|

JOHN RUBINO'SLATEST BOOK |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

"MELT-UP MONITOR "

Meltup Monitor: FLOWS - The Currency Cartel Carry Cycle - 09 Dec 2013 Meltup Monitor: FLOWS - Liquidity, Credit & Debt - 04 Dec 2013 Meltup Monitor: Euro Pressure Going Critical - 28- Nov 2013 Meltup Monitor: A Regression-to-the-Exponential Mean Required - 25 Nov 2013

|

![]()

"DOW 20,000 "

Lance Roberts Charles Hugh Smith John Rubino Bert Dohman & Ty Andros

|

HELD OVER

Currency Wars

Euro Experiment

Sultans of Swap

Extend & Pretend

Preserve & Protect

Innovation

Showings Below

"Currency Wars "

|

"SULTANS OF SWAP" archives open ACT II ACT III

ALSO Sultans of Swap: Fearing the Gearing! Sultans of Swap: BP Potentially More Devistating than Lehman! |

"EURO EXPERIMENT"

archives open EURO EXPERIMENT : ECB's LTRO Won't Stop Collateral Contagion!

EURO EXPERIMENT: |

![]()

"INNOVATION"

archives open |

"PRESERVE & PROTE CT"

archives open |

Weekend Feb. 6th , 2016

Follow Our Updates

on TWITTER

https://twitter.com/GordonTLong

AND FOR EVEN MORE TWITTER COVERAGE

![]()

| FEBRUARY | ||||||

| S | M | T | W | T | F | S |

| 1 | 2 | 3 | 4 | 5 | 6 | |

| 7 | 8 | 9 | 10 | 11 | 12 | 13 |

| 14 | 15 | 16 | 17 | 18 | 19 | 20 |

| 21 | 22 | 23 | 24 | 25 | 26 | 27 |

| 28 | 29 | |||||

KEY TO TIPPING POINTS |

| 1- Bond Bubble |

| 2 - Risk Reversal |

| 3 - Geo-Political Event |

| 4 - China Hard Landing |

| 5 - Japan Debt Deflation Spiral |

| 6- EU Banking Crisis |

| 7- Sovereign Debt Crisis |

| 8 - Shrinking Revenue Growth Rate |

| 9 - Chronic Unemployment |

| 10 - US Stock Market Valuations |

| 11 - Global Governance Failure |

| 12 - Chronic Global Fiscal ImBalances |

| 13 - Growing Social Unrest |

| 14 - Residential Real Estate - Phase II |

| 15 - Commercial Real Estate |

| 16 - Credit Contraction II |

| 17- State & Local Government |

| 18 - Slowing Retail & Consumer Sales |

| 19 - US Reserve Currency |

| 20 - US Dollar |

| 21 - Financial Crisis Programs Expiration |

| 22 - US Banking Crisis II |

| 23 - China - Japan Regional Conflict |

| 24 - Corruption |

| 25 - Public Sentiment & Confidence |

| 26 - Food Price Pressures |

| 27 - Global Output Gap |

| 28 - Pension - Entitlement Crisis |

| 29 - Central & Eastern Europe |

| 30 - Terrorist Event |

| 31 - Pandemic / Epidemic |

| 32 - Rising Inflation Pressures & Interest Pressures |

| 33 - Resource Shortage |

| 34 - Cyber Attack or Complexity Failure |

| 35 - Corporate Bankruptcies |

| 36 - Iran Nuclear Threat |

| 37- Finance & Insurance Balance Sheet Write-Offs |

| 38- Government Backstop Insurance |

| 39 - Oil Price Pressures |

| 40 - Natural Physical Disaster |

Reading the right books?

No Time?

We have analyzed & included

these in our latest research papers Macro videos!

![]()

OUR MACRO ANALYTIC

CO-HOSTS

John Rubino's Just Released Book

![]()

Charles Hugh Smith's Latest Books

![]()

![]()

Our Macro Watch Partner

Richard Duncan Latest Books

MACRO ANALYTIC

GUESTS

F William Engdahl

![]()

![]()

![]()

![]()

![]()

OTHERS OF NOTE

![]()

![]()

![]()

![]()

Book Review- Five Thumbs Up

for Steve Greenhut's

Plunder!

![]()

|

Have your own site? Offer free content to your visitors with TRIGGER$ Public Edition!

Sell TRIGGER$ from your site and grow a monthly recurring income!

Contact [email protected] for more information - (free ad space for participating affiliates).

