|

JOHN RUBINO'SLATEST BOOK |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

"MELT-UP MONITOR "

Meltup Monitor: FLOWS - The Currency Cartel Carry Cycle - 09 Dec 2013 Meltup Monitor: FLOWS - Liquidity, Credit & Debt - 04 Dec 2013 Meltup Monitor: Euro Pressure Going Critical - 28- Nov 2013 Meltup Monitor: A Regression-to-the-Exponential Mean Required - 25 Nov 2013

|

![]()

"DOW 20,000 "

Lance Roberts Charles Hugh Smith John Rubino Bert Dohman & Ty Andros

|

HELD OVER

Currency Wars

Euro Experiment

Sultans of Swap

Extend & Pretend

Preserve & Protect

Innovation

Showings Below

"Currency Wars "

|

"SULTANS OF SWAP" archives open ACT II ACT III

ALSO Sultans of Swap: Fearing the Gearing! Sultans of Swap: BP Potentially More Devistating than Lehman! |

"EURO EXPERIMENT"

archives open EURO EXPERIMENT : ECB's LTRO Won't Stop Collateral Contagion!

EURO EXPERIMENT: |

![]()

"INNOVATION"

archives open |

"PRESERVE & PROTE CT"

archives open |

Weekend Jan. 3rd, 2015

Follow Our Updates

on TWITTER

https://twitter.com/GordonTLong

AND FOR EVEN MORE TWITTER COVERAGE

STRATEGIC MACRO INVESTMENT INSIGHTS

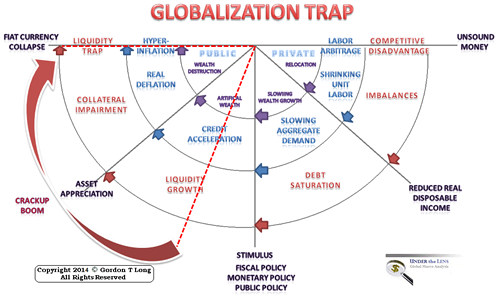

2014 THESIS: GLOBALIZATION TRAP

2014 THESIS: GLOBALIZATION TRAP

NOW AVAILABLE FREE to Trial Subscribers

185 Pages

What Are Tipping Poinits?

Understanding Abstraction & Synthesis

Global-Macro in Images: Understanding the Conclusions

![]()

| DECEMBER | ||||||

| S | M | T | W | T | F | S |

| 30 | 1 | 2 | 3 | 4 | 5 | 6 |

| 7 | 8 | 9 | 10 | 11 | 12 | 13 |

| 14 | 15 | 16 | 17 | 18 | 19 | 20 |

| 21 | 22 | 23 | 24 | 25 | 26 | 27 |

| 28 | 29 | 30 | 31 | 1 | 2 | 3 |

KEY TO TIPPING POINTS |

| 1 - Risk Reversal |

| 2 - Japan Debt Deflation Spiral |

| 3- Bond Bubble |

| 4- EU Banking Crisis |

| 5- Sovereign Debt Crisis |

| 6 - China Hard Landing |

| 7 - Chronic Unemployment |

| 8 - Geo-Political Event |

| 9 - Global Governance Failure |

| 10 - Chronic Global Fiscal ImBalances |

| 11 - Shrinking Revenue Growth Rate |

| 12 - Iran Nuclear Threat |

| 13 - Growing Social Unrest |

| 14 - US Banking Crisis II |

| 15 - Residential Real Estate - Phase II |

| 16 - Commercial Real Estate |

| 17 - Credit Contraction II |

| 18- State & Local Government |

| 19 - US Stock Market Valuations |

| 20 - Slowing Retail & Consumer Sales |

| 21 - China - Japan Regional Conflict |

| 22 - Public Sentiment & Confidence |

| 23 - US Reserve Currency |

| 24 - Central & Eastern Europe |

| 25 - Oil Price Pressures |

| 26 - Rising Inflation Pressures & Interest Pressures |

| 27 - Food Price Pressures |

| 28 - Global Output Gap |

| 29 - Corruption |

| 30 - Pension - Entitlement Crisis |

| 31 - Corporate Bankruptcies |

| 32- Finance & Insurance Balance Sheet Write-Offs |

| 33 - Resource Shortage |

| 34 - US Reserve Currency |

| 35- Government Backstop Insurance |

| 36 - US Dollar Weakness |

| 37 - Cyber Attack or Complexity Failure |

| 38 - Terrorist Event |

| 39 - Financial Crisis Programs Expiration |

| 40 - Natural Physical Disaster |

| 41 - Pandemic / Epidemic |

Reading the right books?

