|

JOHN RUBINO'SLATEST BOOK |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

"MELT-UP MONITOR "

Meltup Monitor: FLOWS - The Currency Cartel Carry Cycle - 09 Dec 2013 Meltup Monitor: FLOWS - Liquidity, Credit & Debt - 04 Dec 2013 Meltup Monitor: Euro Pressure Going Critical - 28- Nov 2013 Meltup Monitor: A Regression-to-the-Exponential Mean Required - 25 Nov 2013

|

![]()

Â

"DOW 20,000 "

Lance Roberts Charles Hugh Smith John Rubino Bert Dohman & Ty Andros  |

Â

HELD OVER

Currency Wars

Euro Experiment

Sultans of Swap

Extend & Pretend

Preserve & Protect

Innovation

Showings Below

Â

"Currency Wars "

|

Â

"SULTANS OF SWAP" archives open ACT II ACT III

ALSO Sultans of Swap: Fearing the Gearing! Sultans of Swap: BP Potentially More Devistating than Lehman! |

Â

"EURO EXPERIMENT"

archives open EURO EXPERIMENT :Â ECB's LTRO Won't Stop Collateral Contagion!

EURO EXPERIMENT: |

Â

![]()

"INNOVATION"

archives open |

Â

"PRESERVE & PROTE CT"

archives open |

Â

Weekend Mar. 8th, 2014

![]()

Follow Our Updates

on TWITTER

https://twitter.com/GordonTLong

AND FOR EVEN MORE TWITTER COVERAGE

Â

STRATEGIC MACRO INVESTMENT INSIGHTS

2014 THESIS: GLOBALIZATION TRAP

2014 THESIS: GLOBALIZATION TRAP

NOW AVAILABLE FREE to Trial Subscribers

185 Pages

What Are Tipping Poinits?

Understanding Abstraction & Synthesis

Global-Macro in Images:Â Understanding the Conclusions

Â

| Â | Â | Â | Â | Â |

| MARCH | ||||||

| S | M | T | W | T | F | S |

| Â | Â | Â | Â | Â | Â | 1 |

| 2 | 3 | 4 | 5 | 6 | 7 | 8 |

| 9 | 10 | 11 | 12 | 13 | 14 | 15 |

| 16 | 17 | 18 | 19 | 20 | 21 | 22 |

| 23 | 24 | 25 | 26 | 27 | 28 | 29 |

| 30 | 31 | Â | Â | Â | Â | Â |

KEY TO TIPPING POINTS |

| 1 - Risk Reversal |

| 2 - Japan Debt Deflation Spiral |

| 3- Bond Bubble |

| 4- EU Banking Crisis |

| 5- Sovereign Debt Crisis |

| 6 - China Hard Landing |

| Â |

| 7 - Chronic Unemployment |

| 8 - Geo-Political Event |

| 9 - Global Governance Failure |

| 10 - Chronic Global Fiscal ImBalances |

| 11 - Shrinking Revenue Growth Rate |

| 12 - Iran Nuclear Threat |

| 13 - Growing Social Unrest |

| 14 - US Banking Crisis II |

| 15 - Residential Real Estate - Phase II |

| 16 - Commercial Real Estate |

| 17 - Credit Contraction II |

| 18- State & Local Government |

| 19 - US Stock Market Valuations |

| Â |

| 20 - Slowing Retail & Consumer Sales |

| 21 - China - Japan Regional Conflict |

| 22 - Public Sentiment & Confidence |

| 23 - US Reserve Currency |

| 24 - Central & Eastern Europe |

| 25 - Oil Price Pressures |

| 26 - Rising Inflation Pressures & Interest Pressures |

| 27 - Food Price Pressures |

| 28 - Global Output Gap |

| 29 - Corruption |

| 30 - Pension - Entitlement Crisis |

| Â |

| 31 - Corporate Bankruptcies |

| 32- Finance & Insurance Balance Sheet Write-Offs |

| 33 - Resource Shortage |

| 34 - US Reserve Currency |

| 35- Government Backstop Insurance |

| 36 - US Dollar Weakness |

| 37 - Cyber Attack or Complexity Failure |

| 38 - Terrorist Event |

| 39 - Financial Crisis Programs Expiration |

| 40 - Natural Physical Disaster |

| 41 - Pandemic / Epidemic |

Â

Reading the right books?

No Time?

We have analyzed & included

these in our latest research papers Macro videos!

![]()

OUR MACRO ANALYTIC

CO-HOSTS

John Rubino's Just Released Book

![]()

Charles Hugh Smith's Latest Books

![]() Â

Â

![]() Â

Â

Our Macro Watch Partner

Richard Duncan Latest Books

MACRO ANALYTIC

GUESTS

F William Engdahl

![]() Â

Â

![]() Â

Â

![]() Â

Â

![]() Â

Â

![]() Â

Â

OTHERS OF NOTE

![]()

![]()

![]()

![]()

Book Review- Five Thumbs Up

for Steve Greenhut's

Plunder!