HOTTEST TIPPING POINTS |

Theme Groupings |

||

We post throughout the day as we do our Investment Research for: LONGWave - UnderTheLens - Macro

|

|||

|

MOST CRITICAL TIPPING POINT ARTICLES TODAY

|

|

||

POWER FAILURE No Post Today

|

|||

TIPPING POINTS, STUDIES, THESIS, THEMES & SII COVERAGE THIS WEEK PREVIOUSLY POSTED - (BELOW)

|

|||

| MOST CRITICAL TIPPING POINT ARTICLES THIS WEEK - Jan 31st, 2016 - Feb 6th, 2016 | |||

| TIPPING POINTS - This Week - Normally a Tuesday Focus | |||

| BOND BUBBLE | 1 | ||

| RISK REVERSAL - WOULD BE MARKED BY: Slowing Momentum, Weakening Earnings, Falling Estimates | 2 | ||

| GEO-POLITICAL EVENT | 3 | ||

| CHINA BUBBLE | 4 | ||

| JAPAN - DEBT DEFLATION | 5 | ||

EU BANKING CRISIS |

6 |

||

| TO TOP | |||

| MACRO News Items of Importance - This Week | |||

GLOBAL MACRO REPORTS & ANALYSIS |

|||

US ECONOMIC REPORTS & ANALYSIS |

|||

