|

JOHN RUBINO'SLATEST BOOK |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

"MELT-UP MONITOR "

Meltup Monitor: FLOWS - The Currency Cartel Carry Cycle - 09 Dec 2013 Meltup Monitor: FLOWS - Liquidity, Credit & Debt - 04 Dec 2013 Meltup Monitor: Euro Pressure Going Critical - 28- Nov 2013 Meltup Monitor: A Regression-to-the-Exponential Mean Required - 25 Nov 2013

|

![]()

"DOW 20,000 "

Lance Roberts Charles Hugh Smith John Rubino Bert Dohman & Ty Andros

|

HELD OVER

Currency Wars

Euro Experiment

Sultans of Swap

Extend & Pretend

Preserve & Protect

Innovation

Showings Below

"Currency Wars "

|

"SULTANS OF SWAP" archives open ACT II ACT III

ALSO Sultans of Swap: Fearing the Gearing! Sultans of Swap: BP Potentially More Devistating than Lehman! |

"EURO EXPERIMENT"

archives open EURO EXPERIMENT : ECB's LTRO Won't Stop Collateral Contagion!

EURO EXPERIMENT: |

![]()

"INNOVATION"

archives open |

"PRESERVE & PROTE CT"

archives open |

Weekend Aug. 15th, 2015

Follow Our Updates

onTWITTER

https://twitter.com/GordonTLong

AND FOR EVEN MORE TWITTER COVERAGE

ANNUAL THESIS PAPERS

FREE (With Password)

THESIS 2010-Extended & Pretend

THESIS 2011-Currency Wars

THESIS 2012-Financial Repression

THESIS 2013-Statism

THESIS 2014-Globalization Trap

THESIS 2015-Fiduciary Failure

NEWS DEVELOPMENT UPDATES:

FINANCIAL REPRESSION

FIDUCIARY FAILURE

WHAT WE ARE RESEARCHING

2015 THEMES

SUB-PRIME ECONOMY

PENSION POVERITY

WAR ON CASH

ECHO BOOM

PRODUCTIVITY PARADOX

FLOWS - LIQUIDITY, CREDIT & DEBT

GLOBAL GOVERNANCE

- COMING NWO

WHAT WE ARE WATCHING

(A) Active, (C) Closed

MATA

Q3 '15- Chinese Market Crash

(A)

Q3 '15-

GMTP

Q3 '15- Greek Negotiations

(A)

Q3 '15- Puerto Rico Bond Default

MMC

OUR STRATEGIC INVESTMENT INSIGHTS (SII)

NEGATIVE-US RETAIL

NEGATIVE-ENERGY SECTOR

NEGATIVE-YEN

NEGATIVE-EURYEN

NEGATIVE-MONOLINES

POSITIVE-US DOLLAR

ARCHIVES

| AUGUST | ||||||

| S | M | T | W | T | F | S |

| 1 | ||||||

| 2 | 3 | 4 | 5 | 6 | 7 | 8 |

| 9 | 10 | 11 | 12 | 13 | 14 | 15 |

| 16 | 17 | 18 | 19 | 20 | 21 | 22 |

| 23 | 24 | 25 | 26 | 27 | 28 | 29 |

| 30 | 31 | |||||

KEY TO TIPPING POINTS |

| 1- Bond Bubble |

| 2 - Risk Reversal |

| 3 - Geo-Political Event |

| 4 - China Hard Landing |

| 5 - Japan Debt Deflation Spiral |

| 6- EU Banking Crisis |

| 7- Sovereign Debt Crisis |

| 8 - Shrinking Revenue Growth Rate |

| 9 - Chronic Unemployment |

| 10 - US Stock Market Valuations |

| 11 - Global Governance Failure |

| 12 - Chronic Global Fiscal ImBalances |

| 13 - Growing Social Unrest |

| 14 - Residential Real Estate - Phase II |

| 15 - Commercial Real Estate |

| 16 - Credit Contraction II |

| 17- State & Local Government |

| 18 - Slowing Retail & Consumer Sales |

| 19 - US Reserve Currency |

| 20 - US Dollar Weakness |

| 21 - Financial Crisis Programs Expiration |

| 22 - US Banking Crisis II |

| 23 - China - Japan Regional Conflict |

| 24 - Corruption |

| 25 - Public Sentiment & Confidence |

| 26 - Food Price Pressures |

| 27 - Global Output Gap |

| 28 - Pension - Entitlement Crisis |

| 29 - Central & Eastern Europe |

| 30 - Terrorist Event |

| 31 - Pandemic / Epidemic |

| 32 - Rising Inflation Pressures & Interest Pressures |

| 33 - Resource Shortage |

| 34 - Cyber Attack or Complexity Failure |

| 35 - Corporate Bankruptcies |

| 36 - Iran Nuclear Threat |

| 37- Finance & Insurance Balance Sheet Write-Offs |

| 38- Government Backstop Insurance |

| 39 - Oil Price Pressures |

| 40 - Natural Physical Disaster |

Reading the right books?

No Time?

We have analyzed & included

these in our latest research papers Macro videos!

OUR MACRO ANALYTIC

CO-HOSTS

John Rubino's Just Released Book

Charles Hugh Smith's Latest Books

Our Macro Watch Partner

Richard Duncan Latest Books

MACRO ANALYTIC

GUESTS

F William Engdahl

OTHERS OF NOTE

Book Review- Five Thumbs Up

for Steve Greenhut's Plunder!