![]()

Â

|

We post throughout the day as we do our Investment Research for: LONGWave - UnderTheLens - Macro |

||||||

"BEST OF THE WEEK "

|

Posting Date |

Labels & Tags | TIPPING POINT or 2013 THESIS THEME | |||

HOTTEST TIPPING POINTS |

|  | Theme Groupings |

|||

| Â | Â | Â | ||||

MARKET RISK - Everyone on the Same Side of the Boat! There isn't much 'runway' left on a chart like this! Maybe a quarter? Likely a spring or early summer market shock.

|

|  | 1 - Risk Reversal | |||

HOUSING - Serious Housing & Household Spending Headwinds. |

|  | 15 - Residential Real Estate - Phase II | |||

EMERGING MARKETS - Emerging World Poses More Danger Than in 1990s Emerging World Poses More Danger Than in 1990s 03-06-14 Morgan Stanley via Bloomberg Developed economies are less resilient to an emerging-market shock than they were in the 1990s, when crises from Thailand to Russia rattled investors without triggering a global recession. Thatâs according to an 81-page study released March 5 by Morgan Stanley economists and strategists. They estimate a 1990s-style slump in emerging-market demand would create

Reasons for the greater vulnerability include the fact that

The Federal Reserve and the Bank of Japan probably would respond by easing monetary policy, lowering commodity prices and bond yields as a result. That would help revive growth, although the recovery would be weak, they said. âIf an emerging-market shock materializes, we believe the impact on developed markets could be stronger than it was in the late 1990s and would most likely last longer,â the Morgan Stanley team wrote. The study is based on a scenario in which:

Europeâs equity markets would be the most adversely affected among global stocks given its companies have derived 65 percent to 80 percent of their revenue growth from emerging markets in recent years. Â STRATEGIC MACRO INVESTMENT INSIGHTS What is important in the Morgan Stanley work above is:

We have written extensively to our subscribers about the Echo Boom and this is exactly what Morgan Stanley is now actually assessing.

THE FINANCIAL MARKETS - Macro AnswersIn LNG WARS: The Ukraine & Syrian Choke Points we stated: Regarding our oil and gas trading, here is the central Macro Driver$ / Trigger$ / Bia$ issue we are grappling with at Trigger$: See TRIGGER$ for Daily and 60 Minute Charts for HPTZ targets

We see a major inflection point coming near term at our Macro Trigger$ Zone "E" (see chart above and table right). After a three year consolidation the question is which way it will break? The answer lies in the MACRO Analysis.

|

|  | 25 - Oil Price Pressures | |||

| MOST CRITICAL TIPPING POINT ARTICLES THIS WEEK - March 2nd - March 9th | Â | Â | Â | |||

| RISK REVERSAL | Â | Â | 1 | |||

| JAPAN - DEBT DEFLATION | Â | Â | 2 | |||

| BOND BUBBLE | Â | Â | 3 | |||

EU BANKING CRISIS |

|  | 4 |

|||

| SOVEREIGN DEBT CRISIS [Euope Crisis Tracker] | Â | Â | 5 | |||

| CHINA BUBBLE | Â | Â | 6 | |||

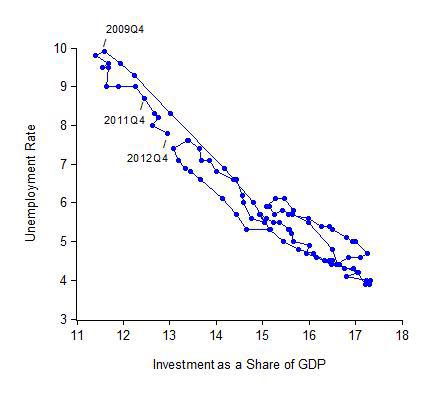

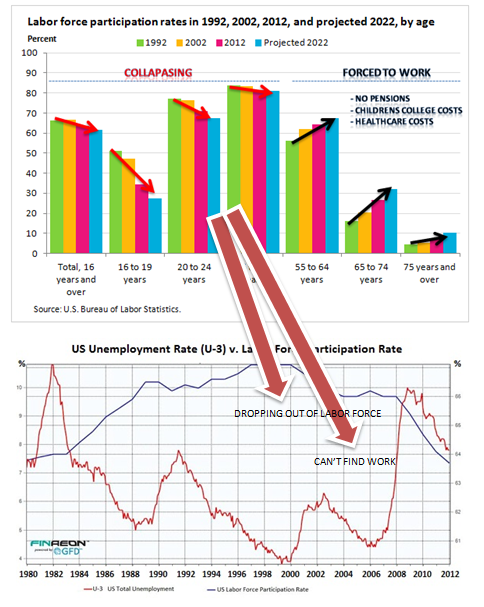

CHRONIC UNEMPLOYMENT - At its Core it is About a Lack of Private Investment Investment-Unemployment Link Still On Track 02-05-14 John B Taylor When the recovery was getting started I pointed out the remarkably strong inverse relationship between fixed investment as a share of GDP and the unemployment rate, and argued that a policy that focused on getting businesses to invest more would help get the unemployment rate down. The additional data from the past several years gives us a chance to check whether that relationship has held up. As shown in the following two charts, it has held up quite well.  The first time series chart shows that as investment has turned up as a share of GDP, the unemployment rate has fallen.  The increase in fixed investment thus far has been largely in the form of business fixed investment, though residential started to pick up last year. The second chart is a scatter plot with unemployment on the vertical axis and the investment ratio (in percent) on the horizontal axis. The lines connecting each quarterly observation represent the path from one quarter to the next. The chart illustrates the close correlation between the two variables. It also shows that the movement of unemployment and the investment ratio during the recovery (the recent dates are marked) has roughly paralleled the path in the recession, but in the reverse direction.  The problem, of course, is that the reverse path is way too short.  Investment has increased very slowly and has a long way to go before it gets back to levels that correspond to the 5 percent range for unemployment that we would like to see. So the message in the charts is much the same as several years ago: economic policies that focus on more private investment are likely to also reduce unemployment.