| CENTRAL BANKING MONETARY POLICIES, ACTIONS & ACTIVITIES | |||

| Market - WEDNESDAY STUDIES | |||

| STUDIES - MACRO pdf | |||

TECHNICALS & MARKET |

|

||

TECHNICALS & MARKET |

02-03-16 |

STUDIES | |

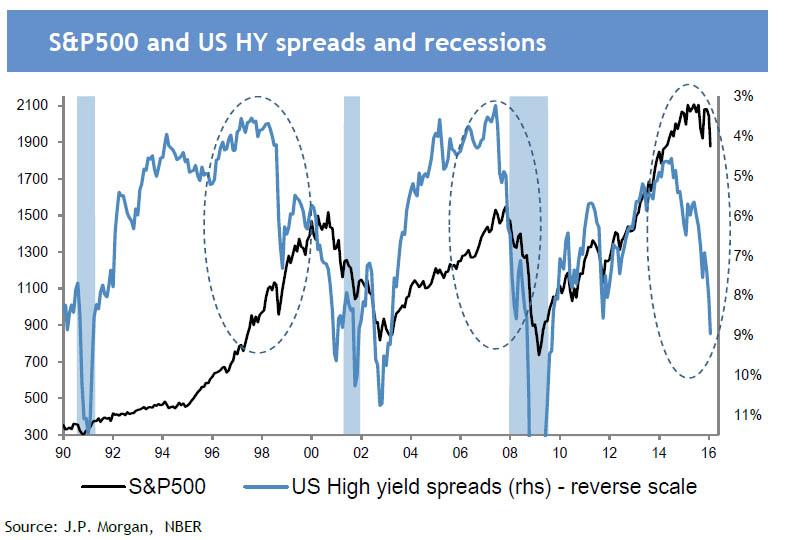

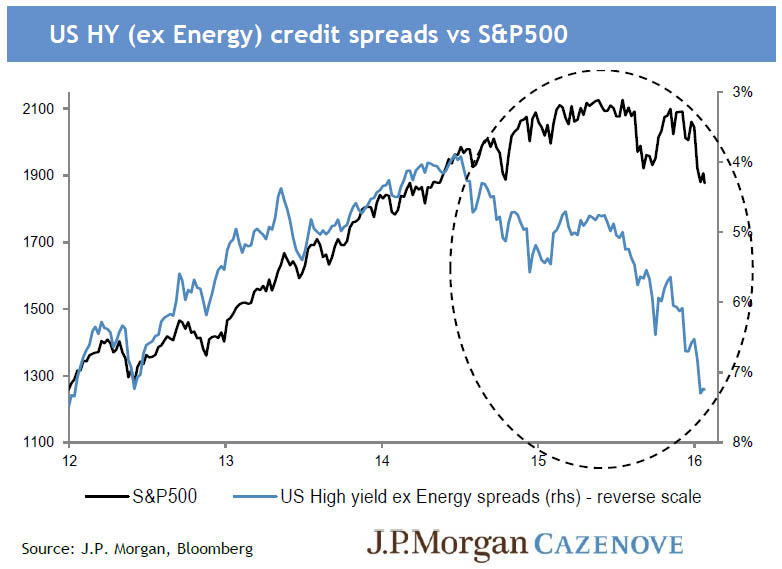

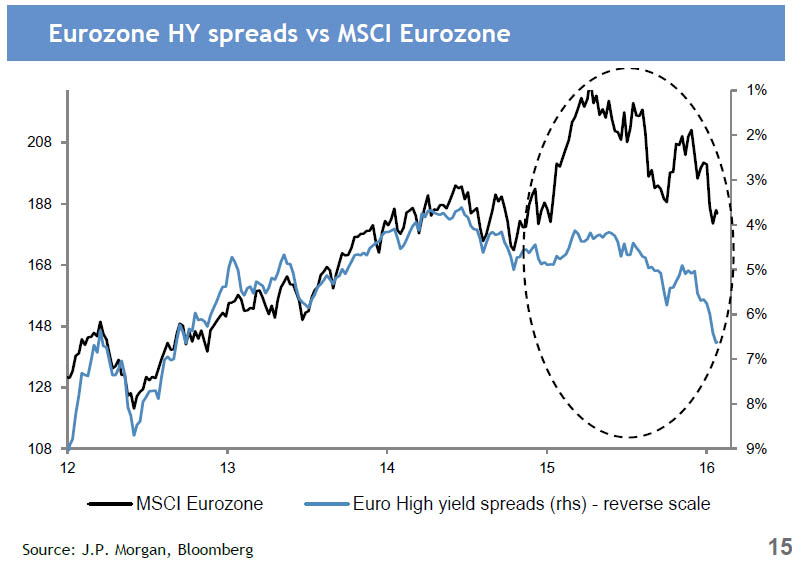

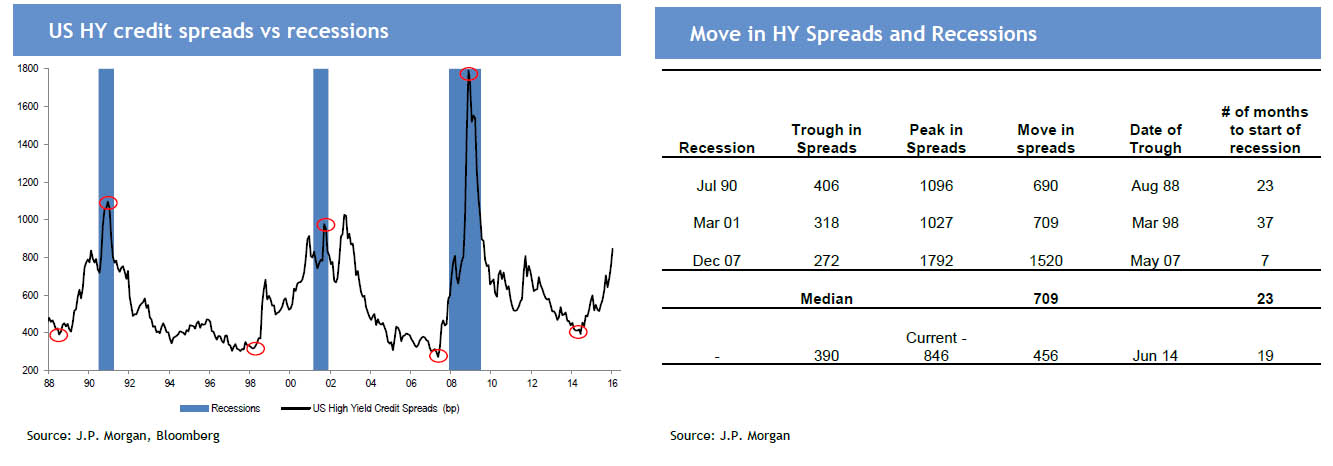

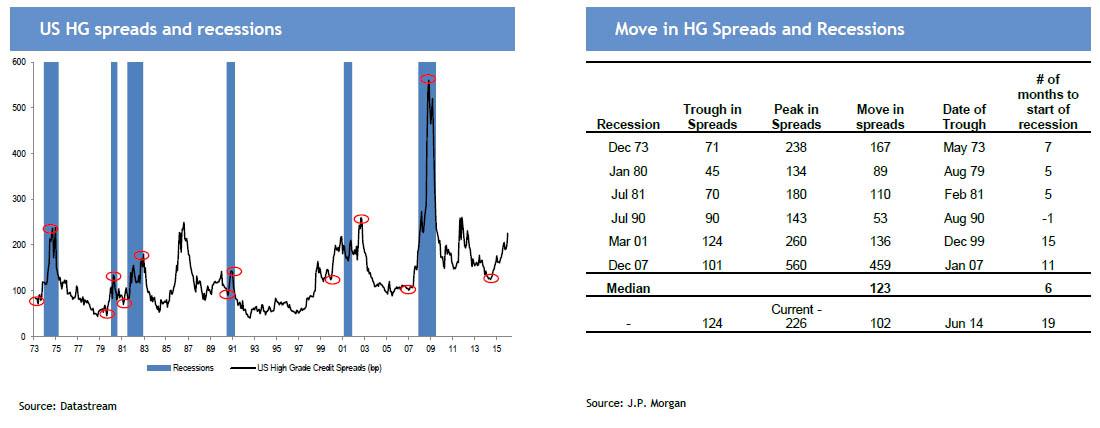

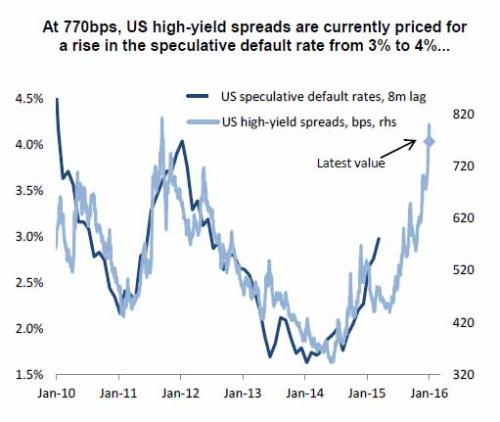

These Are Still The Most Disturbing Charts For The Stock MarketPosted:Mon, 01 Feb 2016 18:58:23 GMTBack before everyone became a junk bond expert, we repeatedly showed what in our opinion was the scariest chart for not only the US, but global stock markets: the unprecedented divergence between the stocks and junk bonds, suggesting that if the recent past is prologue, then the S&P 500 is in for a world of pain as it tracks HY credit far lower.

