FINANCIAL REPRESSION - War on Cash

WHAT YOU NEED TO KNOW

"The only way to prevent the banking collapse is to prevent people from withdrawing cash. Hence, we see this trend is surfacing in all the mainstream press to get the people ready for what is coming – the elimination of cash. We are starting to even see this advocated in parts of Germany. We will not be able to buy or sell anything without government approval. That is where we are going ..." Martin Armstrong

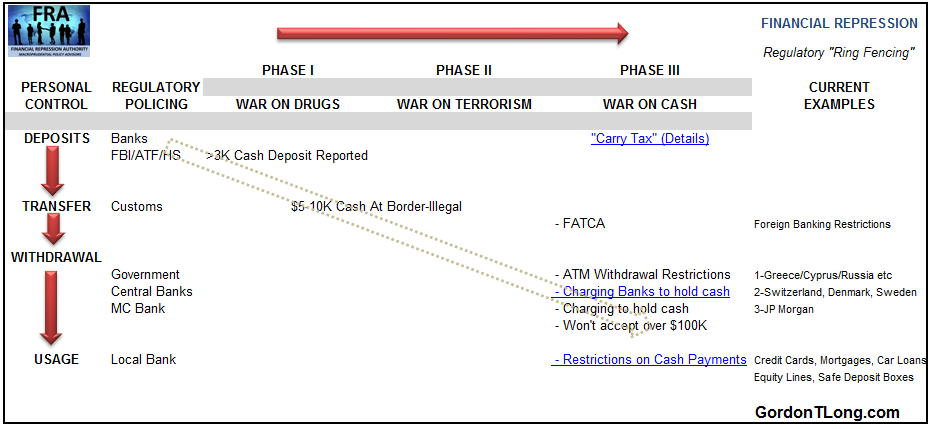

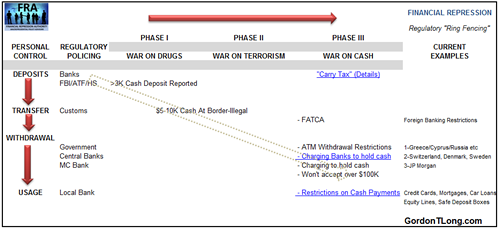

THE HIDDEN EVOLUTION

CLICK TO ENLARGE

1-We Can’t Rein In the Banks If We Can’t Pull Our Money Out of Them

Martin Armstrong summarizes the headway being made to ban cash, and argues that the goal of those pushing a cashless society is to prevent bank runs ... and increase their control:

The central banks are ... planning drastic restrictions on cash itself. They see moving to electronic money will

- First eliminate the underground economy, but

- Secondly, they believe it will even prevent a banking crisis.

This idea of eliminating cash was first floated as the normal trial balloon to see how the people take it. It was first launched by Kenneth Rogoff of Harvard University and Willem Buiter, the chief economist at Citigroup. Their claims have been widely hailed and their papers are now the foundation for the new age of Economic Totalitarianism that confronts us. Rogoff and Buiter have laid the ground work for the end of much of our freedom and will one day will be considered the new Marx with hindsight. They sit in their lofty offices but do not have real world practical experience beyond theory. Considerations of their arguments have shown how governments can seize all economic power are destroy cash in the process eliminating all rights.

Physical paper money provides the check against negative interest rates for if they become too great, people will simply withdraw their funds and hoard cash.

Furthermore, paper currency allows for bank runs. Eliminate paper currency and what you end up with is the elimination of the ability to demand to withdraw funds from a bank.

***

In many nations, specific measures have already been taken demonstrating that the Rogoff-Buiter world of Economic Totalitarianism is indeed upon us.

This is the death of Capitalism.

Of course the socialists hate Capitalism and see other people’s money should be theirs. What they cannot see is that Capitalism is freedom from government totalitarianism. The freedom to pursue the field you desire without filling the state needs that supersede your own.

There have been test runs of this Rogoff-Buiter Economic Totalitarianism to see if the idea works. I reported on June 21, 2014 that Britain was doing a test run.