These diagrams would look very much the same if the denominator in the investment ratio was potential GDP rather than actual GDP. Of course, things other than investment can affect unemployment, and the correlation does not prove causation. As I pointed out here in a reply to comments on my original post, the correlation between investment and unemployment was also strong in the 1970s, through the scatter of points would be higher in the diagram then because demographic factors raised the average rate of unemployment. |

03-04-14 | US CATALYST |

7 - Chronic Unemployment | |||

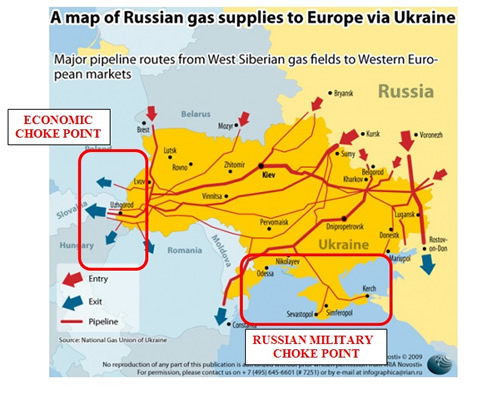

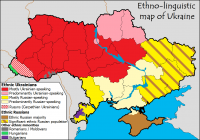

GEO-ECONOMIC RISK - Ukraine

Â

|

03-03-14 | ECO- POLICAL UKRAINE |

8 - Geo-Political Event | |||

GEO-ECONOMIC RISK - Ukraine Memo to Obama: This Was Their Red Line! 03-02-14 David Stockman, via his new blog Contra Corner via ZH

For the next 171 years Crimea was an integral part of Russiaâa span that exceeds the 166 years that have elapsed since California was annexed by a similar thrust of âManifest Destinyâ on this continent, thereby providing, incidentally, the United States Navy with its own warm-water port in San Diego. While no foreign forces subsequently invaded the California coasts, it was most definitely not Ukrainian and Polish riffles, artillery and blood which famously annihilated The Charge Of The Light Brigade at the Crimean city of Balaclava in 1854; they were Russians defending the homeland. And the portrait of the Russian âheroâ hanging in Putinâs office is that of Czar Nicholas Iâwhose brutal 30-year reign brought the Russian Empire to its historical zenith, and who was revered in Russian hagiography as the defender of Crimea, even as he lost the 1850s war to the Ottomans and Europeans. Besides that, there is no evidence that Putin does historical apologies, anyway. In fact, its their Red Line. When the enfeebled Franklin Roosevelt made port in the Crimean city of Yalta in February 1945 he did know he was in Soviet Russia. Maneuvering to cement his control of the Kremlin in the intrigue-ridden struggle for succession after Stalinâs death a few years later, Nikita Khrushchev allegedly spent 15 minutes reviewing his âgiftâ of Crimea to his subalterns in Kiev in honor of the decision by their ancestors 300 years earlier to accept the inevitable and become a vassal of Russia. Self-evidently, during the long decades of the Cold War, the West did nothing to liberate the âcaptive nationâ of the Ukraineâwith or without the Crimean appendage bestowed upon it in 1954. Nor did it draw any red lines in the mid-1990?s when a financially desperate Ukraine rented back Sevastopol and the strategic redoubts of the Crimea to an equally pauperized Russia. In short, in the era before we got our Pacific port in 1848 and in the 166-year interval since then, the security and safety of the American people have depended not one wit on the status of the Russian-speaking Crimea. Should the local population now choose fealty to the Grand Thief in Moscow over the ruffians and rabble who have seized Kiev, whatâs to matter! Worse still, how long can America survive the screeching sanctimony and mindless meddling of Susan Rice and Samantha Power? Mr. President, send them back to geography class; donât draw any new Red Lines. This one has been morphing for centuries among the quarreling tribes, peoples, potentates, Patriarchs and pretenders of a small region that is none of our damn business. |

03-03-14 | ECO- POLICAL UKRAINE |

8 - Geo-Political Event | |||

GEO-ECONOMIC RISK - Ukraine Ukraine Crisis: Crimea in the Crosshairs 03-01-14 Geo-Political Monitor What is unfolding between Ukraine and Russia on the Crimean Peninsula? The answer is ostensibly simple: Russia is defending its interests at the behest of the mostly ethnic Russian population in Crimea. And while there are reports of an imminent Russian invasion, the fact is that Russia already has troops on the ground in Crimea, given that they have leased a major military base in Sevastopol. How will the situation evolve? |