Since then, these fears have been realized and the market tumbled, unleashing even more central bank jawboning and intervention. That, however, has done nothing to fill what amount to a staggering gap, and as JPM notes today, the "credit backdrop has deteriorated; the gap with equities remains stark" Here is what else JPM says as it lays out what were the three scariest charts for stocks in the summer of 2015 and which remains the scariest charts for stocks as we enter February 2016:

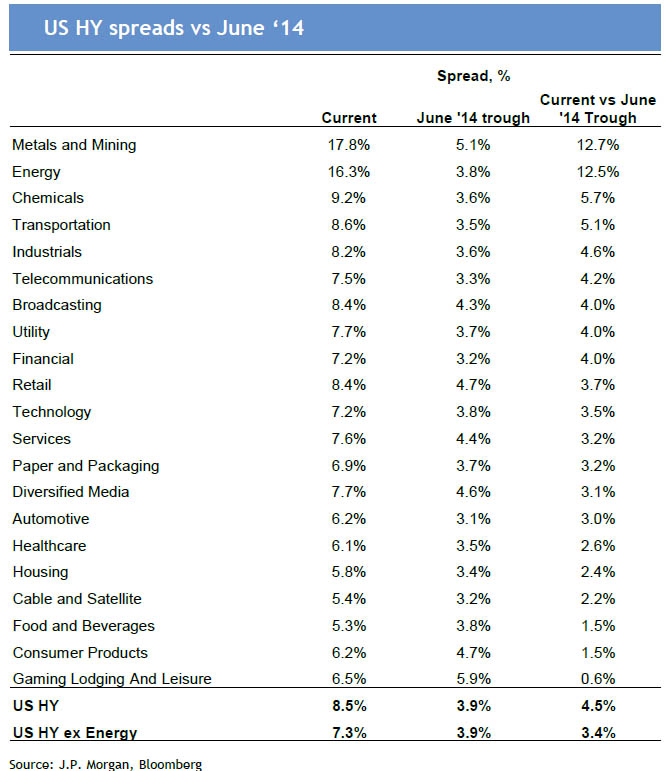

Where things get worse is that as JPM notes, "the increase in HY credit spreads is not just because of Energy, all 21 subsectors have seen widening; US lending standards are tightening again" and in fact "HY spreads have doubled over the past year, with broad participation."

JPM leaves off with two final concerns: "the signal from HY credit is a concern for the stage of the cycle we are in…"

And just as troubling, HY contagion has spread to Investment Grade, that all important source of debt-funded buybacks.

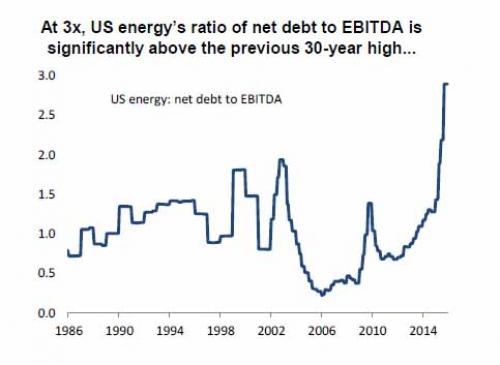

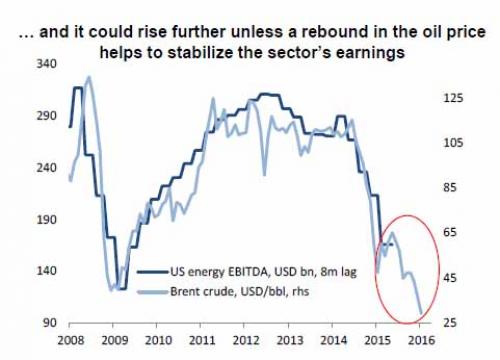

But once again the focal point will be energy where despite record low interest rates, the powder key is set to explode any moment for one simple reason: every incremental dollar of cash flows goes to satisfy bond holders, cash flows which decline with every passing day.

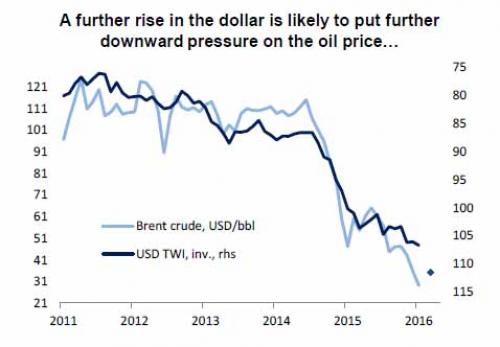

And the punchline, or the biggest irony in all of this, is that it is the Fed's own policies and the pursuit of the strong dollar, at least until the Fed relents and unleashes NIRP and more QE, which are pushing the US straight into the next global crash...