- A shopping street in Manchester banned cash as part of an experiment to see if Brits would accept a cashless society.

- London buses ended accepting cash payments from July 2014.

- Meanwhile, Currency Exchange dealers began offering debt cards instead of cash that they market as being safer to travel with.

The Chorlton, South Manchester experiment was touted to test customers and business reaction to the idea for physical currency will disappear inside 20 years.

- France passed another Draconian new law that from the police parissummer of 2015 it will now impose cash requirements dramatically trying to eliminate cash by force.

- French citizens and tourists will then only be allowed a limited amount of physical money.

- They have financial police searching people on trains just passing through France to see if they are transporting cash, which they will now seize.

Meanwhile, the new French Elite are moving in this very same direction. Piketty wants to just take everyone’s money who has more than he does. Nobody stands on the side of freedom or on restraining the corruption within government. The problem always turns against the people for we are the cause of the fiscal mismanagement of government that never has enough for themselves.

- In Greece a drastic reduction in cash is also being discussed in light of the economic crisis.

- Now any bill over €70 should be payable only by check or credit card – it will be illegal to pay in cash.

- The German Baader Bank founded in Munich expects formally to abolish the cash to enforce negative interest rates on accounts that is really taxation on whatever money you still have left after taxes.

***

Complete abolition of cash threatens our very freedom and rights of citizens in so many areas.

***

Paper currency is indeed the check against negative interest rates. We need only look to Switzerland to prove that theory. Any attempt to impose say a 5% negative interest rates (tax) would lead to an unimaginably massive flight into cash. This was already demonstrated recently by the example of Swiss pension funds, which withdrew their money from the bank in a big way and now store it in vaults in cash in order to escape the financial repression. People will act in their own self-interest and negative interest rates are likely to reduce the sales of government bonds and set off a bank run as long as paper money exists.

Obviously, government and bankers are not stupid. The only way to prevent such a global bank run would be the total prohibition of paper money. This is unlikely, both in Switzerland and in the United States because the economies are dominated there by a certain “liberalism” to some extent but also because their currencies also circulate outside their domestic economies. The fact that but the question of the cash ban in the context of a global conference with the participation of the major central banks of the US and the ECB will be discussed, demonstrates by itself that the problem is not a regional problem.

Nevertheless, there is a growing assumption that the negative interest rate world (tax on cash) is likely to increase dramatically in Europe in particular since it is socialism that is collapsing. Government in Brussels is unlikely to yield power and their line of thinking cannot lead to any solution. The negative interest rate concept is making its way into the United States at J.P. Morgan where they will charge a fee on excess cash on deposit starting May 1st, 2015. Asset holdings of cash with a tax or a fee in the amount of the negative interest rate seems to be underway even in Switzerland.

***

The movement toward electronic money is moving at high speed and this says a lot about the state of the financial system. The track record of the major financial institutions is nearly perfect – they are always caught on the wrong side when a crisis breaks, which requires their bailouts. The fact that we have already seen test runs with theory-balloons flying, the major financial institutions are in no shape to withstand another economic decline.

For depositors, this means they really need to grasp what is going on here for unless they are vigilant, there is a serious risk of losing everything. We must understand that these measures will be implemented overnight in the middle of a banking crisis after 2015.75. The balloons have taken off and the discussions are underway. The trend in taxation and reduction of cash seems to be unstoppable. Government is not prepared to reform for that would require a new way of thinking and a loss of power. That is not a consideration. They only see one direction and that is to take us into the new promised-land of economic totalitarianism.

People can’t pull cash out of their bank accounts – for political reasons, because they’ve lost confidence in the bank, or because “bail-ins” are enacted – if cash is banned.

The Financial Times argued last year that central banks would be the real winners from a cashless society:

Central bankers, after all, have had an explicit interest in introducing e-money from the moment the global financial crisis began…

***

The introduction of a cashless society empowers central banks greatly. A cashless society, after all, not only makes things like negative interest rates possible, it transfers absolute control of the money supply to the central bank, mostly by turning it into a universal banker that competes directly with private banks for public deposits. All digital deposits become base money.

