 Minute video discussion which is illustrated with 21 slides.

SPECIAL GUEST HOST:JOHN RUBINO, Author & Publisher of DollarCollapse.com

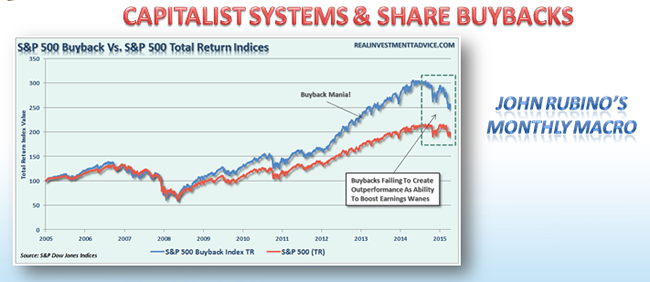

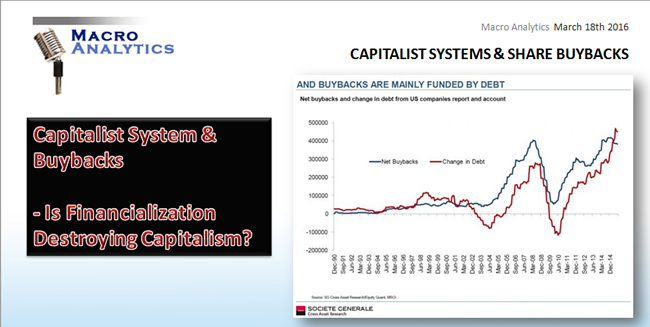

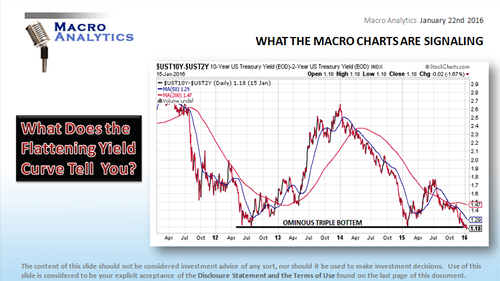

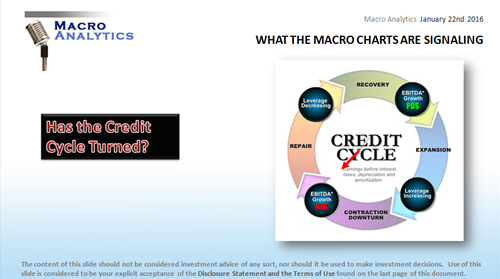

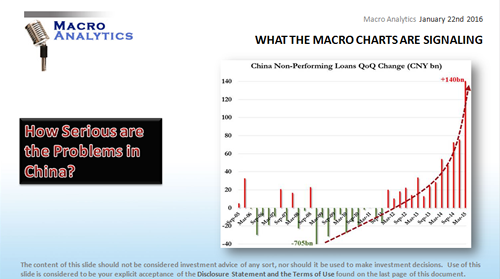

CAPITALIST SYSTEM & SHARE BUYBACKS

with John Rubino & Gordon T Long

Published 01-22-16

31 Minute VIDEO

John Rubino and Gordon T Long discuss concerns with the financial engineering strategy of stock buybacks and what impact it is having on the capitalist system. In this 33 minute discussion they additionally focus on current Macro Economic developments and announced policy changes in Global Monetary Policy.

Capitalist System & Buybacks - Is Financialization Destroying Capitalism?

Draghi's Latest Bazooka,

Japan's NIRP - Our Future?

What the US Primaries are Telling us about the Broken US Social Contract.

Capitalist System & Buybacks

Gordon T Long speculates on some surprising possibilities in answering the following:

Who is actually buying the bonds the corporations are issuing ?

Why - When they are getting more expensive?

How are they are doing it?

What does it say for the future of the Capitalist economic growth when all investment is going into buybacks and not into top-line growth and Capex Investment which is now considered "Risk"?

Is NIRP in the US' Future?

Are Government's Planning on Buying the Markets? (Are They Now?)

.... there is much, much more in this interesting 34 minute podcast discussion.

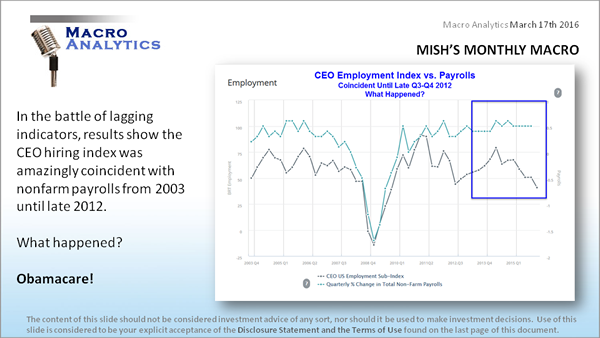

SPECIAL GUEST:MIKE ("Mish") SHEDLOCK , Publisher of the Global Economic Analysis Blogspot.com

An espoused self educated Austrian Economist, Mike Shedlock / Mish is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Read more at MishTalk.com

MISH'S MONTHLY MACRO UPDATE

34 Minute Video

Mish Shedlock lays out some of the Key Macro Messages in his extensive writings over the last month.

US Economy: Concerning Signals

Concerns with what Industrial Production, Consumer Spending and Inventories to Sales are telling us,

FOMC Meeting signals fewer and slower number of rate increases,

The End of the Obamacare Lift for Employment,

US Primaries Signal a Crisis in the US Social Contract.

Draghi's Statement Fallout: "This is end of all the Cuts We Can Do"

Euro reacts fairly significantly,

Concerns about EU Bank profits,

ECB to buy Corporate Bonds.

Strange Central Bank Policies: Confidence in Central Banks Becoming a Problem

What May be Coming,

Fiscal "Helicopter Money' and Guaranteed Minimum Incomes / Universal Income

Gold - Has Broken Key Overhead Resistance

Central Bank Policies of NIRP may be the catalyst,

Precious Metals rise in US dollars may be only in the early stages

Regular Co-Host:CHARLES HUGH SMITH , Author & Publisher of OfTwoMinds.com

.

with Charles Hugh Smith & Gordon T Long

29 Minutes - 21 Slides

Charles Hugh Smith and Gordon T Long take "a walk down memory lane" as they review six predictions they made during Macro Analytic shows between 2012 and early 2014. With 21 slides they also explain what they learned form what they got right and what they got wrong.

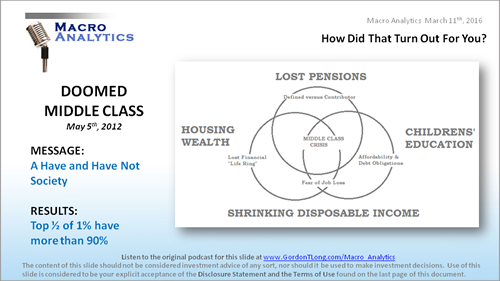

THE SIX PREDICTIONS

The Domination and Growth in Financialization,

The Doomed US Middle Class,

The Growth of Government Centralized Planning,

What is Wrong With Japan and Lessons We Should Learn,

What We Should Expect The Global End Game to Be,

The Coming Retail CRE Implosion.

THE BIGGEST THING THEY GOT RIGHT

The collapse of the US Middle Class was notably right.

THE RESULT

THE BIGGEST THING THEY LEARNED

It tends to take longer to unfold than you think it will and then it happens suddenly faster than you expect,

Never Underestimate what Governments and Central Bankers will do to maintain the status quo during times of distress.

There is much, much more in this 29 Minute video illustrated with 21 slides.

Regular Co-Host:CHARLES HUGH SMITH , Author & Publisher of OfTwoMinds.com

.

with Charles Hugh Smith & Gordon T Long

29 Minutes - 25 Slides

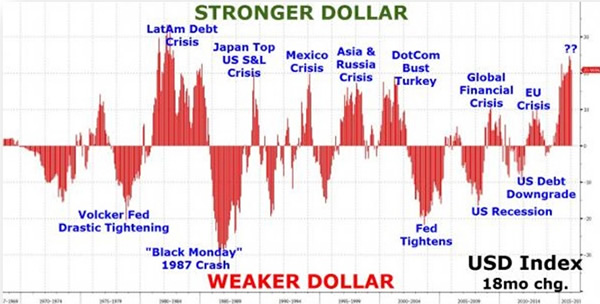

Charles Hugh Smith and Gordon T Long analyze, with 25 slides, the strength in the US Dollar and what we can likely expect going forward.

Both see a strong dollar in the future as it becomes, more and more a flight to safety associated with failed monetary / fiscal policies, weakening current accounts and slowing trade around the world. It isn't that the US$ is a paragon of virtue and value, but rather the "least ugly".

WHAT WE MIGHT EXPECT

1. A Strong dollar is killing global US corporate profits. This will continue to impact stock valuations,

2. Currency wars favor the US at this point. Global investors with billions to manage can still earn a yield in 30-year Treasury bonds, and yet they also get exposure to future appreciation vis a vis other currencies.

3. The stronger dollar (despite recent weakness) acts as a magnet for global capital, leaching capital out of emerging markets, China, Asia and Europe.

4. What happens in a full-blown currency crisis? If history is any guide, gold and the US dollar both soar as panicked investors seek safe havens.

