|

JOHN RUBINO'SLATEST BOOK |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

"MELT-UP MONITOR "

Meltup Monitor: FLOWS - The Currency Cartel Carry Cycle - 09 Dec 2013 Meltup Monitor: FLOWS - Liquidity, Credit & Debt - 04 Dec 2013 Meltup Monitor: Euro Pressure Going Critical - 28- Nov 2013 Meltup Monitor: A Regression-to-the-Exponential Mean Required - 25 Nov 2013

|

![]()

"DOW 20,000 "

Lance Roberts Charles Hugh Smith John Rubino Bert Dohman & Ty Andros

|

HELD OVER

Currency Wars

Euro Experiment

Sultans of Swap

Extend & Pretend

Preserve & Protect

Innovation

Showings Below

"Currency Wars "

|

"SULTANS OF SWAP" archives open ACT II ACT III

ALSO Sultans of Swap: Fearing the Gearing! Sultans of Swap: BP Potentially More Devistating than Lehman! |

"EURO EXPERIMENT"

archives open EURO EXPERIMENT : ECB's LTRO Won't Stop Collateral Contagion!

EURO EXPERIMENT: |

![]()

"INNOVATION"

archives open |

"PRESERVE & PROTE CT"

archives open |

RECAP

Weekend Mar. 23rd, 2014

![]()

Follow Our Updates

on TWITTER

https://twitter.com/GordonTLong

AND FOR EVEN MORE TWITTER COVERAGE

STRATEGIC MACRO INVESTMENT INSIGHTS

2014 THESIS: GLOBALIZATION TRAP

2014 THESIS: GLOBALIZATION TRAP

NOW AVAILABLE FREE to Trial Subscribers

185 Pages

What Are Tipping Poinits?

Understanding Abstraction & Synthesis

Global-Macro in Images: Understanding the Conclusions

| MARCH | ||||||

| S | M | T | W | T | F | S |

| 1 | ||||||

| 2 | 3 | 4 | 5 | 6 | 7 | 8 |

| 9 | 10 | 11 | 12 | 13 | 14 | 15 |

| 16 | 17 | 18 | 19 | 20 | 21 | 22 |

| 23 | 24 | 25 | 26 | 27 | 28 | 29 |

| 30 | 31 | |||||

KEY TO TIPPING POINTS |

| 1 - Risk Reversal |

| 2 - Japan Debt Deflation Spiral |

| 3- Bond Bubble |

| 4- EU Banking Crisis |

| 5- Sovereign Debt Crisis |

| 6 - China Hard Landing |

| 7 - Chronic Unemployment |

| 8 - Geo-Political Event |

| 9 - Global Governance Failure |

| 10 - Chronic Global Fiscal ImBalances |

| 11 - Shrinking Revenue Growth Rate |

| 12 - Iran Nuclear Threat |

| 13 - Growing Social Unrest |

| 14 - US Banking Crisis II |

| 15 - Residential Real Estate - Phase II |

| 16 - Commercial Real Estate |

| 17 - Credit Contraction II |

| 18- State & Local Government |

| 19 - US Stock Market Valuations |

| 20 - Slowing Retail & Consumer Sales |

| 21 - China - Japan Regional Conflict |

| 22 - Public Sentiment & Confidence |

| 23 - US Reserve Currency |

| 24 - Central & Eastern Europe |

| 25 - Oil Price Pressures |

| 26 - Rising Inflation Pressures & Interest Pressures |

| 27 - Food Price Pressures |

| 28 - Global Output Gap |

| 29 - Corruption |

| 30 - Pension - Entitlement Crisis |

| 31 - Corporate Bankruptcies |

| 32- Finance & Insurance Balance Sheet Write-Offs |

| 33 - Resource Shortage |

| 34 - US Reserve Currency |

| 35- Government Backstop Insurance |

| 36 - US Dollar Weakness |

| 37 - Cyber Attack or Complexity Failure |

| 38 - Terrorist Event |

| 39 - Financial Crisis Programs Expiration |

| 40 - Natural Physical Disaster |

| 41 - Pandemic / Epidemic |

Reading the right books?