2-Why Central Banks HATE Cash and Will Begin to Tax It Shortly

Why Central Banks HATE Cash and Will Begin to Tax It Shortly 05-18-15 Graham Summers

Cash is a MAJOR problem for the Central Banks

The reason for this concerns the actual structure of the financial system, that structure is as follows:

1) The total currency (actual cash in the form of bills and coins) in the US financial system is a little over $1.36 trillion.

2) When you include digital money sitting in short-term accounts and long-term accounts then you’re talking about roughly $10 trillion in “money” in the financial system.

3) In contrast, the money in the US stock market (equity shares in publicly traded companies) is over $20 trillion in size.

4) The US bond market (money that has been lent to corporations, municipal Governments, State Governments, and the Federal Government) is almost twice this at $38 trillion.

5) Total Credit Market Instruments (mortgages, collateralized debt obligations, junk bonds, commercial paper and other digitally-based “money” that is based on debt) is even larger $58.7 trillion.

6) Unregulated over the counter derivatives traded between the big banks and corporations is north of$220 trillion.

When looking over these data points, the first thing that jumps out at the viewer is that the vast bulk of “money” in the system is in the form of digital loans or credit (non-physical debt).

Put another way, actual physical money or cash (as in bills or coins you can hold in your hand) comprises less than 1% of the “money” in the financial system.

As far as the Central Banks are concerned, this is a good thing because if investors/depositors were ever to try and convert even a small portion of this “wealth” into actual physical bills, the system would implode (there simply is not enough actual cash).

Remember, the current financial system is based on debt. The benchmark for “risk free” money in this system is not actual cash but US Treasuries.

In this scenario, when the 2008 Crisis hit, one of the biggest problems for the Central Banks was to stop investors from fleeing digital wealth for the comfort of physical cash. Indeed, the actual “thing” that almost caused the financial system to collapse was when depositors attempted to pull $500 billion out of money market funds.

A money market fund takes investors’ cash and plunks it into short-term highly liquid debt and credit securities. These funds are meant to offer investors a return on their cash, while being extremely liquid (meaning investors can pull their money at any time).

This works great in theory… but when $500 billion in money was being pulled (roughly 24% of the entire market) in the span of four weeks, the truth of the financial system was quickly laid bare: that digital money is not in fact safe.

To use a metaphor, when the money market fund and commercial paper markets collapsed, the oil that kept the financial system working dried up. Almost immediately, the gears of the system began to grind to a halt.

When all of this happened, the global Central Banks realized that their worst nightmare could in fact become a reality: that if a significant percentage of investors/ depositors ever tried to convert their “wealth” into cash (particularly physical cash) the whole system would implode.

As a result of this, virtually every monetary action taken by the Fed since this time has been devoted to forcing investors away from cash and into risk assets. The most obvious move was to cut interest rates to 0.25%, rendering the return on cash to almost nothing.

However, in their own ways, the various QE programs and Operation Twist have all had similar aims: to force investors away from cash, particularly physical cash.

After all, if cash returns next to nothing, anyone who doesn’t want to lose their purchasing power is forced to seek higher yields in bonds or stocks.

The Fed’s economic models predicted that by doing this, the US economy would come roaring back. The only problem is that it hasn’t. In fact, by most metrics, the US economy has flat-lined for several years now, despite the Fed having held ZIRP for 5-6 years and engaged in three rounds of QE.

As a result of this… mainstream economists at CitiGroup, the German Council of Economic Experts, and bond managers at M&G have suggested doing away with cash entirely.

This is just the beginning. Indeed… we've uncovered a secret document outlining how the US Federal Reserve plans to incinerate savings

3-The Government Can Manipulate Digital Accounts More Easily than Cash

Moreover, an official White House panel on spying has implied that the government is manipulating the amount in people’s financial accounts.

If all money becomes digital, it would be much easier for the government to manipulate our accounts.