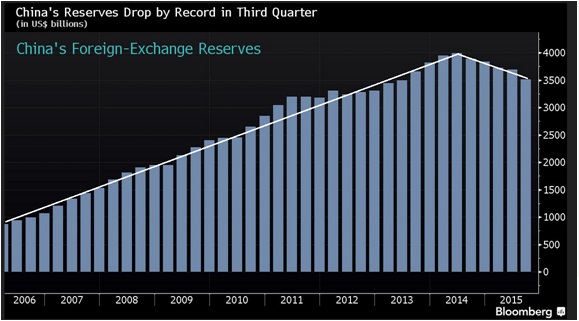

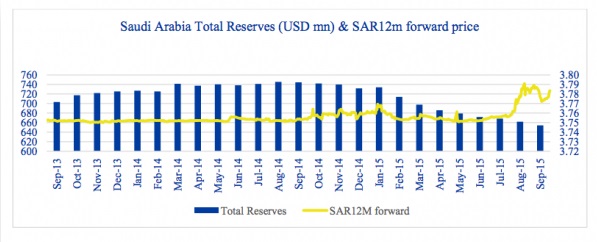

FALLING CURRENCY RESERVES

The collapse in commodity and energy prices, which can only be described as historic, is presently ravaging the current accounts of many countries dependent on the prices paid for these products. Many sovereign nations have been forced to sell currency reserves to protect their currencies.

CHINESE RESERVES

SAUDI RESERVES

The selling of Currency Reserves can clearly be seen in foreign holdings of US Treasuries which has been steadily eroding. Though selling of foreign reserves is temporarily contributing to a weakening US dollar it is likely only short term. In the longer term there is a shortage of reserves in many nations to sustain the current selling before they experience full blown currency dislocations. As global currency instabilities worsen, both video participants see the US dollar as best positioned currency to head higher as the recipient of a flight to "perceived" safety.

FAILING CURRENCY PEGS

Gordon T Long and Charles Hugh Smith both believe ailing Currency PEGs will increasingly take center stage with investors. The Hong Kong Dollar, the Chinese Yuan and the Saudi Arabia Riyal currencies are all focuses of traders and speculators, as are most of the energy exporter nations with a US$ PEG.

Individuals and businesses in five nations across central Asia, the Middle East and Africa are paying anywhere from 4 percent to 136 percent more than official exchange rates to get their hands on dollars. This is a growing tell tail sign as black market trading in the US$ is surging. These are signs of turmoil and a desire for "safety".

JAPAN'S NIRP HAS TRIGGERED SERIOUS DISRUPTIONS TO CAPITAL FLOWS.

According to Graham Summers at Phoenix Capital, Japan just lit the fuse on a $9 Trillion debt implosion. Hundreds of billions of Dollars in capital will begin fleeing Japan to come to the US.

• Bank of Japan implemented Negative Interest Rate Policy, or NIRP.

• It is the second Central Bank to do so.

• The European Central Bank or ECB first went to NIRP in June 2014.

• Thus, between Japan and Europe, over 20% of the world’s GDP is being managed by a Central Bank with NIRP.

• More importantly, TWO major currencies in the world are now at NIRP while the US Dollar is at 0.5%.

When the ECB went to NIRP it precipitiated the lift in the US$. The US Dollar has been in a bull market since mid-2014. It is not coincidence that it started when the Euro first went to NIRP, the minute the ECB implemented NIRP money began fleeing the Euro and moving into the US Dollar.

There is much, much more in this 29 Minute video illustrated with 25 slides.

This is an ominous development for the stock market and the economy. Corporate revenue growth has been negative for a while. Earnings are now down and cash flow has hit the skids. Debt continues to accelerate and pretty soon there will be major credit problems, especially in the energy sector.

Gordon Long: If You Think QE Was An Experiment, You Haven't Seen Anything Yet!

Jan. 14, 2016 6:44 AM ET

By FS Staff

Gordon Long, co-founder of Financial Repression Authority, believes that a massive tax grab by government at the federal, state, and local level is coming regardless of which candidate wins the 2016 US presidential election. He also discusses "a peak in the credit cycle," what this means for investors, and why the Fed may have to reverse course this year in light of a potential liquidity crisis.

"There's concern (and you're seeing it in the market from those who understand what's going on)...that because we have so much collateral pledged to support debt and credit right now," Gordon said, "that when that collateral falls in price as we're seeing in oil and commodities, you get margin calls and if you don't have the liquidity you're caught and you're caught in a serious problem."

I think what we're going to go through here in the first quarter is some kind of adjustment or correction-it's healthy...I can't imagine the market will be allowed to go much below 1820 on the S&P before the central banks will react with new policies and if you think quantitative easing was an experiment you haven't seen anything yet."

We are going to see negative interest rates potentially...we already have $5 trillion in bonds around the globe trading negative...there are all sorts of things that the central banks could do other than just interest rates and they will do them when the collateral is in jeopardy because it will bring down the entire system."

Scroll down for more of his comments or click to hear a preview of his interview below.

Gordon Long: "We've had a $30 trillion household net worth increase since 2009...while the government is facing huge issues of underfunded pensions, a baby boom retirement coming, drains on Social Security - so there's a lot of pressures on the government... to increase (taxes) significantly."

SPECIAL GUEST:MIKE ("Mish") SHEDLOCK , Publisher of the Global Economic Analysis Blogspot.com

An espoused self educated Austrian Economist, Mike Shedlock / Mish is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Read more at http://globaleconomicanalysis.blogspot.com

Regular Co-Host:CHARLES HUGH SMITH , Author & Publisher of OfTwoMinds.com

.

with Charles Hugh Smith & Gordon T Long

31 Minutes - 18 Slides

Charles Hugh Smith and Gordon T Long follow-up to their discussion last month of the puzzle of the falling US Civilian Labor Participation Rate. In this session they tackle the issues associated with "Universal Basic Income" which the public narrative has begun to 'offer up' as a solution.

PUBLIC NARRATIVE

"A Solution to Automation—Universal Basic Income for all“

The conventional wisdom is that a guaranteed free-money check from the central state is the solution. This is nothing more that "A Redistribution Scheme: A new form of Subsistence Serfdom"

• It doesn't address how this enormously costly program will be paid.

• It is Understood that the "Wealthy" will pay for it!

• Runs aground on the reality that upper-middle class and top 5% already pay 93% of all federal income taxes; they actually can’t afford more taxes.

• The top .01% who can afford to pay will continue to buy political protection of their income, and that’s not going to change:

-- A disaster for those getting the welfare check. They are essentially serfs, with no incentives or pathways to build capital.

For the Wealthiest - A Private Tax System That Saves Them Billions

-- ultimately, proponents of basic guaranteed income are relying on borrowing additional trillions of dollars to pay for the scheme. Not only is this financially unsustainable, it is immoral to load debt on future generations to pay for today’s spending.

1- The failed model of WELFARE-FOR-ALL - Communal Poverty

• The central-state welfare model

• Top-down, encouraging dependency and helplessness—and resentment

2- The Social-Economic model of SHARED BENEFITS flowing from working productively together

• The community economy

• Bottom-up, encouraging accumulation of capital, skills, etc.

• Creating the goods and services that are scarce and needed within local communities requires new ways of thinking and organizing work

SUBSISTENCE SERFDOM

• Giving people money without getting any productive work is destructive to participants,

• Those who have to pay for the free-riders (the community) loses the labor of its residents.

• Our goal should be to provide meaningful work to people in their own communities, not give them subsistence welfare,

• Guaranteed income for all is just a new form of subsistence serfdom.

• Those looking to central state “solutions” such as basic guaranteed income are out of touch with the reality that real solutions come from below, in the entrepreneurial Main Street economy, not from above (central banks, politicians enacting new social programs, etc.)

... and much, much more in this 31 minute frank and open discussion.

SPECIAL GUEST HOST:JOHN RUBINO, Author & Publisher of DollarCollapse.com

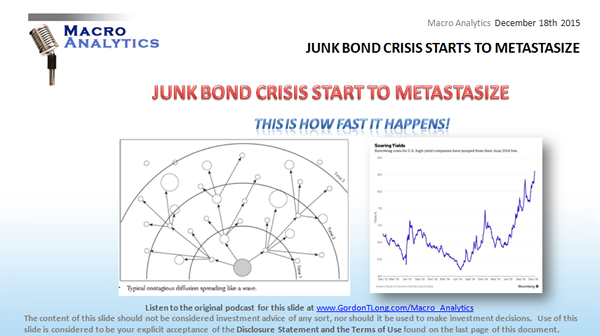

SOMETHING IS BURNING IN

HIGH YIELD CORPORATES!