![]()

TODAY'S TIPPING POINTS

|

Have your own site? Offer free content to your visitors with TRIGGER$ Public Edition!

Sell TRIGGER$ from your site and grow a monthly recurring income!

Contact [email protected] for more information - (free ad space for participating affiliates).

HOTTEST TIPPING POINTS |

Theme Groupings |

||

| STUDIES - MACRO pdf | |||

We post throughout the day as we do our Investment Research for: LONGWave - UnderTheLens - Macro

|

|||

|

MOST CRITICAL TIPPING POINT ARTICLES TODAY

|

|

||

Aug 12, 2015 MARKETS

Oil supply grows at ‘breakneck speed’IEA predicts crude glut to last well into 2016 Aug 12, 2015 MARKETS

Canadian oil sands crude halves in pricePrices drop 50% in six weeks to $23 a barrel |

08-15-15 | SII ENERGY |

|

� Recall crude oil’s dramatic 2008 price collapse. The high that year was in July at $147.50 a barrel. By December, the price had plummeted to $30.28. This chart shows how Elliott Wave Theorist subscribers were warned ahead of time.

It was a few weeks before the top when the Theorist said, “Crude Oil: One of the greatest commodity tops of all time is due very soon.”

Eventually oil did climb back above $100 a barrel. But it took two-plus years, and even then prices remained far below the July 2008 high.

Crude traded roughly sideways through June 2014. Then came another nosedive, and about nine months later crude was trading below $44 a barrel.

Once again, subscribers were warned weeks ahead of time. Here’s what the May 2014 Theorist said:

“The multi-year outlook is for much lower prices.”

After oil’s relentless multi-month decline, the January 2015 Theorist said that “now that bearish conviction has crystallized, oil is likely to rally.”

By May 5, oil’s price climbed to just above $60 a barrel. Yet as our long-term analysis suggested, the bounce was relatively short-lived:

“US oil settles at a six-year low of $43.08 a barrel” (CNBC, Aug. 11).

Where are oil prices headed?

Well, one prominent financial observer has been consistent with his outlook for oil.

“Gary Shilling thinks the price of oil is going way lower. The economist and financial analyst wrote an op-ed for Bloomberg View discussing the various reasons why he thinks the price could get down to $10-20 per barrel” (Business Insider, Feb. 17).

Shilling is a deflationist. In an Aug. 3 tweet he reiterated his oil forecast: “Prices will drop even further.”

As always, there are voices saying the glass is half full: The founder of a financial firm recently told CNBC that “Oil does not have much more of a downside left.”

Time will tell which of these forecasts is correct.

Consider the bigger picture – namely the downtrend in other commodities (like copper). Think about the economic weakness in Europe and now China. Consider the record levels of global debt. Reflect on the ineffective stimulus efforts of central banks around the world. And finally, consider this excerpt from the July Theorist:

People who are afraid that deflation will lead to economic contraction are correct. That’s why the subtitle of Conquer the Crash includes both words: Deflationary Depression. But the trip to the finish line is a zigzag path. Results don’t show up overnight. What’s happening now is nothing compared to what’s coming.

"Peak Oil" -- And Other Ways Crude Oil Fooled Almost Everyone

Remember "Peak Oil"? About ten years ago, it was a hugely popular theory "explaining" why oil prices would only go higher. They didn't. These excerpts from Robert Prechter's Elliott Wave Theorist highlight the flaws in the conventional approach to forecasting oil prices and show you a better method -- a method that has done a remarkable job forecasting the future path of oil prices.

|

|||

| MOST CRITICAL TIPPING POINT ARTICLES THIS WEEK - August 09th, 2015 - August 15th, 2015 | |||

| BOND BUBBLE | 1 | ||

| RISK REVERSAL - WOULD BE MARKED BY: Slowing Momentum, Weakening Earnings, Falling Estimates | 2 | ||

| GEO-POLITICAL EVENT | 3 | ||

| CHINA BUBBLE | 4 | ||

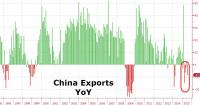

CHINA - Yuan Devaluation China Enters Currency War - Devalues Yuan By Most On Record Submitted by Tyler Durden on 08/10/2015 - 21:32 Submitted by Tyler Durden on 08/10/2015 - 21:32

As we first warned in March, and as became abundantly clear over the weekend when weaker than expected export data as well as the steepest decline in factory gate prices in six years underscored the extent to which the engine of global growth and trade has officially stalled, Beijing has no choice but to join the global currency wars, as the yuan's dollar peg will ultimately prove to be too painful going forward. And sure enough this evening the PBOC weakens the Yuan fix by the most on record. As the details sink in, the Chinese currency complex is collapsing... 12 month NDFs just hit a new 5 year lows against the USD. China's Historic Devaluation Sends Equity Futures, Oil, Bond Yields Sliding, Gold Spikes Submitted by Tyler Durden on 08/11/2015 - 06:48 Submitted by Tyler Durden on 08/11/2015 - 06:48

If yesterday it was the turn of the upside stop hunting algos to crush anyone who was even modestly bearishly positioned in what ended up being the biggest short squeeze of 2015, then today it is the downside trailing stops that are about to be taken out in what remains the most vicious rangebound market in years, in the aftermath of the Chinese currency devaluation which weakened the CNY reference rate against the USD by the most on record, in what some have said was an attempt by China to spark its flailing SDR inclusion chances, but what was really a long overdue reaction by an exporter country having pegged to the strongest currency in the world in the past year. China "Loses Battle Over Yuan", And Now The Global Currency War Begins Submitted by Tyler Durden on 08/11/2015 - 04:40 Submitted by Tyler Durden on 08/11/2015 - 04:40