No Time?

We have analyzed & included

these in our latest research papers Macro videos!

![]()

OUR MACRO ANALYTIC

CO-HOSTS

John Rubino's Just Released Book

![]()

Charles Hugh Smith's Latest Books

![]()

![]()

Our Macro Watch Partner

Richard Duncan Latest Books

MACRO ANALYTIC

GUESTS

F William Engdahl

![]()

![]()

![]()

![]()

![]()

OTHERS OF NOTE

![]()

![]()

![]()

![]()

Book Review- Five Thumbs Up

for Steve Greenhut's

Plunder!

![]()

TODAY'S TIPPING POINTS

|

Scroll TWEETS for LATEST Analysis

Read More - OUR RESEARCH - Articles Below

HOTTEST TIPPING POINTS |

Theme Groupings |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Investing in Macro Tipping Points

THESE ARE NOT RECOMMENDATIONS - THEY ARE MACRO COMMENTARY ONLY - Investments of any kind involve risk. Please read our complete risk disclaimer and terms of use below by clicking HERE |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

We post throughout the day as we do our Investment Research for: LONGWave - UnderTheLens - Macro |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

"BEST OF THE WEEK "

|

Posting Date |

Labels & Tags | TIPPING POINT or THEME / THESIS or INVESTMENT INSIGHT |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

MOST CRITICAL TIPPING POINT ARTICLES TODAY

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

THE $100 TRILLION BOND BUBBLE. REDUCED LIVING STANDARDS

SOCIAL SPENDING & ENTITLEMENTS

LOGICAL DEVELOPMENTS This is why Central Banks have done everything they can to stop any and all defaults from occurring in the sovereign bonds space. Indeed, when you consider the bond bubble everything Central Banks have done begins to make sense.

RISK HAS BECOME CHEAPER

LEVERAGE HAS GROWN DRAMATICALLY

A $191 TRILLION TIME BOMB Cliff Kule has tried to convey the point that everyone waiting for interest rates to 'normalize' (rise) are waiting in vain as long as the Federal Reserve remains in control of the people's money. It is in their (& in their partner .. the government) self interest to keep rates artificially low .. not just to save the government in interest expenses, but to keep the banks' derivatives profitable (for the banks .. not for the derivative buyers) AND not blowing the banks to smithereens. This is directly from Phoenix Capital & it would be tough for us to explain it any more clearly:

When this bubble bursts, 2008 will look like a picnic. |

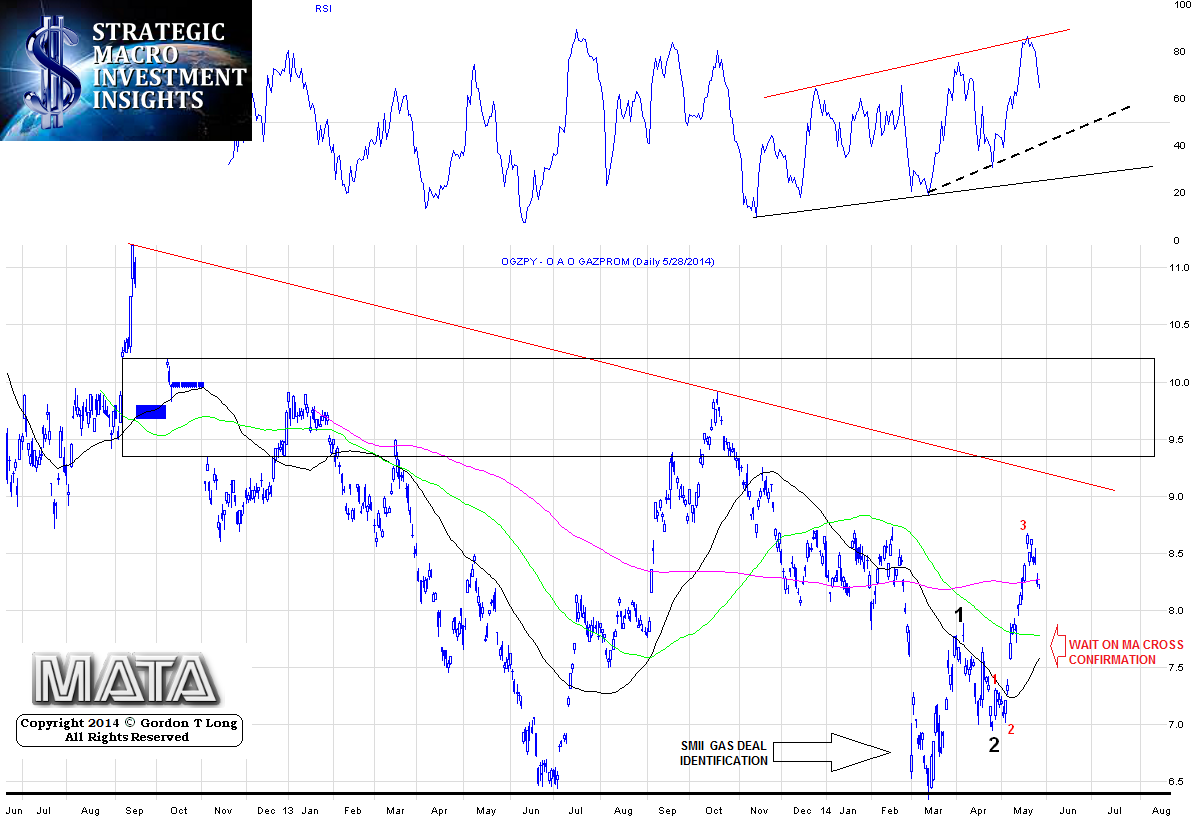

01-03-15 | 3- Bond Bubble | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

BOND BUBBLE - Its About Supply Growth Relative to Demand Growth The Worst Case Scenario For Bond Bears According To JPM: Rising Stock Prices 01-04-15 via ZH We have previously discussed the massive, and getting bigger, Treasury supply/demand imbalance as we head into 2015, when none other than the ECB is expected to join the monetization fray alongside the BOJ, and as we previously reported using a Goldman analysis, while the BOJ is expected to monetize some 100% of all gross Japanese issuance, the ECB will buy some 90% of all Bunds Germany has to issue in 2015, as well as hundreds of billions in other European public debt. So here comes JPM with its own even more startling analysis which finds that total central bank monetization of soverign debt will increase from $1.0 trillion in 2014 (between the Fed and the BOJ) to $1.3 trillion (between the BOJ and the ECB). Why? Recall Citi's analysis from October that "It Costs Central Banks $200 Billion Per Quarter To Avoid A Market Crash."

None of this is news, and certainly not to anyone who read "Desperately Seeking $11.2 Trillion In Collateral", but for those still calling for soaring bond yields now that there is a "recovery", here is a hint: the frontrunning of central banks means there is $600 billion more demand than supply in 2015. It does not take rocket surgery to figure out what this unprecedented excess global Treasury demand means for bond, aka scarce "High Quality Collateral", prices. Yet one thing which JPM did note to our surprise and which is sure to lead to yet another bloodbath for the momentum-chasing, levered beta entities formerly known as hedge funds, and who - in their complete lack of creativity - have once again put on the long S&P, short 10 Year pair trade on hoping that this is the year, is the following:

And that's a half a trillion in additional purchases just out of static reasons, i.e., to keep allocations flat. If asset managers decide that "bond kings" like Gundlach are correct, and that bonds will generate better returns than stocks for the second year in a row, and decide to actively raise the bond allocation above 37%, then all demand bets are off. However, even absent that scenario, the paradox emerges: another 10% increase in the S&P, something which is roughly in line with where the consensus sees the S&P500 saying goodbye to 2015 and the bond market is suddenly subject to a historic imbalance of as much as $1 trillion in excess demand, as a result of both portfolio allocation and central bank buying! Said otherwise, the biggest threat to bond bears and everyone else who is short the long end, is precisely the very signal that said bears have misinterpreted as being the catalyst for the long-awaited bond market selloff: rising stock prices. And then there is the flipside: if 2015 is the year when the inevitable 3rd consecutive bubble (after the 2001 dot com and the 2007 housing bubble) finally pops, which way will bonds trade then, or will this time be different and a wholesale stock market crash finally also result in a parallel dumping of bonds? If so, just what long-despised asset class will the algos end up having now choice but to buy then? |