... a crash which would not be there had the Fed not intervened in 2008/9 and blown yet another bubble to mitigate the collapse and natural implosion of the previous housing and debt bubble, which in turn was blown to offset the bursting of the dot com bubble. We can only hope the bursting of the next, and biggest yet, bubble also takes away the almost thoroughly discredited central bankers with it... |

|||

| COMMODITY CORNER - AGRI-COMPLEX | |||

| THESIS - Mondays Posts on Financial Repression & Posts on Thursday as Key Updates Occur | |||

|

2016 | THESIS 2016 |  |

| 2015 - FIDUCIARY FAILURE | 2015 | THESIS 2015 |  |

| 2014 - GLOBALIZATION TRAP | 2014 |  |

|

|

|||

|

2013 2014 |

|

||

| 02-04-16 | |||

The Continuing Demonization Of CashSubmitted by Paul-Martin Foss via The Mises Institute, The insidious nature of the war on cash derives not just from the hurdles governments place in the way of those who use cash, but also from the aura of suspicion that has begun to pervade private cash transactions. In a normal market economy, businesses would welcome taking cash. After all, what business would willingly turn down customers? But in the war on cash that has developed in the thirty years since money laundering was declared a federal crime, businesses have had to walk a fine line between serving customers and serving the government. And since only one of those two parties has the power to shut down a business and throw business owners and employees into prison, guess whose wishes the business owner is going to follow more often? The assumption on the part of government today is that possession of large amounts of cash is indicative of involvement in illegal activity. If you’re traveling with thousands of dollars in cash and get pulled over by the police, don’t be surprised when your money gets seized as “suspicious.” And if you want your money back, prepare to get into a long, drawn-out court case requiring you to prove that you came by that money legitimately, just because the courts have decided that carrying or using large amounts of cash is reasonable suspicion that you are engaging in illegal activity. Because of that risk of confiscation, businesses want to have less and less to do with cash, as even their legitimately-earned cash is subject to seizure by the government. Restrictions on the use of cash are just some of the many laws that pervert the actions of a market economy. Rather than serving consumers, businesses are forced to serve the government first and consumers last. Businesses act as unpaid tax agents, collecting sales taxes for state governments and paying excise taxes to the federal government, the costs of which they pass on to their customers. Businesses act as enforcers of vice laws, refusing tobacco sales to those under eighteen or alcohol to those under twenty-one. Financial institutions, which includes coin dealers, jewelers, and casinos, are required to report cash transactions above $10,000 as well as any activity the government might deem “suspicious.” Cash becomes such a hassle that it is almost radioactive, and many businesses would rather not deal with the burden. Using cash to buy a house is becoming impossible and it is probably only a matter of time before purchasing a car with cash will become incredibly difficult also. Centuries-old legal protections have been turned on their head in the war on cash. Guilt is assumed, while the victims of the government’s depredations have to prove their innocence. Governments having far more time and money to devote to asset forfeiture cases than the citizenry, most victims of cash seizures decide to capitulate rather than attempt a Pyrrhic victory. Those fortunate enough to keep their cash away from the prying hands of government officials find it increasingly difficult to use for both business and personal purposes, as wads of cash always arouse suspicion of drug dealing or other black market activity. And so cash continues to be marginalized and pushed to the fringes. Stemming the anti-cash tide will require a societal attitudinal adjustment that views cash not as something associated with crime, but as a bastion of consumer freedom and a bulwark against overzealous governments. |

|||

Germany Unveils "Cash Controls" Push: Ban Transactions Over €5,000, €500 Euro NoteIt was just two days ago that Bloomberg implored officials to “bring on a cashless future” in an Op-Ed that calls notes and coins “dirty, dangerous, unwieldy, and expensive.” You probably never thought of your cash that way, but increasingly, authorities and the powers that be seem determined to lay the groundwork for the abolition of what Bloomberg calls “antiquated” physical money. We’ve documented the cash ban calls on a number of occasions including, most recently, those that emanated from DNB, Norway’s largest bank where executive Trond Bentestuen said that although “there is approximately 50 billion kroner in circulation, the Norges Bank can only account for 40 percent of its use.” That, Bentestuen figures, “means that 60 percent of money usage is outside of any control." "We believe," he continues, "that is due to under-the-table money and laundering.” DNB goes on to say that after identifying “many dangers and disadvantages” associated with cash, the bank has “concluded that it should be phased out.” On Tuesday we got the latest evidence that officials across the globe are preparing to institute a cashless “utopia” when Handelsblatt reported (in a piece called "The Death of Cash) that the Social Democrats - the junior partner in Angela Merkel’s coalition government - have proposed a €5,000 limit on cash transactions and the elimination of the €500 note.