Almost exactly seven months ago, on January 15, the Swiss National Bank shocked the world when it admitted defeat in a long-standing war to keep the Swiss Franc artificially weak, and after a desperate 3 year-long gamble, which included loading up the SNB's balance sheet with enough EUR-denominated garbage to almost equal the Swiss GDP, it finally gave up and on one cold, shocking January morning the EURCHF imploded, crushing countless carry-trade surfers. Fast forward to the morning of August 11 when in a virtually identical stunner, the PBOC itself admitted defeat in the currency battle, only unlike the SNB, the Chinese central bank had struggled to keep the Yuan propped up, at the cost of nearly $1 billion in daily foreign reserve outflows, which as this website noted first months ago, also included the dumping of a record amount of US government treasurys. Who Could Have Possibly Foreseen China's Shocking Devaluation? Submitted by Tyler Durden on 08/11/2015 - 03:46 Submitted by Tyler Durden on 08/11/2015 - 03:46

Well, pretty much anyone who is not an economist or Wall Street "strategist" because a mercantilist, export-dominated nation pegged to a currency that has appreciated by an unprecedented amount in the past year, is grounds for nothing short of disaster, or using the parlance of our times, a "hard-landing." Case in point: this is what we said just two days ago when the news of China's dramatic trade collapse hit in a post titled: "Chinese Trade Crashes, And Why A Yuan Devaluation Is Now Just A Matter Of Time"...

|

08-11-15 | CHINA | 4 - China Hard Landing |

| Posted by Bloomberg Brief | |||

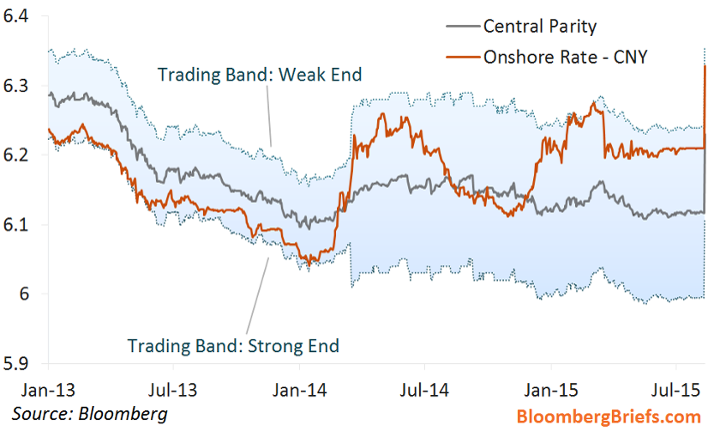

Devaluation Promises to Boost Exports, But Adds Stability Risk China's central bank has signaled a new stage in the management of the yuan and opened the door to depreciation to support export competitiveness. The People's Bank of China adjusted the yuan central parity — the daily fixing used to guide the market — down 1.9 percent today, the largest drop on record. The central bank also said that, going forward, the central parity will closely reflect the market price. That marks a significant shift in policy, as the central bank ends its eight-month resistance to market pressure for yuan depreciation. The direction of travel from the market is clear. At 6 a.m. New York time, the spot price had already fallen to 6.3250 to the dollar, from 6.2097 at Monday's close.

The PBOC's move reflects the depth of concern about China's growth, which threatens to fall below the government's 7 percent target for the year. Exports contracted 8.9 percent year on year in July as a 14 percent annual appreciation in the real effective exchange rate choked off demand. The timing likely also reflects concern that as the Fed moves toward a first rate hike, a peg to a rising dollar would mean continued appreciation of the yuan against the currency of trade rivals. Reviving flagging exports will require a significantly larger depreciation. Exports year to date have been flat from a year ago. Based on our calculations, a 10 percent depreciation against the dollar would take export growth back to 10 percent year on year, all else being equal. The risk is that depreciation triggers capital flight, dealing a blow to the stability of China's financial system. Our estimate is that a 1 percent yuan depreciation against the dollar would trigger about $40 billion in capital flight. The calculation from China's leaders is likely that, with $3.6 trillion in foreign exchange reserves, substantial bank deposits stashed in reserve at the PBOC, and controls on cross-border flows, they can manage any risks. Assuming a 10 Spot Price, Central Parity and Trading Band See this story on the Bloomberg terminal with additional charts here. percent depreciation triggered $400 billion in capital flight, they would still be left with FX reserves in excess of $3 trillion. Years of yuan appreciation increased the appeal of investment in China and had a broad positive impact on asset prices. Yuan depreciation will have the reverse effect. That's a negative for the struggling equity market and the nascent recovery in real estate — where speculative demand plays a major role. Depreciation will deal a blow to China's hopes for yuan inclusion in the IMF's SDR basket. It will decrease international investors' willingness to hold yuan, and will likely irk the IMF — which has only recently shifted away from its characterization of the currency as undervalued. There are also political economy considerations. President Xi Jinping is set to meet with President Obama in September. Competitive depreciation of the yuan will not make that conversation any easier. Neither will it improve Beijing's relations with regional rivals Tokyo and Seoul, who fear any gain for China's exporters comes at the expense of lower sales for their own firms. China likely views any international protests as a manageable second-order consideration. That's especially true as they can legitimately present depreciation as driven by the market, and other major central banks have adopted policies that promote exchange-rate depreciation. In terms of China's longer-term rebalancing agenda, we give the central bank credit for finding a policy that combines stimulus and reform. A weaker yuan will provide a boost to growth. A more market-set exchange rate is in line with the direction of travel set at the Third Plenum, and will promote more efficient allocation of productive resources. Looking at the historical data as a guide to the possible extent of coming moves, the biggest three-month yuan move on record was a 4.2 percent appreciation at the start of 2008. It would take a 14 depreciation to take the yuan back to mid-2014 levels, when its latest period of appreciation in real effective terms started.