01-03-15 | 3- Bond Bubble | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

BOND BUBBLE - Prices Will Continue to Rise as Yields Fall. WE HAVE BEEN OF THE BELIEF & ARGUED FOR 5 YEARS NOW THAT THE 10Y UST RATES ARE HEADED FOR < 1% BEFORE THE END OF 2018

LONG TERM The aftershocks of coming off the Gold Stnadard in August 1971 resulted in unprecented rates which the Volker Fed and the Reagan Administration gained control of. No one to this day has been able to satisfactorially explain how this was done and in such as manner as to sustain the continuous drop has seen below. What is noticeable is how controlled and managed the drop has been over a long period of time, following a very clear regression channel and trading boundary conditions (blue channel). INTERMEDIATE TERM Since the 2008 Financial Crisis which ushered in various forms of Quantitative Easing (QE), Fed Policy has resulted in lower rates with each and evey intervention iteration.

SHORT TERM TAPER has reduced the 13 Week ROC of the Fed's Balance Sheet, strengthened the US$ and weakened the 10Y UST yield.

FALSE PERCEPTIONS

So with expectations of higher yields (lower bond prices) and portfolio allocations shrinking (below), why would bond prices be rising and yields continuing to fall? Part of the answer lies in an ORCHESTRATED shortage of SUPPLY. But with 75M Baby Bommers beginning to retire and Entitlement programs becoming a budget 'bleed' the SUPPLY of government bonds will soon be forced to increase. OUT OF RUNWAY! The Buy Side communitiy do not believe government economic growth numbers, seriously question US fiscal revenue projections and certainly aren't investing in highly optimistic budget deficit projections! MARKET SEES SOMETHING DIFFERENT THE MARKET SEES SIGNIFICANTLY MORE FED MONETARY INTERVENTION AHEAD

UST DICTATES GLOBAL RATES The German Bund Controls EU Spread But IS ITSELF Controlled by UST

The SAME IS TRUE FOR THE YEN

POLITICAL COVER SO WHAT WOULD ALLOW CENTRAL BANKS TO TAKE RATES EVEN LOWER? A DEFLATION SCARE LIKE COLLAPSING COMMODITIES (Like Oil)!!

|

01-02-15 | CoN PATTERNS DRIVERS |

3- Bond Bubble | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| MOST CRITICAL TIPPING POINT ARTICLES THIS WEEK - Dec 28th, 2014 - Jan 3rd ,2014 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| RISK REVERSAL | 1 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| JAPAN - DEBT DEFLATION | 2 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| BOND BUBBLE | 3 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

EU BANKING CRISIS |

4 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| SOVEREIGN DEBT CRISIS [Euope Crisis Tracker] | 5 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| CHINA BUBBLE | 6 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| TO TOP | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| MACRO News Items of Importance - This Week | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

GLOBAL MACRO REPORTS & ANALYSIS |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

US ECONOMIC REPORTS & ANALYSIS |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| CENTRAL BANKING MONETARY POLICIES, ACTIONS & ACTIVITIES | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Market | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| TECHNICALS & MARKET |

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

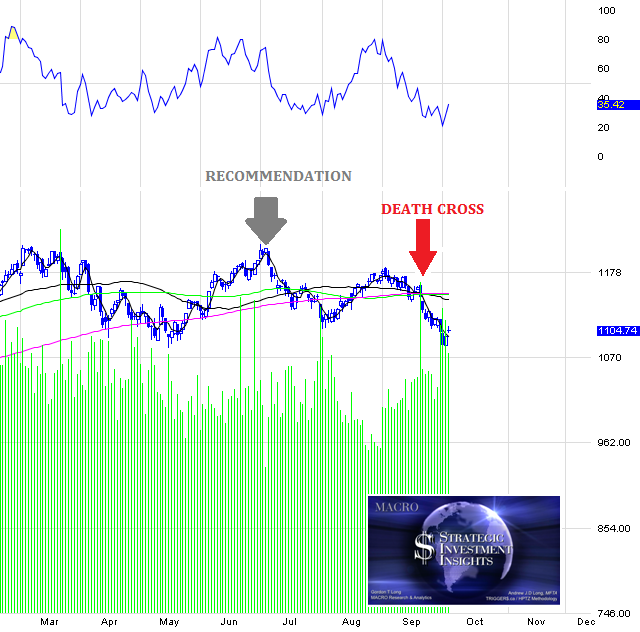

RISK REVERSAL

MINIMALLY MAYBE A SHORT TERM SCARE? IS OUR "M" TOP REAL DEFLATION SCARE LEG ABOUT TO HAPPEN?