Berlin is using a familiar scapegoat to justify the plan: the need to fight "terrorists" and “foreign criminals." “Limits on cash transactions would discourage foreign criminals from coming here to launder money,” says a paper penned by the Social Democrats. “If sums over €5,000 have to pass through traceable bank transactions, laundering would be severely hampered, it adds.” On Wednesday, we got confirmation of the plan from Deputy Finance Minister Michael Meister who told reporters that Germany is proposing a euroarea ban on cash transactions over €5,000 to combat terrorism financing and money laundering. “Since money laundering and terrorism financing are cross-border threats,” it makes sense to adopt a bloc-wide “solution”, but “if a European solution isn’t possible, Germany will move ahead on its own,” he added. This comes at a rather convenient time for policy makers in Europe. Rates are already sitting at -0.30% and are likely to be cut by an additional 10bps in March. But that’s not likely to do anything to curb the disinflationary impulse. Mario Draghi isn’t anywhere close to his inflation target and it says a lot about how ineffective the ECB has been when everyone is relieved to see annual inflation running at the “brisk” pace of 0.4%. As a reminder, the gradual phasing out of cash strips the public of its economic autonomy. Central bankers can only control interest rates down to a certain “lower bound.” Once negative rates are passed on to depositors - and trust us, that’s coming - people will simply start pulling their money out of the bank. The more negative rates go, the faster those withdrawals will be. When you ban cash you eliminate this problem. In a cashless society with a government-managed digital currency there is no effective lower bound. If the economy isn’t doing what a bunch of bureaucrats want it to do, they can simply make interest rates deeply negative, forcing would-be savers to become consumers by making them choose between spending or watching as the bank simply confiscates their money in the name of NIRP. Obviously, banning transactions above €5,000 is a long way from a wholesale ban on cash and several other countries have similar limits on cash transactions. Still, there’s no reason why the same rationale (i.e. fighting terror financing) can’t be applied to smaller sums - or all cash transactions. After all, it’s not as though “foreign criminals” only transact in amounts over €5,000 and since “follow the money” is usually the best way to get to the bottom of a perceived “problem,” having a ledger of everything someone or some group does financially would likely be an effective way to crack down on illicit activity. We would argue that the cost to society of creating an economy wherein people’s economic decisions are completely dictated by small groups of economists far outweighs any benefits that would accrue from using a centrally planned digital currency to deter crime. As for how a cash ban would go over in Germany, we seriously doubt the public would take it laying down given that only 18.7% of transactions in the country involve plastic cards. |