Indeed, numerous high-level NSA whistleblowers say that NSA spying is about crushing dissent and blackmailing opponents … not stopping terrorism.

This may sound over-the-top … but remember, the government sometimes labels its critics as “terrorists“. If the government claims the power to indefinitely detain – or even assassinate – American citizens at the whim of the executive, don’t you think that government people would be willing to shut down, or withdraw a stiff “penalty” from a dissenter’s bank account?

If society becomes cashless, dissenters can’t hide cash. All of their financial holdings would be vulnerable to an attack by the government.

This would be the ultimate form of control. Because – without access to money – people couldn’t resist, couldn’t hide and couldn’t escape.

THE CENTRAL ECONOMIC & BANKING ISSUES

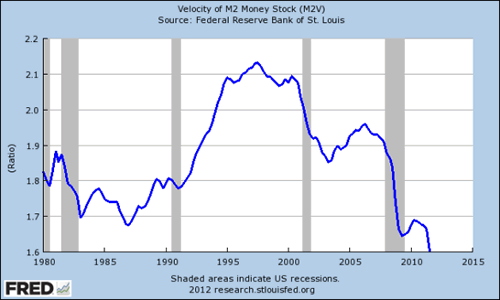

1- VELOCITY OF MONEY

The Coming Crash of All Crashes – but in Debt 05-15-15 Martin Armstrong

Why are governments rushing to eliminate cash? During previous recoveries following the recessionary declines from the peaks in the Economic Confidence Model, the central banks were able to build up their credibility and ammunition so to speak by raising interest rates during the recovery. This time, ever since we began moving toward Transactional Banking with the repeal of Glass Steagall in 1999, banks have looked at profits rather than their role within the economic landscape. They shifted to structuring products and no longer was there any relationship with the client. This reduced capital formation for it has been followed by rising unemployment among the youth and/or their inability to find jobs within their fields of study.

The VELOCITY of money peaked with our ECM 1998.55 turning point from which we warned of the pending crash in Russia.

The damage inflicted with the collapse of Russia and the implosion of Long-Term Capital Management in the end of 1998, has demonstrated that the VELOCITY of money has continued to decline. There has been no long-term recovery. This current mild recovery in the USA has been shallow at best and as the rest of the world declines still from the 2007.15 high with a target low in 2020, the Federal Reserve has been unable to raise interest rates sufficiently to demonstrate any recovery for the spreads at the banks between bid and ask for money is also at historical highs. Banks will give secured car loans at around 4% while their cost of funds is really 0%. This is the widest spread between bid and ask since the Panic of 1899.

We face a frightening collapse in the VELOCITY of money and all this talk of eliminating cash is in part due to the rising hoarding of cash by households both in the USA and Europe. This is a major problem for the central banks have also lost control to be able to stimulate anything.The loss of traditional stimulus ability by the central banks is now threatening the nationalization of banks be it directly, or indirectly. We face a cliff that government refuses to acknowledge and their solution will be to grab more power – never reform.

2- BANK RUNS & PROFITABILITY

The Trouble with Cash 05-14-15 Alasdair Macleod via GoldMoney.com,

When interest rates are zero and it costs a bank to look after your money it becomes an unattractive asset. Banks in some jurisdictions (such as Switzerland, Denmark and Sweden) are even charging customers interest on cash and deposits. And if you go to your bank and withdraw large amounts in the form of folding notes to avoid these charges you will be lucky if you are not treated as a sort of pariah. For the moment, at least, these problems do not extend to sound money, in other words gold.

There are two distinct issues involved with government-issued currency: zero-to-negative interest rates, which all but eliminate any interest turn on deposits for the banks; and a systemic issue that arises if too many people withdraw their money from the banking system. The problems with the latter would become significant if enough people decide to effectively opt out of holding money in the banks.