|

|||

| JAPAN - DEBT DEFLATION | 5 | ||

EU BANKING CRISIS |

6 |

||

| TO TOP | |||

| MACRO News Items of Importance - This Week | |||

GLOBAL MACRO REPORTS & ANALYSIS |

|||

US ECONOMIC REPORTS & ANALYSIS |

|||

| CENTRAL BANKING MONETARY POLICIES, ACTIONS & ACTIVITIES | |||

| Market | |||

| TECHNICALS & MARKET |

|

||

CANARIES - Warnings Everywhere! The Investment Legends Are Preparing For a Crash Graham Summers, Phoenix Capital More and more insiders are warning of a potential systemic event. The first sign of real trouble concerned a number of investment legends choosing to close shop and return investors’ capital. Stanley Druckenmiller

Carl Icahn

Seth Klarman

Even the perma-bulls are speaking with their actions. Warren Buffett

Beyond the legends, institutional investors have been net sellers of stocks in 2014 and on into 2015. The same goes for hedge funds. Do you think they’d be doing this if they thought stocks were offering a lot of opportunities and value today? Ian Spreadbury - Fidelity And finally, we get to today, where one of the largest asset managers in the world at Fidelity stated that we are heading for a “systemic event... similar to 2008” and that owning precious metals and physical cash is a good idea. The punch line? This was a bond fund manager. One of the class of investors who have poo poo’d Gold and physical cash in the past because those assets pay next to or no dividend. And even HE is warning that it’s time to take safety and prepare. Smart investors should take note of this now. It is a MAJOR red flag to be watched closely.

|

08-12-15 | CANARIES | |

Via The Telegraph:

As The Telegraph notes, this is "an unusual" piece of advice coming from "a mainstream strategist" and it suggests the "serious people" are starting to realize that a certain tin foil hat fringe blog — which can already count LIBOR manipulation and HFT proliferation as examples of conspiracy theories turned world-changing conspiracy facts — may be correct to warn that if the current state of affairs persists for much longer, the "market" may one day be halted and simply never reopen. |

|||

| COMMODITY CORNER - AGRI-COMPLEX | PORTFOLIO | ||

| SECURITY-SURVEILANCE COMPLEX | PORTFOLIO | ||

| THESIS - Mondays Posts on Financial Repression & Posts on Thursday as Key Updates Occur | |||