|||

Lacy Hunt – “INFLATION & 10Y UST YIELD HEADED LOWER!”Dr. Lacy Hunt joins FRA Co-Founder Gordon T. Long in an in-depth discussion on the current debt dilemma and the decisions of the Federal Reserve. Dr. Lacy H. Hunt, an internationally known economist, is Executive Vice President of Hoisington Investment Management Company, a firm that manages over $5 billion for pension funds, endowments, insurance companies and others. He is the author of two books, and numerous articles in leading magazines, periodicals and scholarly journals. Included among the publishers of his articles are. Barron’s, The Wall Street Journal, The New York Times, The Christian Science Monitor, the Journal of Finance, the Financial Analysts Journal and the Journal of Portfolio Management. Previously, he was Chief U.S. Economist for the HSBC Group, one of the world’s largest banks, Executive Vice President and Chief Economist at Fidelity Bank and Vice President for Monetary Economics at Chase Econometrics Associates, Inc. A native of Texas, Dr. Hunt has served as Senior Economist for the Federal Reserve Bank of Dallas. Dr. Hunt received his Ph.D. in Economics from the Fox School of Business and Management of Temple University. Furthermore Dr. Hunt served on the Board of Trustees of Temple University from 1987 to 2010 and is now an honorary life trustee. He received the Abramson Award from the National Association for Business Economics for “outstanding contributions in the field of business economics.” He is a life member of the American Finance Association. He was a member of the Economic Advisory Board of the American Bankers Association and Chairman of the Economic Advisory Board of the Pennsylvania Bankers Association. He served on the Monetary and Fiscal Policy Affairs Committee of the National Chamber of Commerce. TACTICS OF THE FED “Debt only works if it generates an income to repay principle and interest.” Research indicates that when public and private debt rises above 250% of GDP it has very serious effects on economic growth. There is no bit of evidence that indicates an indebtedness problem can be solved by taking on further debt. One of the objectives of QE was to boost the stock market, on theory that an improved stock market will increase wealth and ultimately consumer spending. The other mechanism was that somehow by buying Government securities the Fed was in a position to cause the stock market to rise. But when the Fed buys government securities the process ends there. They can buy government securities and cause the banks to surrender one type of government asset for another government asset. There was no mechanism to explain why QE should boost the stock market, yet we saw that it did. The Fed gave a signal to decision makers that they were going to protect financial assets, in other words they incentivized decision makers to view financial assets as more valuable than real assets. So effectively these decision makers transferred funds that would have gone into the real economy into the financial economy, as a result the rate of growth was considerably smaller than expected. “In essence the way in which it worked was by signaling that real assets were inferior to financial assets. The Fed, by going into an untested program of QE effectively ended up making things worse off.” THE FLATTENING YIELD CURVE “Monetary policies currently are asymmetric. If the Fed tried to do another round of QE and/or negative interest rates, the evidence is overwhelming that will not make things better. However if the Fed wishes to constrain economic activity, to tighten monetary conditions as they did in December; those mechanisms are still in place.” They are more effective because the domestic and global economy is more heavily indebted than normal. The fact we are carrying abnormally high debt levels is the reason why small increases in interest rate channels through the economy more quickly. If the Fed wishes to tighten which they did in December then sticking to the old traditional and tested methods is best. They contracted the monetary base which ultimately puts downward pressure on money and credit growth. As the Fed was telegraphing that they were going to raise the federal funds rate it had the effect of raising the intermediate yield but not the long term yields which caused the yield curve to flatten. It is a signal from the market place that the market believes the outlook is lower growth and lower inflation. When the Fed tightens it has a quick impact and when the Fed eases it has a negative impact. The critical factor for the long bond is the inflationary environment. Last year was a disappointing year for the economy, moreover the economy ended on a very low note. There are outward manifestations of the weakening in economy activity. One impartial measure is what happened to commodity prices, which are of course influenced by supply and demand factors. But when there are broad declines in all the major indices it is an indication of a lack of demand. The Fed tightened monetary conditions into a weakening domestic global economy, in other words they hit it when it was already receding, which tends to further weaken the almost non-existent inflationary forces and for an investor increases the value. FAILURE OF QUANTITATIVE EASING “If you do not have pricing power, it is an indication of rough times which is exactly what we have.” The fact that the Fed made an ill-conceived move in December should not be surprising to economists. A detailed study was done of the Fed’s 4 yearly forecasts which they have been making since 2007. They have missed every single year. The Fed begins the year with the high forecast and ts declines each forecast after that and by December it isn’t much of a forecast because you already have 11 months of data. An empirical indication that QE has failed is the fact that their models have relied on them to be indications and the models were wrong which means the policies have also been a failure. CRIPPLING NEGATIVES “Another risk which may very well lead to a worse result is the Fed going to negative interest rates. First we must consider if the Fed can engineer negative interest rates and it is very likely they do have that capability. There will be severe consequences which we will not even be able to anticipate.” There is a trend that in weak economic times the fed will continue untested experiments. Even though QE 1, 2 and 3 have failed, in dire times they will implement QE 4. But if the Fed resorted to negative interest rates it will have an adverse impact on bank earnings, particularly small banks and greatly harm savers who have already been hurt. Negative interest rates will simply penalize people to a far greater degree. It will have devastating consequences to the money market mutual funds; difficult to see how they would operate at all. Pushing interest rates in a negative territory will greatly increase the unfunded liabilities of the corporate pension plans. Pension plans will either be dropped or for those already covered it will explode the liabilities causing them to cut expenditures in the real economy to fund the pension liabilities. “If the Fed went into negative interest rates they would ultimately be required to call in the currency and force people to use their bank deposits.” We are no closer to solving our indebtedness problem in 2016 as we were in 2009.