with John Rubino & Gordon T Long

Published 12-18-15

31 Minute Video

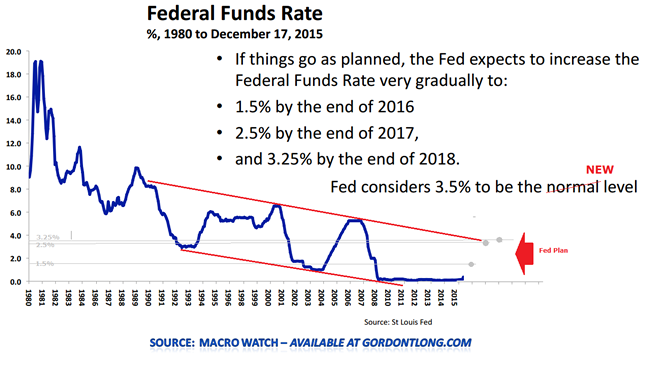

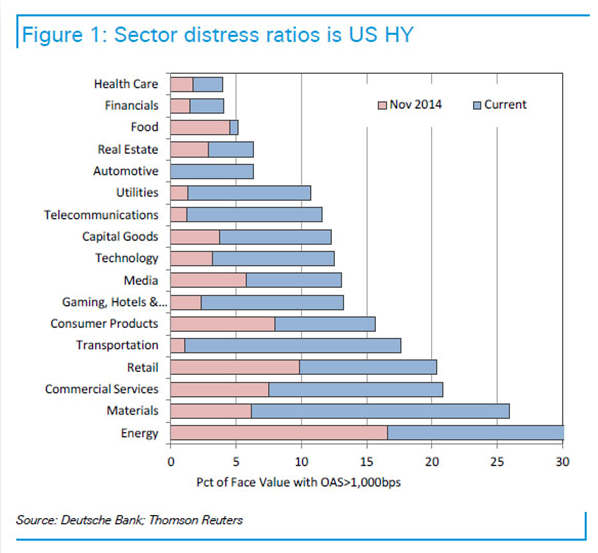

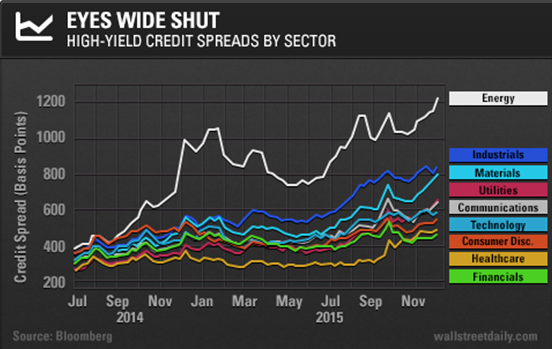

John Rubino and Gordon T Long discuss the alarming developments in the Junk (HY) Bond market. John was warning on his last appearance on Macro about the things he was seeing while Gord was warning of a turn he was seeing in the Credit Cycle. Both previous observations have proven correct so John and Gordon postulate what to expect next. It isn't pretty!

A HUGE POTENTIAL PROBLEM

Since the Financial Crisis the US Federal Reserve has increased its balance sheet by approximately $3.5 Trillion. In this same period the Junk Bond (HY) issuers have issued $2.2T of debt which the markets have 'gobbled' up to achieve yield. The question is what happens if they start selling some of that debt to avoid capital losses. This problem is compounded by regulations since the financial crisis which has significantly curtailed banks making markets in these instruments. Many worry that Investment Grade (IG) bonds also issued over the same period will be "infected", especially with a historic $1.3T being sold for the first time in 2015 to significantly fund stock buybacks and dividend payouts. This is a 'witch's brew' for a potential disaster.

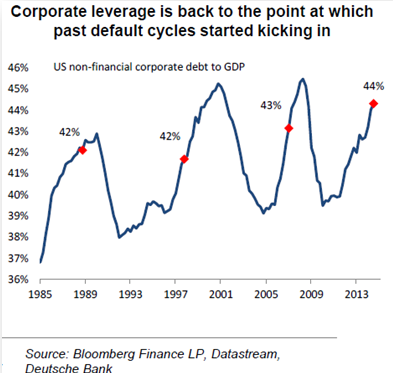

CORPORATE LEVERAGE

With Corporate Leverage back to the point at which past default cycles started kicking in, there are more reasons to worry, as corporate cash flow and EBITDA fall while the Federal Reserve raises rates.

Worsening cash flow to debt ratios normally force credit downgrades making credit more expensive and harder to get. This is coming at a time when major Junk Bond issuers in the Energy and Commodity sector are being hardest hit by falling pricing. They are trapped and investors know this and are now worried about junk bond liquidity.

A SLOWING GLOBAL ECONOMY

John and Gord both see a steadily deteriorating global economy which will bring further pressures to an already troubling situtation.

John lays out the torrent of bad news coming as the Fed begins raising rates:

The question is whether the Fed will be able to follow through with its stated policy direction.

WORRY OF CONTAGION

The problems in the Junk Bond market are not isolated to just the hard hit commodity and energy sectors. The protracted period of "easy money" created by Fed policy has sowed its seeds across all economic sectors.

A CRITICAL 90 DAY WINDOW

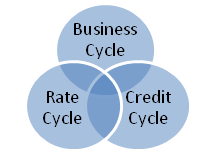

The next 90 days are going to be both quite worrying to investors and highly volatile for the financial markets, as the Credit Cycle, Rate Cycle and Business Cycle all send confusing signals before the future economic direction becomes clear.

Let's all hope that is not spelled: "Recession".

.... there is much, much more in this comprehensive 31 minute video discussion.

Regular Co-Host:CHARLES HUGH SMITH , Author & Publisher of OfTwoMinds.com

.

with Charles Hugh Smith & Gordon T Long

25 Minutes - 22 Slides

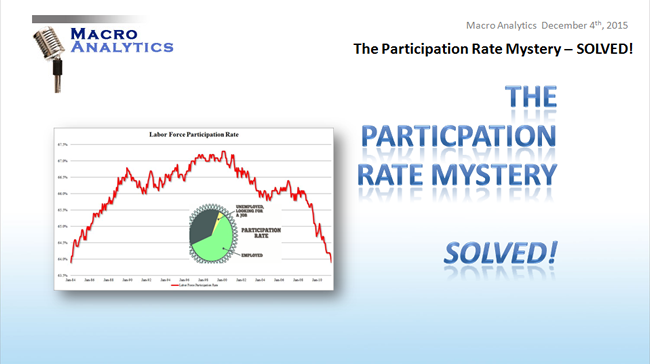

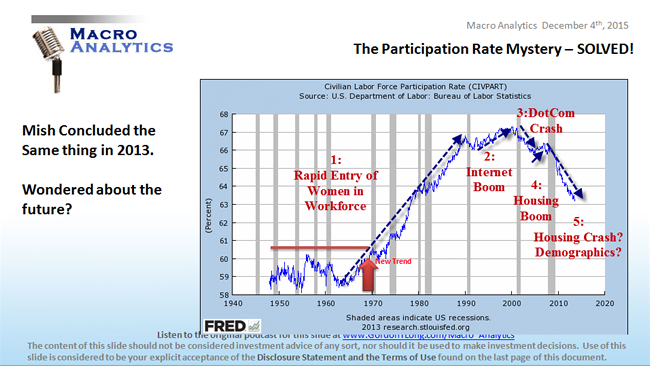

Charles Hugh Smith and Gordon T Long discuss the puzzle of the falling US Civilian Labor Participation Rate in which all the pundits express concern but few agree on what the root cause is.

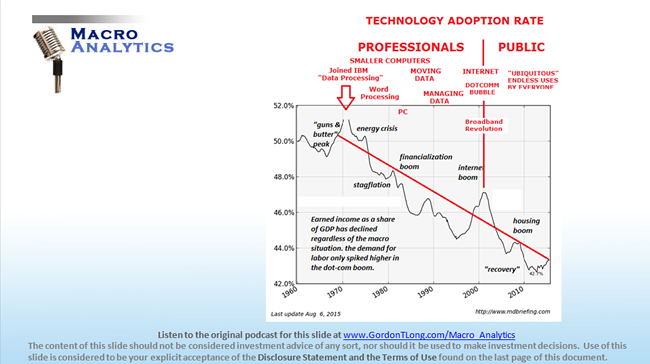

RELENTLESS TECHNOLOGY ADVANCEMENT - Gaining The Right Perspective

Together they show that it is instructive to start with the larger picture going back to 1970 when massive historic computer technology advancements truly began to be adopted.

Schumpeter's Creative Destruction was in full swing and accelerated as every industry was re-invented by labor saving technology. As this wave gained momentum real, family supporting full time jobs became scarcer while fewer equivalent paying new jobs were created when the ratio to population growth was properly factored in.

RAPID ENTRY OF WOMEN IN THE WORK FORCE DISTORTS COMPARISONS

Examining the actual participation rate chart from 1970 there is clear evidence of the initial rapid entry of women into the workforce. This surge distorts effective comparisons to today's developments and the cause of the more recent accelerating problem.

THREE KEY DRIVERS OF THE POST 2008 DECLINE

During the post 2008 financial crisis period, there has been at least three key drivers of the further acceleration in the decline of the US labor participation rate. This is in addition to the ubiquitous adoption of productivity enhancing technology and the effective de-industrialization of America:

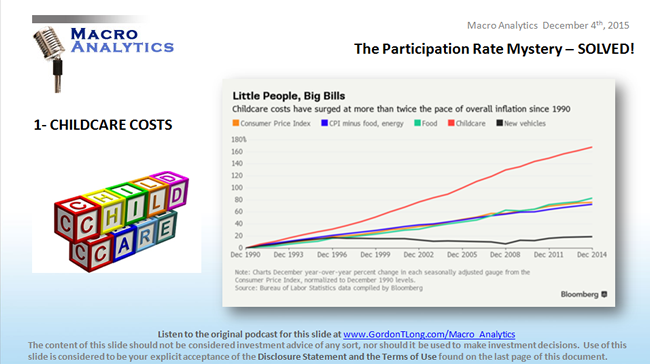

Childcare Costs & Forced Part Time Hours,

Labor Age Youth Unemployment and Growth of non-paying "Internships",

Rate of Job Obsolescence versus retraining opportunities.