03-03-14 | ECO- POLICAL UKRAINE |

8 - Geo-Political Event | |||

GEO-ECONOMIC RISK - Ukraine "Welcome To The Era Of Failed States" 03-03-14 James H. Kunstler of Kunstler.com, via ZH So, now we are threatening to start World War Three because Russia is trying to control the chaos in a failed state on its border â a state that our own government spooks provoked into failure? The last time I checked, there was a list of countries that the USA had sent troops, armed ships, and aircraft into recently, and for reasons similar to Russiaâs in Crimea: the former Yugoslavia, Somalia, Afghanistan, Iraq, Libya, none of them even anywhere close to American soil. I donât remember Russia threatening confrontations with the USA over these adventures. The phones at the White House and the congressional offices ought to be ringing off the hook with angry US citizens objecting to the posturing of our elected officials. There ought to be crowds with bobbing placards in Farragut Square reminding the occupant of 1400 Pennsylvania Avenue how ridiculous this makes us look. The saber-rattlers at The New York Times were sounding like the promoters of a World Wrestling Federation stunt Monday morning when they said in a Page One story:

Are they out of their chicken-hawk minds over there? It sounds like a ploy out of the old Eric Berne playbook: Letâs You and Him Fight. What the USA and its European factotums ought to do is mind their own business and stop issuing idle threats. They set the scene for the Ukrainian melt-down by trying to tilt the government their way, financing a pro-Euroland revolt, only to see their sponsored proxy dissidents give way to a claque of armed neo-Nazis, whose first official act was to outlaw the use of the Russian language in a country with millions of long-established Russian-speakers. This is apart, of course, from the fact Ukraine had been until very recently a province of Russiaâs former Soviet empire. Secretary of State John Kerry â a haircut in search of a brain â is winging to Kiev tomorrow to pretend that the USA has a direct interest in what happens there. Since US behavior is so patently hypocritical, it raises the pretty basic question: what are our motives? I donât think they amount to anything more than international grandstanding â based on the delusion that we have the power and the right to control everything on the planet, which is based, in turn, on our current mood of extreme insecurity as our own ongoing spate of bad choices sets the table for a banquet of consequences. America canât even manage its own affairs. We ignore our own gathering energy crisis, telling ourselves the fairy tale that shale oil will allow us to keep driving to WalMart forever. We paper over all of our financial degeneracy and wink at financial criminals. Our infrastructure is falling apart. Weâre constructing an edifice of surveillance and social control that would make the late Dr. Joseph Goebbels turn green in his grave with envy while we squander our dwindling political capital on stupid gender confusion battles. The Russians, on the other hand, have every right to protect their interests along their own border, to protect the persons and property of Russian-speaking Ukrainians who, not long ago, were citizens of a greater Russia, to discourage neo-Nazi activity in their back-yard, and most of all to try to stabilize a region that has little history and experience with independence. They also have to contend with the bankruptcy of Ukraine, which may be the principal cause of its current crack-up. Ukraine is deep in hock to Russia, but also to a network of Western banks, and it remains to be seen whether the failure of these linked obligations will lead to contagion throughout the global financial system. It only takes one additional falling snowflake to push a snow-field into criticality. Welcome to the era of failed states. Weâve already seen plenty of action around the world and weâre going to see more as resource and capital scarcities drive down standards of living and lower the trust horizon. The world is not going in the direction that Tom Friedman and the globalists thought. Anything organized at the giant scale is now in trouble, nation-states in particular. The USA is not immune to this trend, whatever we imagine about ourselves for now. |

03-03-14 | ECO- POLICAL UKRAINE |

8 - Geo-Political Event | |||

GEO-ECONOMIC RISK - Ukraine The Backstory to the Russia-Ukraine Confrontation: The U.S. and NATO Encirclement of Russia 03-03-14 George Washington Blog via ZH The American press portrays Putin as being the bad guy and the aggressor in the Ukraine crisis. Putin is certainly no saint. A former KGB agent, Putin's net worth is estimated at some $40 billion dollars ... as he has squeezed money out of the Russian economy by treating the country as his own personal fiefdom. And all sides appear to have dirt on their hands in the Russia-Ukraine crisis. But we can only see the bigger picture if we take a step back and gain a little understanding of the history underlying the current tensions. Indeed, the fact that the U.S. has allegedly paid billions of dollars to anti-Russian forces in Ukraine - and even purportedly picked the Ukrainian president - has to be seen in context. Veteran New York Times reporter Steven Kinzer notes at the Boston Globe:

Stephen Cohen - professor emeritus at New York University and Princeton University who has long focused on Russia - explained this weekend on CNN:

Jonathan Steele writes at the Guardian

Again, we don't believe that there are angels on any side. But we do believe that everyone has to take a step back, look at the bigger picture, calm down and reach a negotiated diplomatic resolution. And see this, this, this and this (interview with a 27-year CIA veteran, who chaired National Intelligence Estimates and personally delivered intelligence briefings to Presidents Ronald Reagan and George H.W. Bush and the Joint Chiefs of Staff). |

03-03-14 | ECO- POLICAL UKRAINE |

8 - Geo-Political Event | |||

| TO TOP | ||||||

| Â | ||||||

| MACRO News Items of Importance - This Week | ||||||

GLOBAL MACRO REPORTS & ANALYSIS |

|  |  | |||

US ECONOMIC REPORTS & ANALYSIS |

|  |  | |||

| CENTRAL BANKING MONETARY POLICIES, ACTIONS & ACTIVITIES | Â | Â | Â | |||

CENTRAL BANK POLICY - Insider Says Central Banks Making it Up as They Go! Former Central Banker Admits "[They] Are Making It Up As They Go Along" 03-03-14 Tim Price via Sovereign Man blog,via ZH A few weeks ago, William White (former economist at the Bank of England, the Bank of Canada, and Bank of International Settlements) made a frank admission. And while we search for assets whose prices are less obviously distorted by malign government intervention, itâs refreshing to hear a mea culpa from a member of the economics âprofessionâ. White said:

Doctors at least have the Hippocratic Oath: first, do no harm. If only economists and central bankers had a similar ethic. But they donât. So they continue âmaking it up as they go alongâ, as Mr. White suggests, applying failed ideas with impunity and continued authority to an unquestioning public. Warren Buffett famously compared financial markets to the card table, observing that if youâve been playing poker for half an hour and you still donât know who the patsy is, then youâre the patsy. It seems we are all patsies now. You can listen to the full interview here: Â |

03-04-14 | MACRO MONETARY | CENTRAL BANK |

|||

| Â | Â | Â | ||||

| Market | ||||||

| TECHNICALS & MARKET | Â |

|  | |||

| COMMODITY CORNER - HARD ASSETS | Â | PORTFOLIO | Â | |||

| COMMODITY CORNER - AGRI-COMPLEX | Â | PORTFOLIO | Â | |||

| SECURITY-SURVEILANCE COMPLEX | Â | PORTFOLIO | Â | |||

| Â | Â | Â | ||||

| THESIS | ||||||

| 2014 - GLOBALIZATION TRAP | 2014 |  |

||||

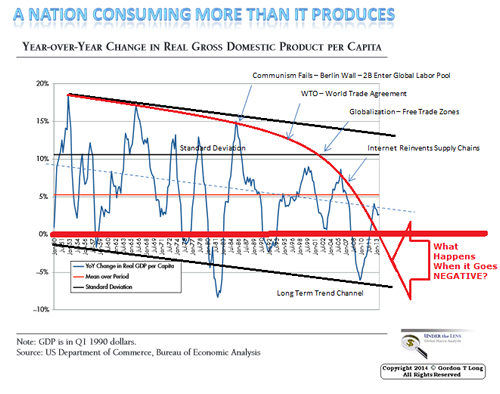

NO INVESTMENT GROWTH - NO JOB GROWTH!

IN THE ERA OF "LABOR ARBITRAGE" PROFITS DOMINATED BY LABOR REDUCTION KILLS THE "GOLDEN GOOSE" |

|  |  | |||

GLOBALIZATION DEMAND - Household Share of GDP The Problem

Ordinary households in too many countries have seen their share of total GDP plunge. Until it rebounds, the global imbalances will only remain in place, and without a global New Deal, the only alternative to weak demand will be soaring debt. Add to this continued political uncertainty, not just in the developing world but also in peripheral Europe, and it is clear that we should expect developing country woes only to get worse over the next two to three years. Nothing fundamental has changed. Demand is weak because the global economy suffers from excessively strong structural tendencies to force up global savings, or, which is the same thing, to force down global consumption. Lower future consumption makes investment today less profitable, so that consumption and investment, which together comprise total demand, are likely to stagnate for many more years. Squeezing out median households Two processes bear most of the blame for weak demand.

For many years the excess savings of the rich and of countries with income imbalances, in the form of capital exports in the latter case, funded a consumption binge among the global middle classes, especially in the US and peripheral Europe, letting us pretend that there was not a problem of excess savings. The 2007-08 crisis, however, put an end to what was anyway an unsustainable process. It is worth remembering that a structural tendency to force up the savings rate can be temporarily sidestepped by a credit-fueled consumption binge or by a surge in non-productive investment, both of which happened around the world in the past decade and more, but ultimately neither is sustainable. As I will show in my next blog entry in two weeks, in a closed economy, and the world is a closed economy, there are only two sustainable consequences of forcing up the savings rate. Either there must be a commensurate increase in productive investment, or there must be a rise in global unemployment. These are the two paths the world faces today. As the developing world cuts back on wasted investment spending, the worldâs excess manufacturing capacity and weak consumption growth means that the only way to increase productive investment is for countries that are seriously underinvested in infrastructure â most obviously the US but also India and other countries that have neglected domestic investment â to embark on a global New Deal. Otherwise the world has no choice but to accept high unemployment for many more years until countries like the US redistribute income downwards and countries like China increase the household share of GDP, neither of which is likely to be politically easy. But until ordinary households around the world regain the share of global GDP that they lost in the past two decades, the world will continue to face the same choices: an unsustainable increase in debt, an increase in productive investment, or higher global unemployment, that latter of which will be distributed through trade conflict. Emerging markets may well rebound strongly in the coming months, but any rebound will face the same ugly arithmetic. Ordinary households in too many countries have seen their share of total GDP plunge. Until it rebounds, the global imbalances will only remain in place, and without a global New Deal, the only alternative to weak demand will be soaring debt. Add to this continued political uncertainty, not just in the developing world but also in peripheral Europe, and it is clear that we should expect developing country woes only to get worse over the next two to three years. |

03-05-14 | THESIS | ||||

WHY IS HOUSEHOLD SHARE OF GDP SHRINKING?