| 2015 - FIDUCIARY FAILURE | 2015 | THESIS 2015 |  |

| 2015 - FIDUCIARY FAILURE | 2015 | THESIS 2015 | |

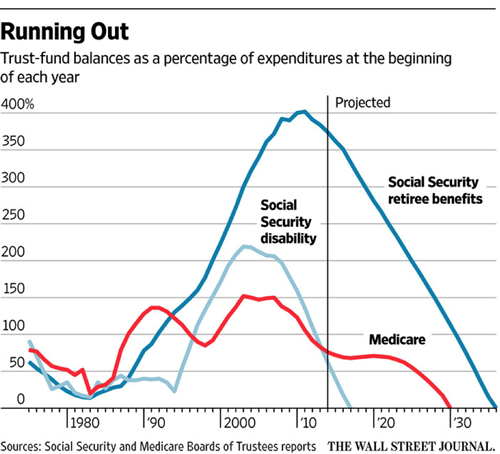

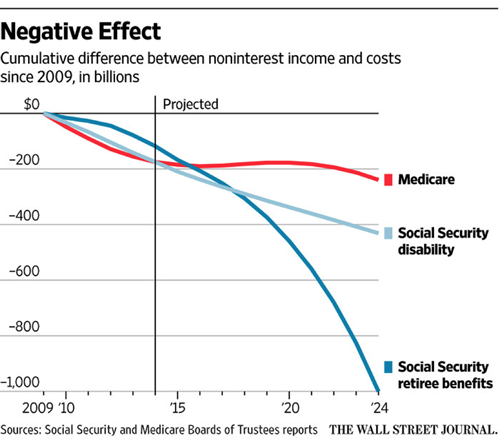

CANARIES - Warnings Everywhere! The Long-Range Social Security/Medicare Deficit: $72 Trillion And Countingby Forbes • August 11, 2015By John C. Goodman for Forbes The Social Security/Medicare Trustees have issued their latest reports and they are not easy reading for the uninitiated. I suspect most of the Trustees hope you don’t read them at all. They prefer their own spin. Under both Republican and Democratic administrations, these reports are invariably accompanied by a press release that completely ignores what is important and focuses instead on what is unimportant. What’s unimportant? The trust funds and when they will run dry. Like most social security systems in the world today, ours is a pay-as-you-go system. Nothing has been saved or invested. What we call trust funds consist of nothing more than IOUs the government has written to itself. (More on that below.) Yet, that is what the official press releases emphasize and this focus is reflected in the first graph below. What’s important? Cash flow. In fact, in a pay-as-you-go system, cash flow is the only thing that matters. As the second graph shows, Social Security and Medicare are paying out more than they are taking in. As the baby boomers retire, the total deficit will grow dramatically. Currently, we are using about one in every seven general revenue dollars to cover these deficits. By 2020, we will need more than one in five. By 2030, we will need about one in three. That implies that in order to fund Social Security and Medicare benefits at their current levels and at the same time balance the budget, in just five years the federal government will need to stop doing about one out of every five other things it is currently doing. In just 15 years, the government will need to stop doing about one out of three other things it is currently doing. Clearly, elderly entitlements are on a course to crowd out all other federal programs. Although the trust funds do not hold valuable assets that can be used to pay benefits, they are useful for another reason. As Figure I shows, trust fund accounting keeps tract of the inflow and outflow of funds related to our entitlement programs over time. Up until sometime in the first decade of the twenty first century, Social Security, Medicare (Part A) and the Disability trust funds were collecting in taxes and premiums more than they paid out in benefits. Today, however, all three programs are paying out more than they are taking in. Figure II shows how this negative cash flow is accumulating. In conventional media accounts, the trust funds will “run out of money” when the lines on the graph in Figure I cross the x-axis and become negative. This will occur next year for the Disability program. For Medicare Part A, it will occur in 2030. For Social Security retirement, it will occur in 2035. Of course, there is no “money” to run out of. But those are the dates in which Congress and the President must act. If they fail to act, the Treasury will be required to reduce benefit payments to the point where they equal the income (taxes and premiums) into each of the programs. The Disability program, for example, will only be able to pay 80 percent of promised benefits – beginning next year. FIGURE I

FIGURE II

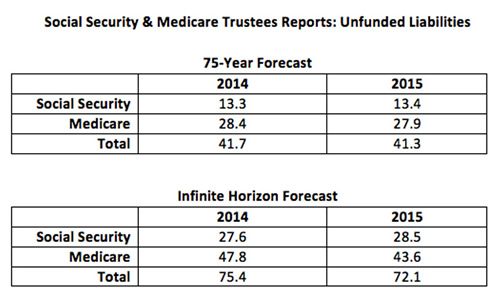

If we have a debt that is growing through time, the natural question to ask is: What is the value of that debt in current dollars? The Trustees actually answer that question. But the answer is buried deep in the report and camouflaged in various ways that require expert deciphering. The table below reflects calculations by former Trustee Thomas Saving and his colleague Andrew Rettenmaier. As the table shows, promises we have made minus expected premiums and dedicated taxes total $41.3 trillion over the next 75 years .

(SOURCE: Calculations by Thomas Saving and Andrew Rettenmaier based onTHE 2015 ANNUAL REPORT OF THE BOARD OF TRUSTEES OF THE FEDERAL OLD-AGE AND SURVIVORS INSURANCE AND FEDERAL DISABILITY INSURANCE TRUST FUNDS and 2015 ANNUAL REPORT OF THE BOARD OF TRUSTEES OF THE FEDERAL HOSPITAL INSURANCE AND FEDERAL SUPPLEMENTARY MEDICAL INSURANCE TRUST FUNDS.) Since 75 years is such a long way off, why do we need anything more than that? Think about the person who is about to retire in the 75th year. A 75-year projection would count all the taxes this individual is expected to pay, but it would ignore all the benefits he expects to receive based on those taxes. So cutting off our projection in the 75th year, or any other year, seriously understates the debt we are amassing. That’s why economists prefer to extend the analysis indefinitely into the future. After doing that, the Trustees tell us that our total unfunded liability is $72.1 trillion. Yet even this number is almost certainly too low. It assumes that (Obamacare) cuts in Medicare spending are sustainable. That is, when seniors cannot find doctors who will see them or facilities that will admit them and access to care for Medicare enrollees is even worse than it is for people in Medicaid, Congress will ignore the complaints of the elderly. If that doesn’t happen (and almost no one in Washington thinks it will happen), then the true unfunded liability is more than $100 trillion – roughly six times the size of our entire economy. As I promised, back to the trust funds. Pay-as-you-go means every dollar collected in payroll taxes is spent. It is spent the very day, the very hour, the very minute that it comes in the door. Nothing is saved. Nothing is invested. The payroll taxes contributed by today’s workers pay the benefits of today’s retirees. When today’s workers retire, their benefits will have to be paid by future taxpayers. Like other government trust funds (highway, unemployment insurance, and so forth), the Social Security Trust Fund exists purely for accounting purposes: to keep track of surpluses and deficits, and the inflow and outflow of funds. The accumulated Social Security surplus actually consists of paper certificates (non-negotiable bonds) kept in a filing cabinet in a government office in West Virginia. (Medicare avoids the paperwork by doing the accounting electronically.) These bonds cannot be sold on Wall Street or to foreign investors. They can only be returned to the Treasury. In essence, they are IOUs the government writes to itself. Every payroll tax check signed by employers is written to the U.S. Treasury. Every Social Security benefit check comes from the U.S. Treasury. The trust funds neither receives money nor disburses it. Moreover, every asset of the trust funds is a liability of the Treasury. Summing over both agencies, the balance is zero. For the Treasury to write a check, it must first tax or borrow Source: How Much Do We Owe? $72 Trillion And Counting – Forbes |