... all of these drivers are discussed with insightful discussion on the subject with supporting graphics and illustrations. Listen below:

�

Thursday

November 19th

2015

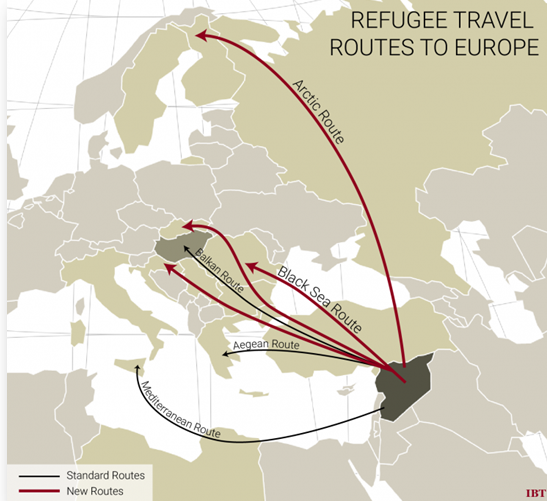

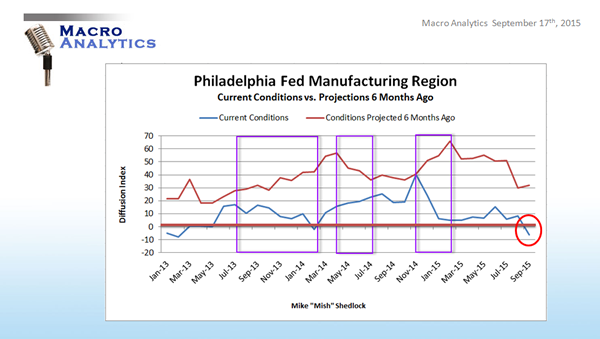

MISH SHEDLOCK talks: Paris Crisis and EU Refugee Problem, Japan 5th Recession, Possibility of a US Recession and the Coming Sub-Prime Auto Bust

"Mish" Shedlock

SPECIAL GUEST:MIKE ("Mish") SHEDLOCK , Publisher of the Global Economic Analysis Blogspot.com

An espoused self educated Austrian Economist, Mike Shedlock / Mish is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Read more at http://globaleconomicanalysis.blogspot.com

MISH'S MONTHLY MACRO UPDATE

30 Minute VIDEO

PARIS CRISIS & THE EU REFUGEE PROBLEM

Mish incredulously points out that Laurent Fabius, France’s foreign minister told France Info radio “If Abaaoud has been able to travel from Syria to France, it means that there are failings in the whole European system.” That there could be "failings in the whole European system" is shocking news? Just look at the policies and actions taken:

Chancellor Merkel and EU President Jean-Claude Juncker welcome refugees from war-torn countries with open arms.

Millions of refugees allowed entry.

Fake passports not detected.

Belgium, France and other countries allow citizens to go to Syria and fight alongside ISIS and return as if nothing meaningful transpired.

France receives multiple terrorist warnings from Turkey but ignores them.

Germany intercepts massive weapons cache headed for Paris but essentially does nothing.

Surely, at least one of those "strong controls" should have worked? Alas, things slipped through the cracks, and we are now faced with the shocking revelation by Laurent Fabius that there may be "failings in the whole European system."

"If there is one border that makes sense to close it is Greece and Turkey! Maybe also Turkey and Bulgaria!"

JAPAN'S FIFTH RECESSION

It may be the second under Shinzo Abe but this chart suggests it has been a Quintuple-Dip Recession. Abenomics has been a total failure, as expected..... but it did weaken the yen sending the stock market soaring!

Blooomberg Notes: "Weakness in business investment and shrinking inventories contributed to the contraction amid concerns over slower growth in China and the global economy that prompted Japanese companies to hold back on spending and production. While growth is expected to pick up in the current quarter, the GDP report could put pressure on Abe and Bank of Japan Governor Haruhiko Kuroda to boost fiscal and monetary stimulus.

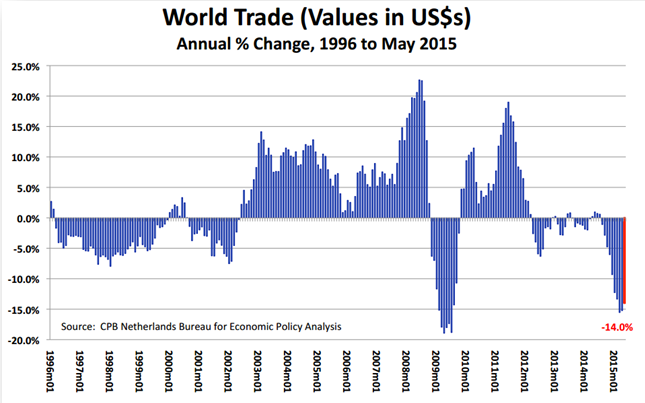

SLOWING GLOBAL ECONOMY & POSSIBILITY OF A US RECESSION

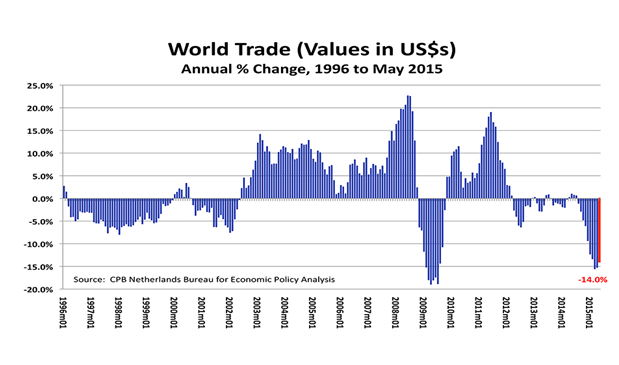

Global trade has slowed dramatically on a value basis (think corporate cash flows) and it is being felt on earnings and investment decisions!. US freight and shipping data suggests that slowing global trade has "washed ashore" in America.

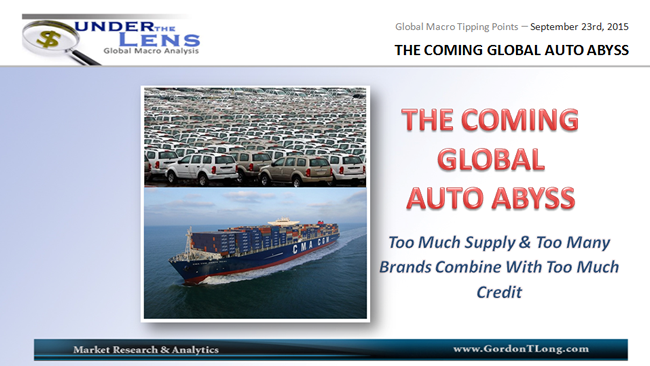

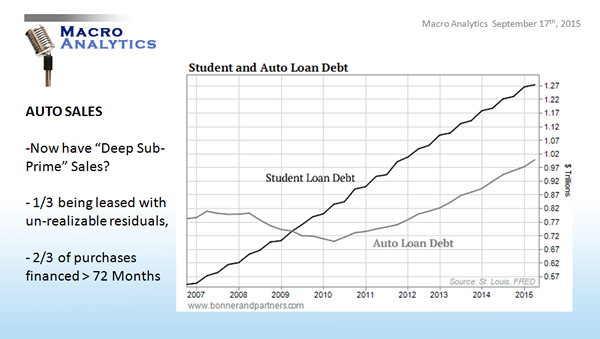

THE COMING SUB-PRIME AUTO BUST

"I have been surprised for sometime that the sub-prime auto party hasn't ended by now, and it hasn't! It is like the energizer bunny that just keeps on ticking" .....

"Typically banks react too late, after most of the damage has been done. It's the same every cycle. By the time credit is available to those on the bottom rung, the party is about over. Regardless, and as I have pointed out numerous times, the surge in autos is one of the few things holding up consumer spending and is also the only bright spot at all of manufacturing. What cannot go on forever won't. And it's nearly the end of the line for autos. Repercussions will be deeper than economists expect!"

Gordon T Long agrees with Mish's conclusions and in fact published this study and video for his subscribers in September:

....and there is much, much more, in this fast paced 30 minute Video.

�

AUDIO ONLY - choose an alternate listening

method...

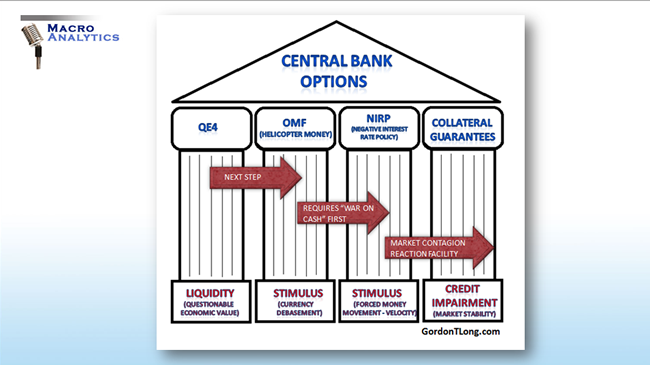

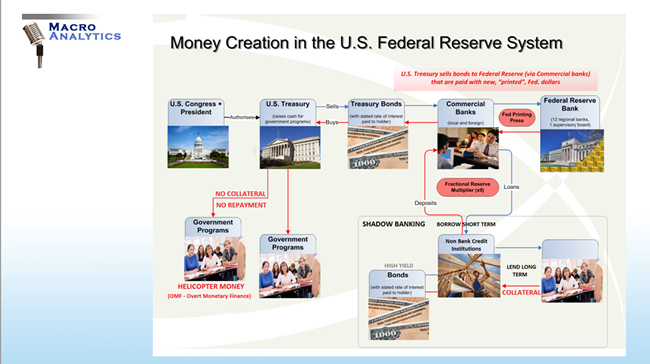

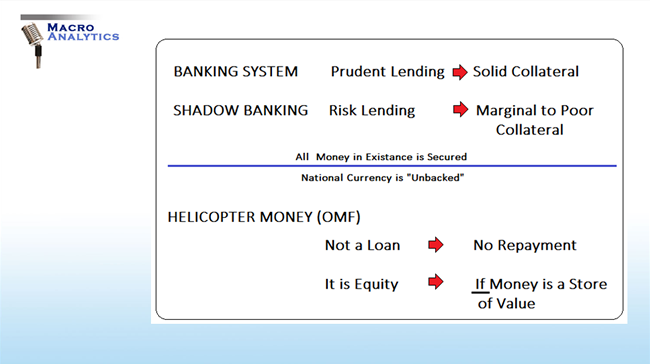

IS HELICOPTER MONEY, NIRP & COLLATERAL GUARANTEES IN OUR FUTURE?