READ BELOW |

03-05-14 | THESIS | GLOBAL- IZATION TRAP Â

|

|||

GLOBALIZATION DEMAND - Household Share of GDP The Problem

As the markets push once again into record territory the question of valuations becomes ever more important. While valuations are a poor timing tool in the short term for investors, in the long run valuation levels have everything to do with future returns. The reason I bring this up is that in 2013 reported earnings per share for the S&P 500 rose by 15.9% to a record of $100.28 per share with roughly 40% of that increase occurring in the 4th quarter alone. That late surge in corporate profits was a bit of a surprise as estimates had been lowered going into the end of last year. The question, however, remains the ongoing sustainability of that growth rate of earnings going forward. John Hussman, via Hussman Funds, made an interesting point in this regard in a recent note:

The chart below shows corporate profits, per the BEA, divided by GDP.  (You can substitute GNP but the result is virtually identical between the two measures.) The current levels of profits, as a share of GDP, are at record levels. This is interesting because corporate profits should be a reflection of the underlying economic strength. However, in recent years, due to financial engineering, wage and employment suppression and increase in productivity, corporate profits have become extremely deviated. This deviation begs the question of sustainability. Currently, according to the S&P website, reported corporate earnings are expected to grow by 20.26% in 2014, and by an additional 20.28% in 2015. In total, reported earnings are expected to grow by almost 50%($100.28/share as of 2013 to $147.50/share in 2015) over the next two years. If we assume that these projections are accurate, and we assume a continued growth rate of 2% annually in the economy (as has been witness the average since 1999) we can put the current environment into perspective. The chart below shows real, inflation adjusted, GDP and reported earnings, both actual and estimates, through 2015. I also notated the previous earnings trendline estimates that existed prior to each market peak.  The sustainability of corporate profits is dependent on two primary factors; sustained revenue growth and cost controls. From each dollar of sales is subtracted the operating costs of the business to achieve net profitability. The chart below shows the percentage change of sales, what happens at the top line of the income statement, as compared to actual earnings (reported and operating) growth. Since 2000, each dollar of gross sales has been increased into more than $1 in operating and reported profits through financial engineering and cost suppression. The next chart shows that the surge in corporate profitability in recent years is a result of a consistent reduction of both employment and wage growth. This has been achieved by increases in productivity, technology and offshoring of labor. However, it is important to note that benefits from such actions are finite. As asset prices continue to surge higher in hopes of an "economic revival," the question of"sustainability" of corporate profitability looms large. As John Hussman concludes:

As we know from repeatedly from history, extrapolated projections rarely happen. Could this time be different? Sure.  However, believing that historical tendencies have evolved into a new paradigm will likely have the same results as playing leapfrog with a Unicorn. There is mounting evidence, from valuations being paid in M&A deals, junk bond yields, margin debt and price extensions from long term means, "irrational exuberance" is once again returning to the financial markets. However, that does not mean that a mean reversion process in imminent. It was in 1996 when Alan Greenspan first uttered those famous words, it was 4 years later before investors regretted not paying attention them. It is likely that the same will be true this time. With the Federal Reserve still pushing liquidity into the markets, there is little to deter the "bullish bias" presently. However, as John noted above, investors that fail to heed the warning signs will likely ensure themselves a rude awakening over time |

03-05-14 | THESIS | ||||

WATER - EPA Defines "Water"  Abnormal heat and cold temperature is resulting in Water shortages. This in turn is resulting in Food price increases. � |

|  | ||||

|

||||||

|

2013 2014 |

|

|||||

2011 2012 2013 2014 |

|

|||||

| Â | Â | |||||

| THEMES | ||||||

| FLOWS -FRIDAY FLOWS | Â | THEME |  |

|||

Â

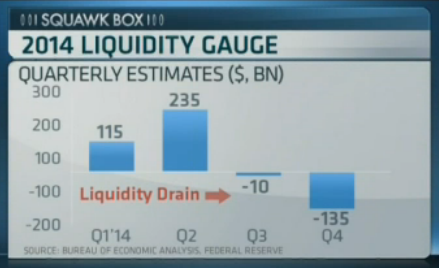

If you are an investor in the stock market, you may be in for a wild ride during the rest of this year. Think ROLLERCOASTER: slowly up, up, up, up and then, whoosh, way down fast. And, then, up again. Hereâs why. Liquidity determines the direction of asset prices; and the level of liquidity in the markets is going to change abruptly between the second and third quarter of this year. According to my calculations, liquidity will shift from being abundant â even excessive â in the second quarter to being tight in the third quarter and, then, very tight in the fourth quarter. This sudden change in liquidity conditions could whipsaw the markets. Â