Conversion of bank deposits into physical cash increases reserve ratios, restricting the banks’ ability to create credit. However, while the banks are contractually obliged to supply physical cash to anyone who wants it, a drawdown on bank deposits is a bad thing from a central bank’s point of view. A desire for physical cash is, therefore, discouraged. Instead, if the option of owning physical cash was removed and there was only electronic money, deposits would simply be transferred from one bank to another and any imbalances between the banks resolved through the money markets, with or without the assistance of a central bank. The destabilising effects of bank runs would be eliminated entirely.

In the current financial climate demand for cash does not originate so much from loss of confidence in banks, with some notable exceptions such as in Greece. Instead it is a consequence of ultra-low or even negative interest rates. The desire for cash is therefore an unintended consequence of central banks attempting to inject confidence into the economy. The rights of ordinary individuals to turn deposits into physical cash are therefore resisted by central banks, which are focused instead on managing zero interest rate policies and suppressing any side effects.

Central banks can take this logic one step further. Monetary policy is primarily intended to foster investor confidence, so any tendency for investors to liquidate investments is, therefore, to be discouraged. However, with financial markets getting progressively more expensive central bankers will suspect the relative attraction of cash balances are increasing. And because banks are making cash deposits more costly, this is bound to increase demand for physical notes.

Monetary policy has now become like a pressure cooker with a defective safety-valve. Central bankers realise it and investors are slowly beginning to as well. Add into this mix a faltering global economy, a fact that is becoming impossible to ignore, and a dash-for-cash becomes a serious potential risk to both monetary policy and the banking system.

There is an obvious alternative to cash, and that is to buy physical gold. This does not constitute a run on the banking system, because a buyer of gold uses electronic money that transfers to the seller. The problem with physical gold is a separate issue: it challenges the raison d’être of the banking system and of government currencies as well.

This is why we can still buy gold instead of encashing our deposits, for the moment at least. It can only be a matter of time before people realise that with the cash option closing this is the only way to escape an increasingly dysfunctional financial system.

3- A "CARRY TAX"

The Secret Fed Paper That Advocated a "Carry Tax" on All Physical Cash 05-16-15 Graham Summers

Many commentators have noted that mainstream economists are calling to do away with cash entirely.

It would be easy to scoff at these proposals as completely insane if the Fed hadn’t published a paper back in 1999 suggesting the implementation of a “carry tax” or taxing actual physical cash using an expiration date if depositors aren’t willing to spend the money.

The author of this lunacy is a visiting scholar with the ECB, the Fed, the IMF, and the Swiss National Bank. The fact that two of those groups have already imposed negative interest rates (ECB and SNB) should give warning that these sorts of ideas are actually taken very seriously by Central Banks.

The paper, written 16 years ago, suggested that if the Fed were to find that zero interest rates didn’t induce economic growth, it could try one of three things:

1) A carry tax (meaning tax the value of actual physical cash that is taken out of the system)

2) Buy assets (QE)

3) Money transfers (literally HAND OUT money through various vehicles)

Regarding #1, the idea here is that since it costs relatively little to store physical cash (the cost of buying a safe), the Fed should be permitted to “tax” physical cash to force cash holders to spend it (put it back into the banking system) or invest it.

The way this would work is that the cash would have some kind of magnetic strip that would record the date that it was withdrawn. Whenever the bill was finally deposited in a bank again, the receiving bank would use this data to deduct a certain percentage of the bill’s value as a “tax” for holding it.

For instance, if the rate was 5% per month and you took out a $100 bill for two months and then deposited it, the receiving bank would only register the bill as being worth $90.25 ($100* 0.95=$95 or the first month, and then $95 *0.95= $90.25 for the second month).

It sounds like absolute insanity, but I can assure you that Central Banks take these sorts of proposals very seriously. QE sounded completely insane back in 1999 and we’ve already seen three rounds of it amounting to over $3 trillion.

No one would have believed the Fed could get away with printing $3 trillion for QE in 1999, but it has happened already. And given that it has failed to boost consumer spending/ economic growth, I wouldn’t at all surprised to see the Fed float one of the other ideas in the coming months.

Indeed, JP Morgan has already begun implementing a similar scheme by forbidding the storage of cash in its safe deposit boxes.