John Rubino

SPECIAL GUEST HOST:JOHN RUBINO, Author & Publisher of DollarCollapse.com

IS HELICOPTER MONEY, NIRP &

COLLATERAL GUARANTEES IN OUR FUTURE?

with John Rubino & Gordon T Long

Published 10-17-15

30 Minute Video

John Rubino and Gordon T Long discuss the strong possibility of of a sequence of "QE4 for the People", Helicopter Money, NIRP and Collateral Guarantees now being in our economic future as the US and Global Economies rapidly slow. The evidence is clear for all to see, with little debate, except in the hallowed halls of the US Federal Reserve!

Gordon T Long argues that there are three cycles that must be closely monitored. Of the three, the Credit Cycle always leads and it has now turned. He believes the evidence shows that the Business Cycle has also turned and that the Rate Cycle has been disconnected from reality since it skipped a "Cyclical Beat" due to Central Bank Monetary Malpractice.

John Rubino agrees but believes no on should be surprised that the Business Cycle has turned and a recession is a real possibility after experiencing over 6 years of an apparent cyclical recovery. What is particularly ominous and unique about this slowdown he feels is that it is arriving during a period when we have:

1- HISTORIC LOW INTEREST RATES: Little conventonial Monetary Policy available to be a counter force mounting recessionary momentum.

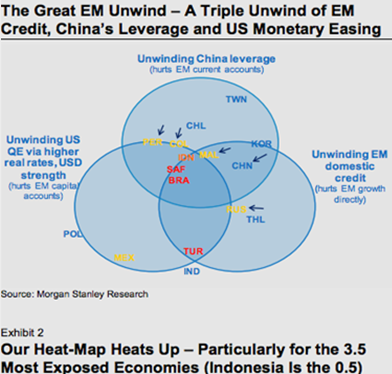

2-CHINA SLOWING DRAMATICALLY: China's massive build out and credit expansion since the 2008 Financial Crisis has powered Emerging & Frontier Economies. Now the Chinese economic engine is sputtering and by some measures is not growing at all,

2- A GLOBAL COMMODITY CRASH: We are in the midst of a major global commodity crash which is impacting corporate earnings, sovereign current accounts and employment,

3- GROWING WAGE PRESSURES IN THE US: Years of corporate profit increases without wage increases has left many corporations under fire and earnings pressures, most evidently seen with labor issues at WalMart,

4- REGIONAL PROBLEMS IN CHINA, JAPAN AND THE EU: Leaving no economy bright light for reversing the US Economic Slowdown.

"How do you have an equity bull market and a recovery in economic growth in general at a time when the main engine for growth (China) is sputtering and corporate profits (in the US in particular) are starting to turn down HARD? The answer is you don't! You can't grow under those circumstances."

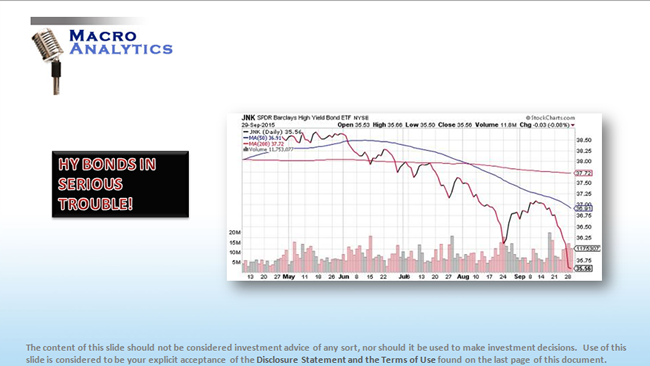

CANARY IN THE COAL MINE

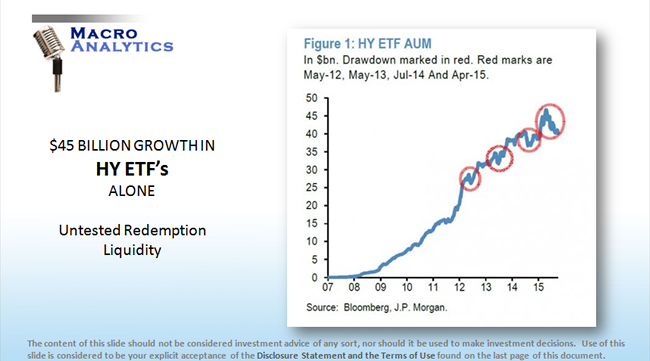

The dramatic collapse in HY (High Yield) Bonds is signaling serious problems for the continuation of cheap corporate funding. It also has the potential for contagion as liquidity is a problem when large amounts have been bid up on price due to the explosion is the use of ETF's to buy HY bonds.

BOTTOM LINE

As the UK Guardian newspaper recently declared:

"The world needs inventive responses. It needs a bigger reinvigorated IMF whose constitution should reflect the global balance of economy power and that can rescue the emerging markets. It needs western governments to launch massive economic stimulus centered on infrastructure spending. It needs new smart money policies that will allow negative interest rates."

This is exactly what is going to sell political in the coming year!

The bottom line is the central bankers of the world are now left with few choices and none are traditional approaches and the political pressures on them have almost pre-ordained the policies of: "QE4 for the People", Helicopter Money, NIRP and Collateral Guarantees to keep markets levitated.

"There is no political alternative but to 'double down' on existing policy approaches. The only alternative is austerity and we witnessed in one country after another in the EU what happens when this is attempted! ..... the only thing that will sell now is 'we are going to give you something'! "

.... there is much, much more in this 30 minute video discussion.

Friday

October 9th,

2015

IS HELICOPTER MONEY TO FOLLOW QE3?

Charles Hugh Smith

Regular Co-Host:CHARLES HUGH SMITH , Author & Publisher of OfTwoMinds.com

.

with Charles Hugh Smith & Gordon T Long

35 Minutes - 21 Slides

Charles Hugh Smith and Gordon T Long discuss the notion of "Helicopter Money" in the context of the following:

1- The What, Why and How of Helicopter Money,

2- Who is likely to be first off the pad?

3- The Recipients: The Expected Winners.

4- The Payers: The Expected Losers.

WHAT TO EXPECT GOING FORWARD - "QE for the People"

THE WHAT, WHY AND & HOW OF HELICOPTER MONEY

Support is growing around the world for increasing stimulus needs to be funded by “People’s QE.” The idea behind “People’s QE” is that central banks would directly fund government spending and even inject money directly into household bank accounts, if need be. As you would expect, the idea is catching on.

The European Central Bank is buying bonds of the European Investment Bank, an E.U. institution that finances infrastructure projects.

The new leader of Britain’s Labor Party, Jeremy Corbyn, is backing a British version of Helicopter Money.

You can count on it be very popular with the public.

Who will protest when the feds begin handing money to “mid- and low-income households”?

There is a serious problem however with this scheme as Gordon T Long points out. To him it signals the end and that we have crossed the Rubicon.

.. and much, much more of insightful discussion here!

�

.

AUDIO ONLY - choose an alternate listening

method...

SPECIAL GUEST HOST:JOHN RUBINO, Author & Publisher of DollarCollapse.com

STARK WARNINGS ON GLOBAL TRADE

with John Rubino & Gordon T Long

Published 09-25-15

24 Minute Video

John Rubino and Gordon T Long discuss the September FOMC decision, Brazil, Japan in the context of the large number and size of recent international bank layoff announcements. They talk about what is really going on here that no one wants to talk about publicly.

FOMC DECISION - An Incredibly Fragile Situation

Rubino says "It would have been a surprise if the Fed had raised rates! What is going out there is mostly pretty bad. The Fed is in a box right now and anything they do cares the potential for some sort of very serious unintended consequences.If they don't act in raising interest rates then that implies to the rest of the world that the Fed sees slow growth which scares the markets to do what they are doing(see chart to the right)."

"We are so leveraged right now that even a 'garden variety' equity bear market of -20% in the US and abroad cares the potential of pushing us into some sort of deflationary crash or 1930's style depression!"

"THE GUYS IN CHARGE HAVE NO IDEA WHAT TO DO! EXPECT A SHIFT TOWARDS RENEWED EASING.... ITS GOING TO BE 'BIGGER AND BADDER'.... 2016 is going to be a fascinating year for continued monetary experimentation."

We are currently seeing the build up in the intellectual framework from which this will happen.

BRAZIL

Brazil for a period of time was the Latin American country that initially got it right! They appeared to be on the verge of becoming a 'developed country' before it all fell apart. The US dollar spiked and Brazilian investment companies that had borrowed a lot of US dollars, investing them in high yielding Brazilian bonds of extraction oriented commodity companies. Now they are on the wrong site of the 'carry' with corruption concerns steadily surfacing.