The Fed has begun tapering Quantitative Easing. Nevertheless, it still intends to create $145 billion new dollars during the second quarter. It will inject that liquidity into the markets by acquiring financial assets. On the other side, the government is unlikely to absorb any liquidity at all during that period. Americans pay their taxes in April. Therefore, the US Treasury will probably have all the cash it needs and wonât have to sell any new (liquidity-absorbing) bonds during the second quarter. Thatâs going to leave a lot of excess liquidity sloshing around the financial markets between now and the end of June. And, when there is excess liquidity, stock prices tend to rise. By the third quarter, it will be a different story, however. The Fed will print much less and the government will borrow much more. During those three months, the Fed intends to create only $85 billion, whereas the government could have to borrow $180 billion or more. With the government borrowing more than the Fed is printing, there will no longer be any excess liquidity. In fact, there will be a liquidity drain. The markets have been spoiled by a great deal of excess liquidity since the end of 2012 when the Fed launched QE 3. They are going to find the reduction in liquidity very unpleasant. Bond yields are likely to begin moving up and stock prices are likely to begin moving down. It is in such moments that stock market panics often take hold. If investors do manage to maintain their nerve throughout the third quarter, they may find it considerably more difficult to remain calm during the fourth. The Fed has signaled that it will only print $20 billion during those three months, while the government is likely to have to borrow something like $240 billion to fund its budget deficit. (The budget deficit tends to be highest during the fourth quarter.) With the government sucking out much more liquidity than the Fed is pumping in, liquidity will be drained from the markets. In that environment, bond yields will rise. That will push up the cost of mortgages, causing the property market to take a hit. All this would be too much for the stock market to bear. If share prices donât fall in Q3, then, in the scenario being described here, they seem very likely to fall in Q4. Falling home prices and stock prices would cause a big drop in household sector wealth. Consumption would decline and the US would tumble back into recession, pulling the rest of the world down with it. I write âwouldâ instead of âwillâ because I donât believe the Fed will allow that scenario to play out. The Fed has worked very hard to push up asset prices in order to make the economy grow. I donât believe they will allow liquidity to tighten to the point where asset prices tumble again and drag the economy back into recession. That means that sometime during the third quarter, if not before, the Fed is going to have to announce it will stop tapering QE. That announcement may prove to be the biggest financial news story of the year. If I am right about this, then stocks are likely to move higher â and perhaps significantly higher â between now and mid-year. They will then begin to correct â and, again, perhaps quite significantly - during the third quarter. At that point, the Fed will ride to the rescue by announcing that it will continue its program of Quantitative Easing on into the indefinite future. Stocks will rally again on that news. This rollercoaster scenario is the one that strikes me as the most likely as of now. Of course, the futureâs not ours to see. Things change unexpectedly. Big disruptions appear out of nowhere. So, weâll have to wait and see. However, given what we know now, it looks to me that liquidity is going to tighten substantially. That suggests that either the stock market is going to buckle or, more probably, the Fed will backtrack again and keep its printing presses working overtime.

� Â

|

03-07-14 | FLOWS | ||||

| SHADOW BANKING -LIQUIDITY / CREDIT ENGINE | Â | THEME | Â | |||

| CRACKUP BOOM - ASSET BUBBLE | Â | THEME | Â | |||

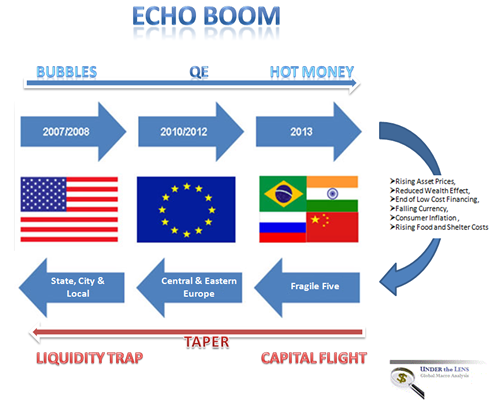

| ECHO BOOM - PERIPHERAL PROBLEM | Â | THEME | Â | |||

| PRODUCTIVITY PARADOX -NATURE OF WORK | Â | THEME | Â | |||

| STANDARD OF LIVING -EMPLOYMENT CRISIS | Â | THEME | Â | |||

| CORPORATOCRACY -CRONY CAPITALSIM | Â | THEME |  |

|||

CRONY CPAITALISM - Theft on Grand Scale

Missing Military-Industrial-Complex Money 02-19-14 batr.org  C O R P O R A T O C R A C Y

|

03-03-14 | THEME | Â CRONY CAPITALISM

|

|||

CORRUPTION & MALFEASANCE -MORAL DECAY - DESPERATION, SHORTAGES. |

| THEME |  |

|||

| SOCIAL UNREST - INEQUALITY & A BROKEN SOCIAL CONTRACT | Â | THEME | Â | |||

WATER - EPA Defines "Water" Fight Inequality With Better Jobs 03-02-14 Mort Zuckerman WSJ The anemic recovery has left millions still out of work or underemployed. The long-term solution: education. Adecade ago, before "income inequality" became a political watchword, the World Bank issued a report called "Beyond Economic Growth." The 2004 study concluded with this message: "An excessively equal distribution can be bad for economic efficiency. Take, for example, the experience of socialist countries where deliberately low inequality deprives people of the incentives needed for their active participation in economic activities." Among the consequences, the report noted, is "slower economic growth leading to more poverty." That insight is in danger of being lost nowadays, when many Americans, encouraged by their political leaders, have come to view the U.S. economy as a winner-take-all system. The disequilibrium in the distribution of wealth today is not hard to discern: The wealthiest 1% has captured 95% of the growth of wealth between 2009 and 2013, while the bottom 90% has become poorer in real terms. Yet these facts can distort the fundamental economic issue facing America. That issue is jobsâtheir scarcity and the quality of those that people manage to find. The unemployment rate is about 13% if you take into account people "marginally attached" to the workforce. The Bureau of Labor Statistics reports that at the end of 2013