As of March, Chase began restricting the use of cash in selected markets, including Greater Cleveland. The new policy restricts borrowers from using cash to make payments on credit cards, mortgages, equity lines, and auto loans. Chase even goes as far as to prohibit the storage of cash in its safe deposit boxes .

In a letter to its customers dated April 1, 2015 pertaining to its "Updated Safe Deposit Box Lease Agreement," one of the highlighted items reads: "You agree not to store any cash or coins other than those found to have a collectible value." Whether or not this pertains to gold and silver coins with no numismatic value is not explained.

https://mises.org/blog/chase-joins-war-cash

Here is the single largest bank in the US, forbidding depositors from storing cash in a storage box or safe deposit box at their bank. And virtually no one even responded in outrage.

Again, the Fed has declared a War on Cash, and a “carry tax” is coming.

PROPAGANDA HAS BEGUN

GOVERNMENT'S LAUNCH "TRIAL BALLOONS" IN THE PUBLIC MEDIA

READ BELOW AND WEEP

How to end boom and bust: make cash illegal 05-

13-15 The Telegraph

Forcing everyone to spend only by electronic means from an account held at a government-run bank would give the authorities far better tools to deal with recessions and economic booms - Jim Leaviss

Gordon Brown promised to 'end boom and bust' but a cashless world would have given him far more chance to achieve it, academics suggest Photo: Getty Images

This story is part of our "Money Lab" series, in which respected figures from the world of finance put forward controversial ideas for improving our personal finances or the economy.

A proposed new law in Denmark could be the first step towards an economic revolution that sees physical currencies and normal bank accounts abolished and gives governments futuristic new tools to fight the cycle of “boom and bust”.

The Danish proposal sounds innocuous enough on the surface – it would simply allow shops to refuse payments in cash and insist that customers use contactless debit cards or some other means of electronic payment.

Officially, the aim is to ease “administrative and financial burdens”, such as the cost of hiring a security service to send cash to the bank, and is part of a programme of reforms aimed at boosting growth – there is evidence that high cash usage in an economy acts as a drag.

But the move could be a key moment in the advent of “cashless societies”. And once all money exists only in bank accounts – monitored, or even directly controlled by the government – the authorities will be able to encourage us to spend more when the economy slows, or spend less when it is overheating.

This may all sound far-fetched, but the idea has been developed in some detail by a Norwegian academic, Trond Andresen*.

In this futuristic world, all payments are made by contactless card, mobile phone apps or other electronic means, while notes and coins are abolished. Your current account will no longer be held with a bank, but with the government or the central bank. Banks still exist, and still lend money, but they get their funds from the central bank, not from depositors.

Having everyone’s account at a single, central institution allows the authorities to either encourage or discourage people to spend. To boost spending, the bank imposes a negative interest rate on the money in everyone’s account – in effect, a tax on saving.

Faced with seeing their money slowly confiscated, people are more likely to spend it on goods and services. When this change in behaviour takes place across the country, the economy gets a significant fillip.

The recipient of cash responds in the same way, and also spends. Money circulates more quickly – or, as economists say, the “velocity of money” increases.

What about the opposite situation – when the economy is overheating? The central bank or government will certainly drop any negative interest on credit balances, but it could go further and impose a tax on transactions.

So whenever you use the money in your account to buy something, you pay a small penalty. That makes people less inclined to spend and more inclined to save, so reducing economic activity.

Such an approach would be a far more effective way to damp an overheated economy than today’s blunt tool of a rise in the central bank’s official interest rate.

If this sounds rather fanciful, negative interest rates already exist in Denmark, where the central bank charges depositors 0.75pc a year, and in Switzerland.

At the moment it’s easy for individuals to avoid seeing their money eroded this way – they can simply hold banknotes, stored either in a safe or under the proverbial mattress.

But if notes and coins were abolished and the only way to hold money was through a government-controlled bank, there would be no escape.

Apart from the control over the economy, there would be many other advantages of a cashless society. Such a system is much cheaper to run than one based on banknotes and coins. Forgery is impossible, as are robberies.