"The corruption seems to have gone all the way to the top of the government! They have a political crisis as well as an economic crisis."

JAPAN

Japan has had the most aggressive debt monetization program of anyone in the world over the last three years where they basically tripled the balance sheet of the BOJ. It hasn't worked and Japan is not growing anymore! There inflation rate is basically zero and potentially dropping into deflation AFTER all this new money creation.

"It is clear what they do next, but proposals are now coming out of the woodwork from the easy money, Keynesian side of the spectrum which involves massive increases in money creation and government spending."

WE WILL SEE INTEREST RATES PUSHED TO NEGATIVE LEVELS IN MOST OF THE DEVELOPED WORLD AND CASH (ONE WAY OR THE OTHER) BE HOBBLED AS A STORE OF VALUE TO MAKE THAT HAPPEN!"

"For a long time global trade grew faster than GDP. More and more of our wealth was coming from trade. It turns out that most of that was do to China borrowing $15-$20 Trillion to snap up most of the global commodities. Everyone was getting richer on paper but that is turning out to be a mirage."

... there is much, much more in this 24 minute video discussion.

Tuesday

September 15th,

2015

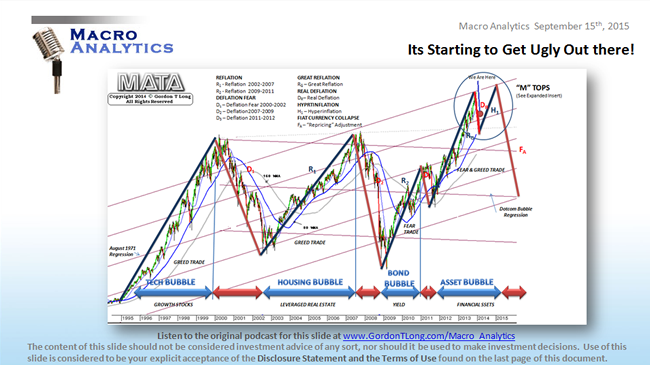

ITS STARTING TO GET UGLY OUT THERE!

Charles Hugh Smith

Regular Co-Host:CHARLES HUGH SMITH , Author & Publisher of OfTwoMinds.com

with Charles Hugh Smith & Gordon T Long

28 Minutes - 21 Slides

Charles Hugh Smith and Gordon T Long discuss the US Equity Market Technicals. They position the technical charts which they go thropugh in the context of the following primary sources of system risk to the markets:

1. Too much debt globally; public and private debt has skyrocketed since 2008.

2. Mal-investment due to perverse incentives: borrow money for stock buybacks rather than invest in new productive capacity, etc.

3. Stagnant income/revenues: households, companies and nations cannot support more debt

4. The rise of high-frequency trading (HFT) has increased the odds of flash crashes and instability

5. Rising U.S. dollar has triggered capital flight from emerging markets and China

6. China’s economy is grinding to a halt, crushing demand for commodities and commodity-dependent economies

7. Opaque banking: shadow banking in China, dark pools in offshore banking centers, etc. True totals of debt, leverage and quality of collateral are all unknown

8. Deteriorating collateral globally. How many of the 60 million empty “investment” flats in China can be sold for the purchase price? This is just one example of illiquid, impaired assets that are grossly overvalued.

JUST 3 POTENTIAL TRIGGERS

Gordon T Long takes the lead is laying out three technical market triggers that are currently at play, which he feels will significantly disrupt the markets and heighten volatility:

Have Entered a "Revenue Recession",

Cycle Timing,

Shifting Global Sentiment & Confidence

However, Gordon doesn't see this cyclical bull market to be quite over yet. Though he sees a scare coming in the near term, he feels the central bankers still have three arrows left in their quiver and until they are all fired the markets still have more room to run. He lays this out in his theory of an unfolding final "M" Top.

.. lots of charts here!

�

AUDIO ONLY - choose an alternate listening

method...

MISH SHEDLOCK talks: Fed Decision, The Illinois Saga and US Industrial Production

"Mish" Shedlock

SPECIAL GUEST:MIKE ("Mish") SHEDLOCK , Publisher of the Global Economic Analysis Blogspot.com

An espoused self educated Austrian Economist, Mike Shedlock / Mish is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Read more at http://globaleconomicanalysis.blogspot.com

MISH SHEDLOCK talks:

Fed Decision, The Illinois Saga and US Industrial Production

20 Minute VIDEO

FOMC DECISION -"Its All Actually Absurd!"

Mish had speculated that the Fed would likely hike 1/8th of a point at the critical September 17th FOMC meeting, but it turns out they didn't move at all. It appears that "The Fed is now going to delay so long that they may not even get in a rate hike!"

"Its all absurd to actually think that an 1/8 - 1/4 point hike is going to do anything other than perhaps put an end to the damage they have already done!"

"The Fed has blown this massive asset bubble and as soon as they hike and everything goes to h^&%ll, it isn't going to be because the Fed hiked, is is going to be because they didn't hike and encouraged and blew this asset bubble since March 2009!"

US DOLLAR REACTS & NEAR TERM SUPPORTCHANNEL

US INDUSTRIAL PRODUCTION -Bloomberg Ridiculously Suggests it is the Northeast?

Mish is stunned to read that Bloomberg is suggesting that the rapidly falling US Industrial problem appears to be centered in the northeast after the Dallas Fed, Kansas City Fed, Richmond Fed and the Empire State Manufacturing Report all showed serious deterioration within their economic regions for various reasons.

Auto's will soon have a used car glut as 1/3 of all cars are now on leases of 3 years or less! With all these cars financed through ABS (Asset Back Securities) within the Shadow Banking System it reminiscent of the 2008 Financial Crisis when housing residuals fell below their MBS values.

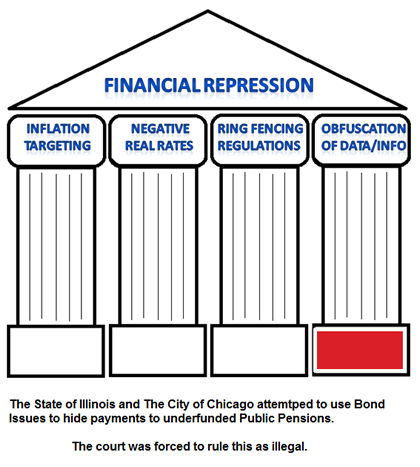

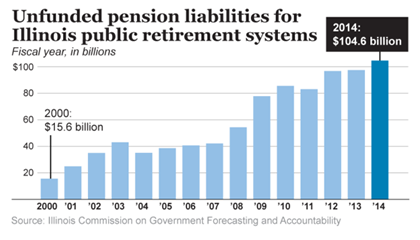

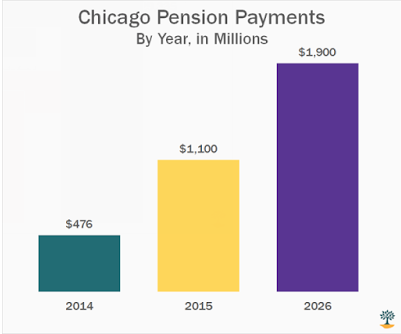

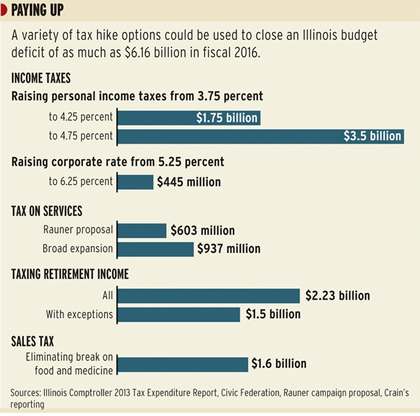

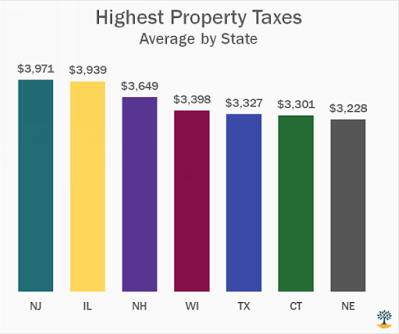

THE ILLINOIS SAGA - Special Political "Carve Outs" Circumvent Constitutional Budget Issues

"This year the Illinois legislature didn't even attempt to base a balanced budget. It was $8B out of whack and sent it on to Governor Bruce Rauner who refused to sign it. Illinois without a budget can't constitutionally pay its bills. Last year (almost like they knew this was going to happen) the legislature passed a "carve out" for THEMSELVES. No matter what happened the legislators would get paid. Now there is no pressure on them to produce a budget because they get paid anyway." Illinois facing the short term budgetary issue of not being able to pay the public schools additionally "carved out" an exemption for them to avoid the wrath of parents when kids couldn't return to school in September.

"We now have a stand off between the Governor and the Illinois legislators, but more and more bills are going unpaid. They recently stopped paying dentists and the next up are medical bills!"

....and much, much more, including a discussion o China in this fast paced 20 minute Video.

�

AUDIO ONLY - choose an alternate listening

method...