No wonder recovery is a dirty word to millions of Americans who continue to experience hardship five years after the Great Recession of 2008-09. On Friday, the Commerce Department announced that fourth-quarter economic growth for 2013 was even lower than predicted, coming in at a desultory 2.4%. That is bad news for Americans who need work. Job losses in the low-wage and minimum-wage category is the critical issue of our day: Too many of the poor are not working full time or at all. Income inequality isn't so much the problem as income inadequacy. A more robust economy, stoked by growth-oriented policies from Washington, would help produce the jobs and opportunities that millions of Americans need to climb the economic ladder. A landmark new study by Harvard economics professor Raj Chetty asserts that advances in opportunity provided by expanded social programs have been offset by increased global trade and advanced technology that in turn have limited the traditional sources of middle-income jobs. But there is a simpler reason that the country remains mired in the weakest recovery from a recession since World War II: Government has diminished animal spirits by displaying a hostile attitude toward business. That attitude is evident in everything from excessive corporate taxes to the incompetence and dishonesty of the ObamaCare rollout. Government is perpetually establishing economic policies and rules that business perceives as overregulation, dampening the willingness to investâas witnessed by the slowest rate of capital investment in decades on corporate plant equipment and machinery. What is to be done to restore upward mobility with more and better jobs? The key is education, and that is where policy makers should focus. The two main sectors seeing healthy job growth today are education and health careâwhere having a college education is essential. Those with less than a high-school diploma have an unemployment rate triple those with a college degree (3.2%). Hoping for a return of manufacturing jobs for less-skilled workers is a pipe dream. Since 1979, the U.S. economy has added 45 million workers but has lost eight million manufacturing jobs. Technology has transformed the very nature of many industries: Eastman Kodak an iconic photography company that in its heyday had 145,000 employees, filed for bankruptcy in 2012âthe same year that Facebook paid $1 billion to buy the photo-related business Instagram, which had 13 employees. Silicon Valley companies and others across the country report that many tech jobs go unfilled because they can't find knowledgeable workers. Firms are offshoring their science, technology, engineering and math (STEM) jobs given the lack of qualified technical workers at home. There is a shortage of skilled labor generally: Nearly one in four small businesses, according to a February 2014 National Federation of Independent Business survey, have at least one position open because they have few or no qualified applicants. When technology jobs go begging, we inhibit startups in a field where each new job creates another five in the nearby community. As Enrico Moretti points out in "The New Geography of Jobs," a half-million new tech startup jobs translate into 2.5 million other new jobs. Federal and state education policy should step up support for science, technology, engineering and mathematics, in tandem with organizations such as Project Lead the Way, Achieve and Techbridge in building interest in these subjects. Not every tech job requires a college education: Better job-training can prepare young people for these good-paying jobs. The Department of Commerce's Economics and Statistics Administration has found that employees in STEM jobs earn 26% more than workers in non-STEM positions. We must also welcome people from abroad who are trained in STEM disciplines. That means restoring the H1-B visa admissions program to the higher levels of earlier yearsâ195,000 a year compared with only 65,000 today. A high proportion of these immigrants start new businesses, which are the source of some three million new jobs a year. Another way to encourage startups would be a tax holiday for their first three years of business. The political system is failing us. Washington doesn't seem to be listening, as our political parties are focused more on ideological conflict than the good of the country. Their inability to respond forcefully and practically to America's needs is no longer tolerable. Our national leadership must respond before more lives are ruined. Mr. Zuckerman is chairman and editor in chief of U.S. News & World Report. Â |

03-04-14 | THEME | ||||

| SECURITY-SURVEILLANCE COMPLEX -STATISM | Â | THEME | Â | |||

| GLOBAL FINANCIAL IMBALANCE - FRAGILITY, COMPLEXITY & INSTABILITY | Â | THEME | Â | |||

| CENTRAL PLANINNG -SHIFTING ECONOMIC POWER | Â | THEME | Â | |||

| CATALYSTS -FEAR & GREED | Â | THEME | Â | |||

| GENERAL INTEREST | Â |

|  | |||

| TO TOP | ||||||

From 2008 to 2013 we can see the market contracting, or winding / spiralling in on itself. This changed in 2013 when OIL started to expand. Previous resistance has now become support, however there is potential for the market to oscillate back down to the lows of 2008 as it âspirals outâ. Andrew J. D Long MFTA (Master of Technical Analysis - IFTA), Publisher, Trigger$

From 2008 to 2013 we can see the market contracting, or winding / spiralling in on itself. This changed in 2013 when OIL started to expand. Previous resistance has now become support, however there is potential for the market to oscillate back down to the lows of 2008 as it âspirals outâ. Andrew J. D Long MFTA (Master of Technical Analysis - IFTA), Publisher, Trigger$

In 1783 the Crimea was annexed by Catherine the Great, thereby satisfying the longstanding quest of the Russian Czars for a warm-water port. In fact, over the ages Sevastopol emerged as a great naval base at the strategic tip of the Crimean peninsula, where it became home to the mighty Black Sea Fleet of the Czars and then the commissars.

In 1783 the Crimea was annexed by Catherine the Great, thereby satisfying the longstanding quest of the Russian Czars for a warm-water port. In fact, over the ages Sevastopol emerged as a great naval base at the strategic tip of the Crimean peninsula, where it became home to the mighty Black Sea Fleet of the Czars and then the commissars.

Tipping Points Life Cycle - Explained

Click on image to enlarge

Â Â Â

Â

TO TOP

|

YOUR SOURCE FOR THE LATEST THINKING & RESEARCH  |

Â

Â

�

Â

TO TOP

Â

Â

Â