2015 | THESIS 2015 | |

| 2014 - GLOBALIZATION TRAP | 2014 |  |

|

|

|||

|

2013 2014 |

|

||

FINANCIAL REPRESSION - UPDATE

The Disappearing Retirement Fund International Man's Jeff Thomas points to the unprecedented financial & economic challenges & crises in the indebted developed world .. Thomas is very pessimistic about the retirement situation for Americans, Canadians, Europeans .. he thinks their investments in their pension funds will diminish dramatically in value or disappear .. for example, on U.S. social security, "Ergo, each year, those working will need to be taxed more heavily if the system is to continue. Unfortunately, at some point, we reach the tipping point and the concept itself is no longer viable. After that point, benefits will be reduced and, possibly, eliminated altogether." .. in regard to private pension funds like 401Ks, Thomas sees the risks of a stock market crash as bringing down the value of these funds, even if the funds are so-called "diversified" .. but there's more - there are now new risks from governments desperately in search of funds to keep their operations & public pensions going .. "When governments find themselves on the verge of insolvency, they invariably react the same way: go back to the cash cow for a final milking. Each of the jurisdictions that is in trouble at present, has, in its playbook, the same collection of milking techniques. One of those will have a major impact on pensions: the requirement that pension plans must contain a percentage of government Treasuries .. Legislation will be created to ensure that a percentage be in Treasuries, which are 'guaranteed' .. Sounds good. And people will be grateful. Unfortunately, the body that is providing the guarantee is the same body that has created the economic crisis. And if the government is insolvent, the 'guarantee' will become just one more empty promise. Recently, the U.S. Supreme Court ruled that employers have a duty to protect workers invested in their 401(k) plans from mutual funds that perform poorly or are too expensive. By passing this ruling, the US government has the power to seize private pension funds “to protect pensioners”. It also has the authority to dictate how funds may be invested. The way is now paved for the requirement that 401(k)s be invested heavily in US Treasuries."

Financial Repression Will Intensify as Central Bank/Government Policy Options Become Limited Economist Satyajit Das sees increasing methods of financial repression being employed by governments as policy options become limited .. Introduced in 1973 by economists Edward Shaw & Ronald McKinnon, the term refers to measures implemented by governments to channel savings & funds to finance the public sector, lower its borrowing costs & liquidate debt .. Das sees new taxes, means testing, user pay surcharges all coming .. "Entitlement liabilities, such as retirement benefits, will be managed by increasing the allowable minimum retirement age, reducing benefit levels, linking to actual contribution by individuals over their working life, and eliminating inflation indexation. Many of these policies will be packaged as socially and ethically progressive initiatives, belying the financial imperatives." .. points out in a 2013 study, the McKinsey Global Institute found that between 2007 & 2012, interest rate & quantitative easing (QE) policies resulted in a net transfer to governments in the United States, Britain & the eurozone of $1.6 trillion (£1.03 trillion), through reduced debt-service costs & increased central bank profits - "The losses were borne by households, pension funds, insurers and foreign investors. Households in these countries together lost $630bn in net interest income, with the major losses being borne by older households with significant interest-bearing assets. Non-financial corporations in these countries also benefited by $710bn through lower debt service costs." .. Das also sees deliberate devaluation as another financial repression mechanism .. regulations are another mechanism: "Governments can legislate minimum mandatory holdings of government securities for banks, pension funds and insurance companies. New liquidity regulations already require increased holdings of government bonds by banks and insurers." .. wealth confiscation is yet another mechanism - seizing savings or pension fund assets like in 2013 when Spain drew €5bn (£3.5bn) from the state’s Social Security Reserve Fund, designed to guarantee pension payments in times of hardship .. nationalizations are yet another mechanism .. "Debt monetization and the resultant loss of purchasing power effectively represent a tax on holders of money and sovereign debt. They redistribute real resources from savers to borrowers and the issuer of the currency, resulting in diminution of wealth over time. This highlights the reliance on financial repression, explicitly seeking to reduce the value of savings. Ultimately, the policies being used to manage the crisis punish frugality and thrift, instead rewarding borrowing, profligacy, excess and waste."

Germany Replacing Bank Cards and Eliminating Cash Withdrawals: Financial Repression Gone Mad Martin Armstrong: "The game is afoot to eliminate CASH .. Already we see the cancellation of such cards and the issuing of new debit cards. Why? The new cards cannot be used at an ATM outside of Germany to obtain cash. Any attempt to get cash can only be an advance on a credit card .. Little by little, these people are destroying everything that held the world economy together .. This will NEVER END NICELY for they can only think about their immediate needs with no comprehension of the future they are creating .. This is total insanity and we are losing absolutely everything that makes society function .. Once they eliminate CASH, they will have total control over who can buy or sell anything."

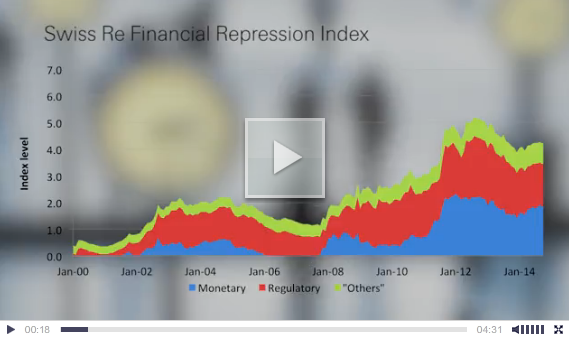

16 June 2015 Swiss Re Meeting: "Sounding the Alarm on Financial Repression" Swiss Re video highlights the recent meeting they held with experts voicing concerns about the ongoing use of unconventional policies .. financial repression is causing financial market distortions & poses a serious risk to financial stability .. These unconventional policies have pushed institutional investors into holding government debt. As a result they have less money available for productive investment, such as infrastructure projects .. "It means that there's a global search for yield. That possibly leads to a misallocation of resources," says Douglas Flint, Group Chairman of HSBC .. Jean-Claude Trichet, Chairman of the Group of Thirty affirms the risks. |