SPECIAL GUEST: PETER SCHIFF is CEO & Chief Global Strategist of Euro Pacific Capital.Peter Schiff is one of the few non-biased investment advisors (not committed solely to the short side of the market) to have correctly called the current bear market before it began and to have positioned his clients accordingly. As a result of his accurate forecasts on the U.S. stock market, economy, real estate, the mortgage meltdown, credit crunch, subprime debacle, commodities, gold and the dollar, he is becoming increasingly more renowned. He has been quoted in many of the nation’s leading newspapers, including The Wall Street Journal, Barron’s, Investor’s Business Daily, The Financial Times, The New York Times, The Los Angeles Times, The Washington Post, The Chicago Tribune, The Dallas Morning News, The Miami Herald, The San Francisco Chronicle, The Atlanta Journal-Constitution, The Arizona Republic, The Philadelphia Inquirer, and the Christian Science Monitor, and appears regularly on CNBC, CNN, Fox News, Fox Business Network, and Bloomberg T.V. His best-selling book, “Crash Proof: How to Profit from the Coming Economic Collapse” was published by Wiley & Sons in February of 2007. His second book, “The Little Book of Bull Moves in Bear Markets: How to Keep your Portfolio Up When the Market is Down” was published by Wiley & Sons in October of 2008.

Mr. Schiff began his investment career as a financial consultant with Shearson Lehman Brothers, after having earned a degree in finance and accounting from U.C. Berkeley in 1987. A financial professional for over twenty years he joined Euro Pacific in 1996 and has served as its President since January 2000. He is also Chairman of SchiffGold, a precious metals dealer based out of Manhattan. An expert on money, economic theory, and international investing, Peter is a highly recommended broker by many leading financial newsletters and investment advisory services. He is also a contributing commentator for Newsweek International and served as an economic advisor to the 2008 Ron Paul presidential campaign. He holds FINRA Series 4, 7, 24, 27, 53, 55, 63 & 65 licenses.

PETER SCHIFF talks

GOLD BACKED DEBIT CARDS

Published 08-25-15

A 21 Minute VIDEO

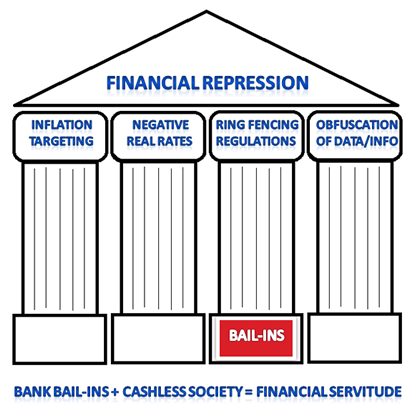

FINANCIAL REPRESSION

"Governments finds all sorts of ways of repressing their citizens and certainly do it for the banking system. In America today if you have a bank account you have no privacy anymore. Your banker is basically an unpaid spy working for the government trying to monitor your activities for anything suspicious so they can turn you into the government!"

"Inflation is a form of repression. If you save in the fiat currency the government creates, it will lose value over time as it orchestrates a deliberate plan of depreciation of the medium of exchange. So therefore you have continuous inflation. Of course to the extent you earn any money the government represses you by seizing a good portion of it with Income Tax, Inheritance Tax, The Payroll Tax etc. There all sorts of ways that the government seeks to repress us!"

BAIL-IN'S & A CASHLESS SOCIETY

Bail-ins are a function of government deposit schemes which really don't work! When these government insured banks fail, rather than having to just create a lot of money they will resort to the bail-in where they dispense the loses among the depositors. Actually (the later) is the right thing to do! We shouldn't have any government insurance for bank deposits! If you deposit your money in a bank and that bank fails, your deposits SHOULD BE at risk! In fact if we had deposits at risk we would have a much sounder banking system like we had before the invention of deposit insurance during the Roosevelt era!"

Peter Schiff points out that not all countries have these deposit schemes and the ones that don't have healthier banking institutions because now you have the market forces reigning in risky banking activity because "when people have to assume the risk of their deposits they do their homework! Banks then compete with each other based on SAFETY".

BITGOLD & EURO PACIFIC BANK

"I don't think bitcoin is going to work!"

"The fatal flaw of bitcoin is that there is no true intrinsic value there! There is nothing behind it, like when you have gold."

"People find it cumbersome. How do I spend my gold? It is very easy to spend it bitcoin but how do I spend gold? I solved that problem a few years ago at my bank (Euro Pacific Bank).. which is a 100% reserve bank that doesn't make any loans. We simply charge fees for our services."

"Right now our service is a prepaid service ... but what is coming is a one step process. BitGold copied what I was doing. They are now offering the same type of pre-paid debit card that I have been offering for three years."

"What I am doing, and this change will likely take place in the next 30-60 days is we will have the first true gold backed debit card!"

There is much more in this video on coming world of gold backed debit cards.

SPECIAL GUEST HOST:JOHN RUBINO, Author & Publisher of DollarCollapse.com

OPEN ACCESS

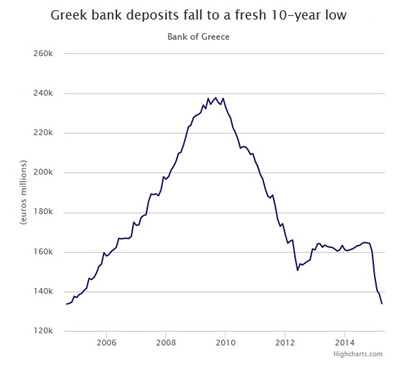

PUTTING THE PUZZLE OF GREECE TOGETHER

with John Rubino & Gordon T Long

Published 07-271-15

33 Minute Video

John Rubino and Gordon T Long discuss the current puzzling developments in Greece and the seemingly impossible choices facing the Greek people and their government.

THE ACCOUNTING CHARADE

To better understand how Greece and the EU found itself in this perplexing problem, John Rubino traces the history of Greece prior to joining the EU. John doesn't hold back in describing the manipulation of economic numbers carried out by Greece, abetted by Goldman Sachs to gain entry into the EU. Greece never met the Maastricht Treaty bar but nevertheless was granted entry. Goldman Sachs and the International Bankers were the big winners. In the short term so were the Greek people.

UNLIMITED SPENDING

John further goes on to detail how cheap money suddenly became available to Greece and the other poor peripheral countries. The exploding growth in debt to them was perceived and treated to be debt backed by the EU. John describes it as:

"It was like giving a teenager an unlimited credit card with no supervision. You should have expected nothing less!"

The situation in the EU with its peripherals was actually not to dis-similar to the bankers' "game plan" regarding US Agency debt (Fannie Mae and Freddie Mac) which were also perceived to be backed by the US government.

When these agencies got into serious financial trouble during the Financial Crisis the US government accepted the liabilities for these agencies and placed them in "conservatorship" thereby burdening US tax payers with the negligent lending practices they had callously incurred. EU tax payers are likewise being handed the bill for what can only be described as a wonderful party of staggering pension benefits and limited taxation for the Greek people and a lending bonanza for the bankers.

PARTY IS OVER AND THE HANGOVER BEGINS

The financing of the debt incurred cannot possibly be financed by Greece's economy nor absorbed by the EU, for fear that the other delinquent debtor nations will demand the same easy way out.

Of course what is happening here is the banks have made enormous profits on loans that should have never been made and are now sliding the responsibility to EU taxpayers.

Many Greeks see no real solution and therefore cash runs on the banks will continue to leave Greek banks insolvent as more money is fruitlessly pumped into them by desperate and naive EU officials.

... there is much, much more in this 33 minute video discussion.

Saturday

July 25th

2015

JEFF BERWICK talks CRYPTO CURRENCIES

Jeff Berwick

SPECIAL GUEST: JEFF BERWICK is a Canadian entrepreneur, libertarian and anarcho-capitalist activist who founded StockHouse Media Corporation in 1994, one of the most active financial website in Canada. He remained CEO until 2002. In 2013, Berwick announced plans to co-found the world's first Bitcoin automated teller machine (ATM). He presently resides in Acapulco, Mexico and is Chief Editor of THE DOLLAR VIGILANTE

JEFF BERWICK talks

CRYPTO CURRENCIES

Recorded 07-17-15

A 25 Minute Video Interview

Jeff Berwick, based in Acapulco, Mexico, has formerly been interviewed in this series (https://www.youtube.com/watch?v=O20n_oDUx54 ). He founded the StockHouse Media Corporation in 1994 and was its CEO until 2002. He is publisher of the dollar vigilante website (https://www.dollarvigilante.com/ ), which went online in 2010. Back then, he predicted the complete collapse of the US Dollar and the world financial system within the next five to ten years. He thinks that we are a lot closer now. He recently predicted a massive breakdown for September 2015 based on the seven year “Shemitah cycle“ (http://surviveshemitah.com/ ).

Jeff is concerned about the dependence of governments and financial market institutions on extremely low interest rates, even negative interest rates, which he calls “complete Keynesian insanity”. What is happening in Greece right now is just the beginning. It will eventually happen in other eurozone countries like Spain, Portugal, Italy, France and in countries all around the world, including the US.

Government debt in most countries has become so high that minor increases in the interest rate would lead to immediate default. The explicit US debt is above $18.3 trillion, as shown in the figure below. This however does not include implicit debt and liabilities that the US government has accumulated over the years, for example in the form of social security. Total debt and liabilities according to Jeff amount to $95 trillion.

“All it takes is, for example, for the Federal Reserve to raise interest rates by .25 per cent and they can bankrupt the entire financial system. This is where we are now. It’s been complete insanity. They tried to fix the 2008 crisis by printing money and going into more debt, which is why they got into that problem in the first place. And we are starting to see the next wave of major collapses and crises.”