Electronic money is an inclusive and convenient system, giving poor and rural sectors of an economy – where cash machines and bank branches may be few and far between and not all people have accounts – a tool for easy participation in the economy.

Finally, the “black economy” will be hugely diminished, and tax evasion made all but impossible.

Jim Leaviss is head of retail fixed interest at M&G Investments.

Leading German Keynesian Economist Calls For Cash Ban 05-16-15 Zero Hedge

It’s official: the world has gone central-planner crazy.

Monetary policy, whether in the form of “conventional” methods such as the micromanagement of policy rates or so-called “unconventional” measures such as QE, has proven utterly ineffective when it comes to both “smoothing out” the business cycle and reigniting economic growth in the wake of severe downturns. If anything, recent history has shown the exact opposite to be true. That is, the Fed helped to engineer the housing bubble and has now succeeded in inflating a similar bubble in stocks and fixed income. Meanwhile, the Japanese experience with QE has plunged the country into what we have affectionately dubbed “The Kuroda Zone”, wherein the BoJ has cornered both the stock and bond markets while failing to promote wage growth or meaningfully raise inflation expectations. In China, the PBoC has taken to cutting policy rates at the first sign of weakness in the stock market, helping to sustain what will perhaps go down in history as the second coming of the tulip bulb mania, while the ECB has taken the insane step of adopting a trillion euro bond buying program while simultaneously demanding fiscal discipline, meaning the central bank’s bond monetization efforts are set against a backdrop of meager supply.

In sum, the collective actions of the world’s most influential central banks have done wonders when it comes to inflating asset bubbles but have done very little to revive robust economic growth. In fact, far from smoothing out the business cycle and resuscitating DM demand, post-crisis monetary policy has actually had the exact opposite effect: it has set the stage for an even more spectacular collapse while simultaneously creating a worldwide deflationary supply glut.

At this stage, a sane person might be tempted to call it a day on the monetary experiments, especially considering that at this point, the limits have been reached. That is, there are literally no more assets to buyand rates have hit the effective lower bound where rational actors will eschew bank deposits in favor of the mattress. But not so fast, say folks like Citi’s Willem Buiter and economist Ken Rogoff: the world could always ban cash because if you eliminate physical currency and force people to use a debit card linked to a government controlled bank account for all transactions, you can effectively centrally plan everything. Consumers not spending? No problem. Just tax their excess account balance. Economy overheating? Again, no problem. Raise the interest paid on account holdings to encourage people to stop spending. So with Citi, Harvard, and Denmark all onboard, we bring you the latest call for a cashless society, this time from German economist and member of the German Council Of Economic Experts Peter Bofinger.

Via Spiegel (Google translated):

Coins and bills are obsolete and only reduce the influence of central banks. This position represents the economy Peter Bofinger. The federal government should stand up for the abolition of cash, he calls in the mirror…

The economy Peter Bofinger campaigns for the abolition of cash. "With today's technical possibilities coins and notes are in fact an anachronism," Bofinger told SPIEGEL.

If these away, the markets for undeclared work and drugs could be dried out. In addition, it would have the central banks easier to enforce its monetary policy.The teaching in Würzburg economics professor called on the federal government to promote at the international level for the abolition of cash. "That would certainly be a good topic for the agenda of the G-7 summit in Elmau," he said. (Click here to read the full interview in the new mirror .)

Even the former US Treasury Secretary Larry Summers and economist pleaded for an end to the already cash . Likewise, the US economist Kenneth Rogoff . He also argued that the interest rates of central banks have less clout when banks or consumer credit rather than hoard cash.

Critics warn, however , such debates would only distract from the real problems of the current monetary policy.

Yes, the “real problems” with current monetary policy. Like the fact that by design it can't possibly work(but it can and will push stocks to unprecedented highs). Paging Mr. Weidmann, your countrymen are going Keynesian crazy.

... More to come through the day

|

05-18-15

05-19-15 |

THEMES |

FINANCIAL REPRESSION

|