|||

2011 2012 2013 2014 |

|

||

| THEMES - Normally a Thursday Themes Post & a Friday Flows Post | |||

I - POLITICAL |

|||

| CENTRAL PLANNING - SHIFTING ECONOMIC POWER - STATISM | THEME | ||

- - CORRUPTION & MALFEASANCE - MORAL DECAY - DESPERATION, SHORTAGES. |

THEME |  |

|

| - - SECURITY-SURVEILLANCE COMPLEX - STATISM | M | THEME | |

| - - CATALYSTS - FEAR (POLITICALLY) & GREED (FINANCIALLY) | G | THEME | |

II-ECONOMIC |

|||

| GLOBAL RISK | |||

| - GLOBAL FINANCIAL IMBALANCE - FRAGILITY, COMPLEXITY & INSTABILITY | G | THEME | |

| - - SOCIAL UNREST - INEQUALITY & A BROKEN SOCIAL CONTRACT | US | THEME | |

| - - ECHO BOOM - PERIPHERAL PROBLEM | M | THEME | |

| - -GLOBAL GROWTH & JOBS CRISIS | |||

| - - - PRODUCTIVITY PARADOX - NATURE OF WORK | THEME | MACRO w/ CHS |

|

| - - - STANDARD OF LIVING - EMPLOYMENT CRISIS, SUB-PRIME ECONOMY | US | THEME | MACRO w/ CHS |

III-FINANCIAL |

|||

| FLOWS -FRIDAY FLOWS | MATA RISK ON-OFF |

THEME |  |

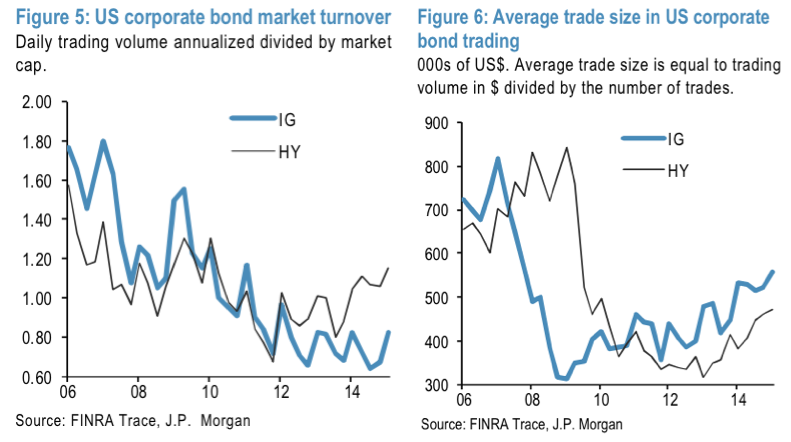

The Complete Guide To ETF Phantom LiquidityTwo months ago, in “ETF Issuers Quietly Prepare For Meltdown With Billions In Emergency Liquidity,” we outlined the rather disconcerting circumstances that have led some large fund managers to quietly line up emergency liquidity facilities that can be tapped in the event of a sudden retail exodus from bond funds. "The biggest providers of exchange-traded funds, which have been funneling billions of investor dollars into some little-traded corners of the bond market, are bolstering bank credit lines for cash to tap in the event of a market meltdown. Vanguard Group, Guggenheim Investments and First Trust are among U.S. fund companies that have lined up new bank guarantees or expanded ones they already had, recent company filings show," Reuters reported at the time, in a story we suspect did not get the attention it deserved. At a base level, these precautionary measures are the result of the interplay between central bank policy and the unintended consequences of the post-crisis regulatory regime. ZIRP creates a hunt a for yield and simultaneously incentivizes companies (especially cash strapped companies) to tap the bond market while borrowing costs remain artificially suppressed. Clearly, this is a self-fulfilling prophecy. The longer rates on risk free assets remain near, at, or even below zero, the more demand there is for new corporate issuance (the rationale being that at least corporate credit offers some semblance of yield). More demand means rates on corporate credit are driven still lower, and once yields on high grade issues get close to the lower limit, yield-starved investors are then herded into HY. All of this supply in the primary market comes at a time when liquidity in the secondary market for corporate credit is non-existent thanks to the shrinking dealer books that resulted from the government’s (maybe) well-meaning attempt to crack down on prop trading. The result: a crowded theatre with a tiny exit. This situation has been exacerbated by the proliferation of bond ETFs which have allowed retail investors to pile into corners of the fixed income world where they might not belong. All of the above can be summarized as follows. "MF assets too large versus dealer inventories" (via Citi)...

... clear evidence of "structural damage in corporate bond trading liquidity" (via JP Morgan)...

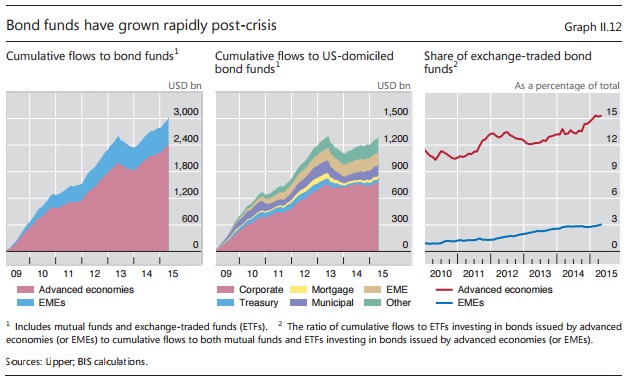

... and the rapid growth of bond funds in the post-crisis world (via BIS)...