As a response to the ongoing war on cash, Jeff suggests to go out of large cash holdings as soon as possible. He sees one potential solution in BitGold and even more so in Bitcoin, as a completely decentralized money and payment system. The price of bitcoin has been rising during the recent Greek crisis, whereas gold and silver have fallen. However, Jeff points out that the prices for gold and silver are systematically distorted on a “very manipulated market.”

“There is no Bitcoin office, there is no BItcoin servers. So no matter what the government does, unless they turn off the internet entirely, they can’t stop Bitcoin. That’s the beauty of Bitcoin.”

Although Mexico is often portrayed as a dangerous third world country, Jeff can tell from personal experience that it is in many respects a better place than the US, as there is far less government involvement in private and business affairs. Mexico will nonetheless face serious problems, because of their close economic ties to the US. The collapse of the American economy will inevitably spill over to Mexico.

“But I think people here [in Mexico] are more used to it. So, for example, they had their peso collapse in the 90s and people lived through it. But Americans aren’t ready for what’s coming. They haven’t seen it in their lifetime. And as you know, half the people in the US are on government assistance now, and a lot of those are on welfare and food stamps. When those EBT cards get shut down, I wouldn’t want to be anywhere near any major population center in the US.”

Jeff generally sees potential in other Latin and South American countries like Columbia, Chile and even Nicaragua, as well as some Asian countries, but definitely not in North America, Europe, Japan or Australia, which all share the same problem: the biggest cohorts of their populations looking for unsustainable entitlement payments in the near future.

AUDIO POST TEMPORARILY DELAYED

AUDIO ONLY - choose an alternate listening

method...

SPECIAL GUEST: GUILLERMO BARBA is a Mexican economist and financial blogger writing for Forbes Mexico. Barba is a follower of the Austrian school of economics.

GUILLERMO BARBA talks

FINANCIAL REPRESSION

Published 09-05-14

A 24 Minute PODCAST

A Mexican Economist, Guillermo Barba never heard of the Austrian school of economics until after graduating. Mexican University teaching still focuses on Marxist philosophy and Keynesian thinking. His subsequent exposure to the Austrian school of Economics was an eye opener which started him on a road which he hopes to help others in Mexico and Latin American become exposed to. He believes that the socialist thinking which South American universities are still oriented towards is one of the cancers in the world and hurting economic development.

"I became a real economist after I met the Austrian School of Economics!"

"The Austrian School has a framework to explain the current 'economic mess' in the world today!"

Barba's popular Mexican blog is focused on financial intelligence because he felt the truth was not being told and it needed to be.

FINANCIAL REPRESSION

"Mexicans know perfectly what Financial Repression means! Living in Mexico means living in the neighborhood of the United States of America. That is a lot of financial repression!"

"The entire world is suffering from Financial Repression because there are Financial Repressors. That is the problem. Who are those financial repressors? As Hugo Salinas Price told him, the entire world is controlled by a group of about 1000 people and a smaller core group control most of the decisions. Most of them are bankers"

Barba believes that t he global reserve system which is based on the US dollar "is basically a scam". According to Barba, to keep the whole system working the powers to be must get people into debt. Debt must grow exponentially.

IMPORTANCE OF SAVINGS

"Pushing people to spend and taken on debt versus savings is insane! Savings is the base and the cornerstone of development. Savings are the cornerstone of capital! The world needs capital accumulation, not debt accumulation!

"Debt accumulation is not sustainable. Capital accumulation is sustainable!"

Guillermo Barba believes the powers to be simply don't know what to do other than just 'print more money'. He also sees the US dollar getting much, much stronger as people generally won't know what to do to protect their wealth. This will offer opportunities to use inflated US dollars to buy real estates at attractive prices.

..... there is much more in this interview on the Mexican and South American economies.

�

AUDIO ONLY - choose an alternate listening

method...

SPECIAL GUEST: DAVID MORGAN: Seduced by silver at the tender age of 11, David Morgan started investing in the stock market while still a teenager. A precious metals aficionado armed with degrees in finance and economics as well as engineering, he created the Silver-Investor.com website and originated The Morgan Report, a monthly that covers economic news, overall financial health of the global economy, currency problems ahead and reasons for investing in precious metals.

David considers himself a big-picture macroeconomist whose main job as education—educating people about honest money and the benefits of a sound financial system—and his second job as teaching people to be patient and have conviction in their investment holdings. A dynamic, much-in-demand speaker all over the globe, David’s educational mission also makes him a prolific author having penned "Get the Skinny on Silver Investing" available as an e-book or through Amazon.com. As publisher of The Morgan Report, he has appeared on CNBC, Fox Business, and BNN in Canada. He has been interviewed by The Wall Street Journal, Futures Magazine, The Gold Report and numerous other publications. Additionally, he provides the public a tremendous amount of information by radio and writes often in the public domain.

DAVID MORGAN TALKS SILVER

Published 07-17-15

A 32 Minute Video

An Aeronautical Engineer by training, David brings these analytic skills to his analysis of financial and commodities markets. He believes the inability of the majority of people to properly understand the significance of mathematical science such as the exponential curve is one such important example. A "hockey stick" of debt growth is simply and fundamentally unsustainable!

FINANCIAL REPRESSION

Keeping interest rates low is central to debt ridden governments surviving. Acording to David Morgan the government must keep rates low as long as possible but believes a reset of some sore is inevitable. David sees the mechanics and policies of keep rates repressed as fundamentally defining Financial Repression.

Financial Repression is like a big coffee press, pressing everything down and has suppressed the ability for us to have a free market and thereby enjoy the fruits of our intellect, labor, creativity and purpose as humans."

POTENTIAL RISING INTEREST RATES

Many believe that rising interest rates will hurt gold. David fully expects the Fed to increase rates but sees it as being nothing more that "showmanship". David suggests that:

"his experience shows that it is when REAL RATES get positive that you COULD see gold impacted from an increase in interest rates"

"What you really need to know is what are the real rates versus nominal rates which you see iin the newspapers."

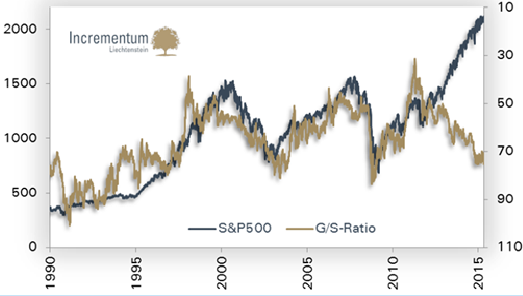

GOLD-SILVER RATIO

The current gold-silver ratio implies to David Morgan is that silver is presently undervalued relative to gold.

According to Morgan the Gold-Silver Ratio is telling us something else that is important.

"If you have a real economy with sound money you get a deflationary trend. This means your money is worth more over time. It is beneficial to almost everybody. Silver is the best inflation edge and not the best deflation hedge. Gold is the best deflation hedge. Silver anticipated this huge inflationary environment back when QE2 was announced and moved from $26/OZ to $48/OZ. What happened was all that anticipated inflation didn't get into the market place because all the increased debt only resulted in re-liquifying the banks. They forced the money into the banking system and not out into the public sector."

David believes silver is currently a better buy than gold. He still believes silver will outperform gold.

"We are not out of the woods. There is a place for precious metals in your portfolio. 20% for "metal bugs" and 10% for the average public."

There is much, much more in this 32 minute interview with this well respected precious metals and silver expert.

SPECIAL GUEST:James Turk has specialized in international banking, finance and investments since graduating in 1969 from George Washington University with a B.A. degree in International Economics. His business career began at The Chase Manhattan Bank, which included assignments in Thailand, the Philippines and Hong Kong. He subsequently joined the investment and trading company of a prominent precious metals trader based in Greenwich, Connecticut. He moved to the United Arab Emirates in December 1983 to be appointed Manager of the Commodity Department of the Abu Dhabi Investment Authority, a position he held until resigning in 1987. Since 1987 James Turk has written The Freemarket Gold & Money Report, an investment newsletter that publishes twenty issues annually. He is the author of The Illusions of Prosperity (1985), SOCIAL SECURITY Lies, Myths and Reality (1992) and several monographs and articles on money and banking. He founded GoldMoney.com based on two US patents awarded to him for digital gold currency, which enables gold to circulate efficiently as currency.

JAMES TURK on FINANCIAL REPRESSION

24 Minute VIDEO

With a career in International Banking, including managing the Abe Dubai Investment Authority's Commodities Portfolio, James Turk is an experienced professional who's insights should be thoughtfully considered. He feels strongly that the US needs to return to the sound money principles the framers of the US Constitution outlined and which the US has unfortunately and perilously veered away from.

FINANCIAL REPRESSION

"Financial Repression is government intervention in the market system which distorts the market's signals. .... Government intervention not only distorts the markets but in fact is counter-productive because many times it is government policies which the market are reacting to!"

Instead of changing the policies, governments try and convince the markets (through intervention) that the policies they are following are the correct ones, when in fact they are not.

James feels strongly that governments need to be outside the markets and be primarily focused on maintaining the 'rule of law' and ensuring there is a level playing field for competitive capitalism to operate on. Government intervention results in distorting that playing field to the advantage of themselves and their special interests.

"(Governments & Central Banks) are following policies that basically are not sustainable!"

"The government's 'make believe' is that they are creating wealth through creating currency and distributing it through their various programs. That is not creating wealth, but rather debasing the currency. When you debase the currency this is the worst type of financial repression because you are essentially destroying peoples ability to interact entirely voluntarily within the market place, as we fulfill our needs and wants."

UNDERSTANDING WEALTH