Abstract written by, Karan Singh |

|||

2011 2012 2013 2014 |

|

||

| THEMES - Normally a Thursday "Themes" Post & a Friday "Flows" Post | |||

I - POLITICAL |

|||

CENTRAL PLANNING - SHIFTING ECONOMIC POWER - STATISM

MACRO MAP - EVOLVING ERA OF CENTRAL PLANNING

|

G | THEME | |

| - - CRISIS OF TRUST - Era of Uncertainty | G | THEME | |

CORRUPTION & MALFEASANCE - MORAL DECAY - DESPERATION - RESENTMENT. |

US | THEME PAGE |  |

| - - SECURITY-SURVEILLANCE COMPLEX - STATISM | G | THEME | |

| - - CATALYSTS - FEAR (POLITICALLY) & GREED (FINANCIALLY) | G | THEME | |

II-ECONOMIC |

|||

| GLOBAL RISK | |||

| - GLOBAL FINANCIAL IMBALANCE - FRAGILITY, COMPLEXITY & INSTABILITY | G | THEME | |

| - - SOCIAL UNREST - INEQUALITY & A BROKEN SOCIAL CONTRACT | US | THEME | |

| - - ECHO BOOM - PERIPHERAL PROBLEM | M | THEME | |

| - -GLOBAL GROWTH & JOBS CRISIS | |||

| - - - PRODUCTIVITY PARADOX - NATURE OF WORK | THEME | MA w/ CHS |

|

| 01-08-16 | THEME | MA w/ CHS |

|

| - - - STANDARD OF LIVING - EMPLOYMENT CRISIS, SUB-PRIME ECONOMY | US | THEME | MA w/ CHS |

III-FINANCIAL |

|||

|

FLOWS - Liqudity, Credit & Debt

|

MATA RISK ON-OFF |

THEME |

w/ R Duncan |

|

|||

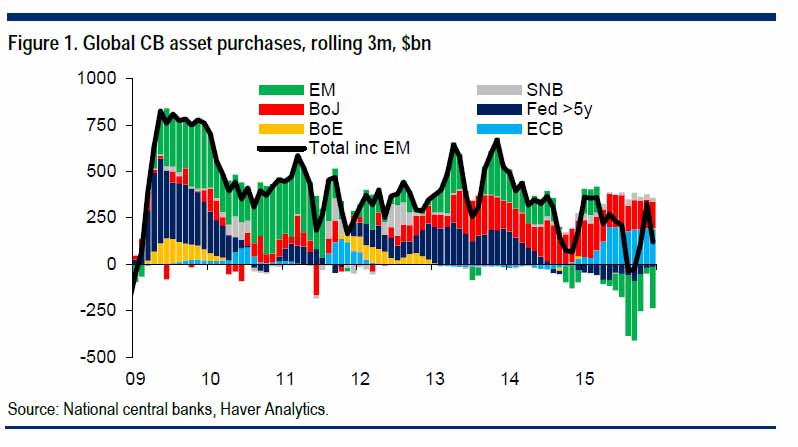

The One Chart Which Explains "Why Markets Are All Falling Down"Yesterday we felt like a brief moment of gloating was deserved, when we noted that, based on the WSJ's reporting, the somber mood among Davos "prominent investors" and billionaires was "irritated, bordering on affronted, with what they say has been central-bank intervention that has gone on too long.... from this anecdotal sampling, at least, that has created growing distortions in nearly all asset prices—from stocks to bonds to real estate." In other words, precisely what we have said all along. But there is much more work to do before the victory lap, most importantly in explaining what happens next. Well, since it is now common knowledge that it is all about central bank and rigged markets, the next logical step is to predict what happens to markets when looking at "asset prices" from a purely central bank liquidity standpoint, aka the Austrian money flow perspective. Here, we remind readers that in early 2013, just as the BOJ was preparing to unleash an epic QE episode in order to offset the lost liquidity injections which the Fed's upcoming taper would lead to, we explained that instead of looking at central banks as standalone entities operating within their own liquidity domains, one has to look at global liquidity as a coordinated whole, one in which every central bank is now an integral cog and where inside money liquidity is not only globally fungible, but transferable from point A to point B at the push of a buy or sell button. And while for the longest time many, including us, were focused on DM central banks, over the past year a new market participant emerged: Emerging Markets, whose $7 trillion in reserve assets had become a source of reverse liquidity, or "quantitative tightening" as dubbed here over the summer, as numerous nations have been forced to liquidate USD-denominated assets to compensate for the loss of trade exports and oil revenue in the aftermath of the death of the Petrodollar which initially was noticed on this site alone and subsequently everywhere else. Which brings us to the topic of this post, namely "why are markets all falling down?" and the answer by Citigroup's iconic, and one of Wall Street's very best, analyst Matt King who adds that "many investors have been struggling to explain the magnitude and violence of the recent sell-off. Why are EM and commodity price weakness proving such negatives for DM as a whole?" The answer, hopefully not a surprise to our readers, is as follows:

We hope that after they see the following chart, which shows not only DM net liquidity injections (i.e., q-easing), but also EM net liquidity outflows (i.e., quantitative tightening) and which explains not only the recent selloff, but also shows how to trade global central bank and sovereign wealth fund and reserve manager flows, all confusion and denial will end.

Or perhaps not. As King himself pessimistically concludes, "Perhaps if this sell-off fizzles out by itself, as it did last October, central banks will again be spared the need to face up to the distortive effect they have had upon markets, and can continue the pretence that markets are still following fundamentals. After all, for many of them, this has been the sell-off which ‘isn’t supposed to be happening’." We couldn't have said it better ourselves. |

|||

| CRACKUP BOOM - ASSET BUBBLE | 12-31-15 | THEME | |

| SHADOW BANKING - LIQUIDITY / CREDIT ENGINE | M | THEME | |

| GENERAL INTEREST |

|

||

| STRATEGIC INVESTMENT INSIGHTS - Weekend Coverage | |||

|

|||

|

SII | ||

|

SII | ||

|

SII | ||

|

SII | ||

| TO TOP | |||

Read More - OUR RESEARCH - Articles Below

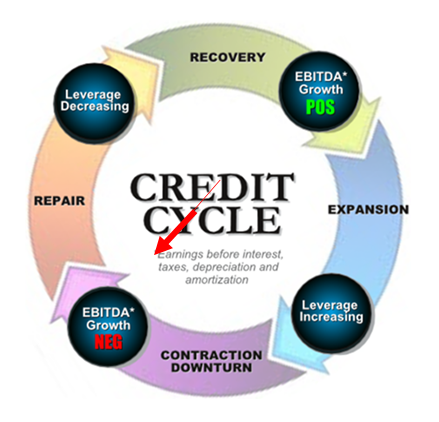

Tipping Points Life Cycle - Explained

Click on image to enlarge

TO TOP

|

YOUR SOURCE FOR THE LATEST THINKING & RESEARCH

|

�

TO TOP