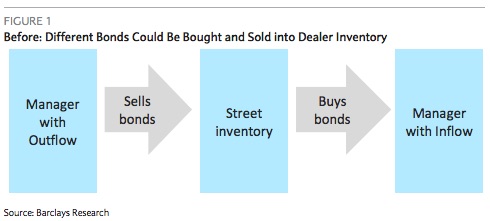

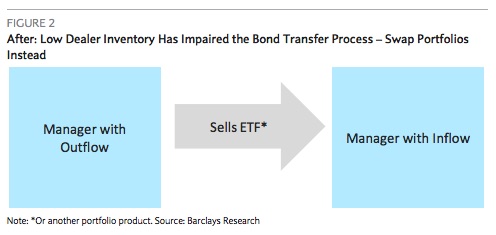

So given the above, the question is this: if something were to spook the market - a rate hike cycle for instance, or an October revolver raid on HY energy names, or an exogenous geopolitical shock - causing an exodus from these funds, what would happen to prices if fund managers were suddenly forced to transact in size in an illiquid secondary market in order to meet redemptions? "Nothing good", is the answer. The solution is to avoid selling the underlying bonds - even when investors are selling their shares in the funds. But how is this possible? To a certain extent, outflows in one fund can be offset by inflows to another. These "diversifiable flows" are one happy byproduct of the great ETF proliferation. Here's a refresher on how this works courtesy of Barclays. * * * Portfolio Products Replace Dealer Inventory While diversifiable flows limit the risks to portfolio managers in principle, the reality of the high yield market is more complicated. Managers have specific views on tenor, callability, sectors, covenants, and, most importantly, individual credits, such that actually finding buyers for specific bonds can be quite difficult. In the pre-crisis period, dealers ran large inventories that effectively facilitated the netting of flows across funds (Figure 1). A fund with an outflow would sell bonds into the dealer community, and funds with outflows would buy bonds out of the dealer inventory. When inventory is large, the fact that the specific bonds bought and sold did not match was largely irrelevant. Funds with outflows could sell the bonds of their choice, and the funds with inflows could pick investments from the large variety of inventory held by dealers.

The matching problem has become more acute as dealer inventories have declined. Even funds can net flows in principle, dealers are much less willing to warehouse bonds, and are much more likely to buy only when they believe they can quickly offload the risk. Under this scenario, the fact that flows can theoretically be netted is of little practical use to fund managers – actually netting individual bonds is extremely difficult, particularly in the short time frame required by funds offering daily liquidity to end investors. This is where portfolio products come in. Investors can use portfolio products to fund outflows/invest inflows immediately and execute the necessary single-name bond trades over time as liquidity in the underlying bond market allows (Figure 2). In this scenario, funds with inflows and outflows simply exchange portfolio products, sidestepping the immediate need to trade single-name corporate bonds.

* * * Ok great, so ETFs provide a kind of "phantom" liquidity if you will. There are two problems with this:

Here's how we put it last month in "How Fund Managers Use ETF Phantom Liquidity To Avert A Meltdown":

So what is a fund manager to do? This is where we come full circle to the emergency liquidity lines mentioned at the outset. In order to avoid tapping the underlying illiquid bond market in a situation where flows are unidirectional, fund managers may instead pay out redemptions in borrowed cash. This is, to quote Citi's Matt King, "creative destruction destroyed." Only worse. That is, this represents the willful delay of a long overdue episode of creative destruction layered atop another delay of the much needed Schumpeterian endgame. Stripping out the metaphysics and philosophy references, that can be translated as follows: this strategy is yet another example of delaying the inevitable. If fund managers are forced to tap these liquidity lines it likely means investors have found a reason to sell en masse and if that reason turns out to be something that permanently impairs the value of the underlying bonds (as opposed to a transitory, irrational panic) then all the funds are doing by borrowing to meet redemptions is employing leverage to stave off the recognition of losses, which is ironically the same thing (in principle anyway) that the companies whose bonds they’re holding have done to stay in business. It’s a delay-and-pray scheme designed to avoid selling the debt of companies whose similar delay-and-pray schemes have run their course. In closing, it's important to note that no fund manager in the world will be able to line up enough emergency liquidity protection to avoid tapping the corporate credit market in the event of panic selling in the increasingly crowded market for bond funds. In other words, when the exodus comes, the illiquidity that's been chasing markets for the better part of seven years will finally catch up, and at that point, all bets are officially off.

|

|||

| CRACKUP BOOM - ASSET BUBBLE | THEME | ||

| SHADOW BANKING - LIQUIDITY / CREDIT ENGINE | M | THEME | |

| GENERAL INTEREST |

|

||

| STRATEGIC INVESTMENT INSIGHTS - Weekend Coverage | |||

|

SII | ||

|

SII | ||

|

SII | ||

|

SII | ||

| TO TOP | |||

Read More - OUR RESEARCH - Articles Below

Tipping Points Life Cycle - Explained

Click on image to enlarge

TO TOP

|

YOUR SOURCE FOR THE LATEST THINKING & RESEARCH

|

�

TO TOP