BUT NOT TO WORRY THE COMING SCARE WILL ALLOW EVEN MORE DRACONIAN CENTRAL BANK ACTIONS!

|

12-30-14 | CoN PATTERNS RISK |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| COMMODITY CORNER - HARD ASSETS | PORTFOLIO | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| COMMODITY CORNER - AGRI-COMPLEX | PORTFOLIO | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| SECURITY-SURVEILANCE COMPLEX | PORTFOLIO | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| THESIS | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2014 - GLOBALIZATION TRAP | 2014 |  |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

2013 2014 |

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

FINANCIAL REPRESSION - Misplaced Central Banking Policies Lead to their Demise Below are two articles by my Co-Host at MACRO - Charles Hugh Smith that we will discuss in an upcoming MACRO video. OUR MESSAGE: How Central Banks Unknowingly Create Their Achilles Heel: Deflation

THE OIL SHOCK IS YOUR FIRST SIGN! Central Banks by creating 'Excessive' INFLATION actually sow their eventual destruction by creating DEFLATION

CONCLUSION EASY CREDIT CREATES EXCESS SUPPLY & DEMAND WHICH EVENTUALLY REACH EQUILIBRIUM

SHRINKING AGGREGATE DEMAND THEN REDUCES COMMODITY PRICES WHICH LEADS TO COLLAPSING COLLATERAL VALUES THE GLOBALIZATION TRAP

Central Banks Create Deflation, Not Inflation (December 9, 2014) Financial and risk bubbles don't pop in a vacuum--all the phantom collateral constructed with mal-invested free money for financiers will also implode.

Central Banks' 2% Plan to Impoverish You (December 11, 2014) The 2% target is low enough that the household frogs in the kettle of hot water never realize they're being boiled alive because the increase is so gradual.

|

12-29-14 | THESIS | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

2011 2012 2013 2014 |

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| THEMES | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| FLOWS -FRIDAY FLOWS | THEME |  |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| SHADOW BANKING -LIQUIDITY / CREDIT ENGINE | THEME | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| CRACKUP BOOM - ASSET BUBBLE | THEME | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| ECHO BOOM - PERIPHERAL PROBLEM | THEME | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| PRODUCTIVITY PARADOX -NATURE OF WORK | THEME | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| STANDARD OF LIVING -EMPLOYMENT CRISIS | THEME | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| CORPORATOCRACY -CRONY CAPITALSIM | THEME |  |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

CORRUPTION & MALFEASANCE -MORAL DECAY - DESPERATION, SHORTAGES. |

THEME |  |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| SOCIAL UNREST -INEQUALITY & A BROKEN SOCIAL CONTRACT | THEME | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| SECURITY-SURVEILLANCE COMPLEX -STATISM | THEME | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| GLOBAL FINANCIAL IMBALANCE - FRAGILITY, COMPLEXITY & INSTABILITY | THEME | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| CENTRAL PLANINNG -SHIFTING ECONOMIC POWER | THEME | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| CATALYSTS -FEAR & GREED | THEME | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| GENERAL INTEREST |

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| STRATEGIC INVESTMENT INSIGHTS | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

SII | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

SII | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

SII | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

SII | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| TO TOP | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

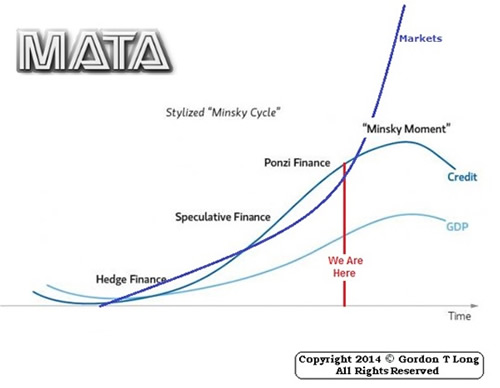

Tipping Points Life Cycle - Explained

Click on image to enlarge

{kind=link}

TO TOP

|

YOUR SOURCE FOR THE LATEST THINKING & RESEARCH

|

�

TO TOP