No Time?

We have analyzed & included

these in our latest research papers Macro videos!

![]()

OUR MACRO ANALYTIC

CO-HOSTS

John Rubino's Just Released Book

![]()

Charles Hugh Smith's Latest Books

![]()

![]()

Our Macro Watch Partner

Richard Duncan Latest Books

MACRO ANALYTIC

GUESTS

F William Engdahl

![]()

![]()

![]()

![]()

![]()

OTHERS OF NOTE

![]()

![]()

![]()

![]()

Book Review- Five Thumbs Up

for Steve Greenhut's

Plunder!

![]()

|

Scroll TWEETS for latest Analysis

Read More - OUR RESEARCH - Articles Below

HOTTEST TIPPING POINTS |

Theme Groupings |

|||||

UKRAINE - The Unfolding Financial Battle

|

||||||

We post throughout the day as we do our Investment Research for: LONGWave - UnderTheLens - Macro |

||||||

"BEST OF THE WEEK "

|

Posting Date |

Labels & Tags | TIPPING POINT or 2014 THESIS THEME |

|||

|

||||||

| MOST CRITICAL TIPPING POINT ARTICLES THIS WEEK - March 16th - March 22nd, 2014 | ||||||

| RISK REVERSAL | 1 | |||||

RISK - Reflexivity Suggests another Crash Is Inevitable Soros’s Reflexivity Suggests another Crash Is Inevitable 03-13-14 Chase Van Der Rhoer, Bloomberg Markets slumped on a toxic brew of headlines about the dismantling of Fannie Mae and Freddie Mac, writedowns from UniCredit, losses at Ceasars Entertainment and escalating tension between the West and the kremlin. Investment-grade corporates responded by widening 1 basis point with a 1:3 tightening to widening ratio, high yield widened 5 basis points with a 1:6 ratio and emerging markets widened 10 basis points with a 1:6 ratio. a market confronted with extreme complexity is obliged to resort to methods of simplification as George Soros points out in a paper entitled “Fallibility, Reflexivity, and the Human Uncertainty Principle.” He argues that interpreting the world, then acting upon that world, with both actions subject to great fallibility, creates a reflexive feedback loop that causes an escalat- ing probability of disaster. When the entanglement of flawed market expectations becomes large enough, Soros says, the market experiences a bust following predictable trends and stages. Echoing this analysis, stock analyst Tom Demark last year pointed to the similarity between the stock market trend that preceded the 1929 crash and the present day. The following two charts are examples of the boom-bust cycles overlaid with today’s equity market. |

03-17-14 | RISK CANARIIES | 1 - Risk Reversal | |||

RISK - Historically, Extended Bull Market Runs Ended Badly

|

03-17-14 | RISK CANARIIES | 1 - Risk Reversal | |||

| JAPAN - DEBT DEFLATION | 2 | |||||

JAPAN - ABE-nomics is Simply Not Working 35th consecutive trade deficit and 8th miss of last 9. |

03-19-14 | JAPAN | 2 - Japan Debt Deflation Spiral | |||

| BOND BUBBLE | 3 | |||||

EU BANKING CRISIS |

4 |

|||||

| SOVEREIGN DEBT CRISIS [Euope Crisis Tracker] | 5 | |||||

| CHINA BUBBLE | 6 | |||||

CHINA - Has an Inflation Problem Will Inflation Collapse the Chinese Economy? 03-19-14 Graham Summers A growing concern for the global economy is inflation. We’ve recently detailed this issue for the US economy earlier this week. Global Central Banks, concerned with a potential deflationary collapse, have allowed inflation to seep into the financial system. In developed nations like the US, this puts a squeeze on consumers. But in emerging markets like China, inflation is outright disastrous. Nearly 40% of China lives off of $2 a day. Your average college graduate in China makes just $2,500 per year. In an economy such as this, a rise in prices in costs of living can be devastating for the population. Why are we not seeing this in the Chinese stock market? In China, the banking monetary mechanism tends to funnel cash directly into the economy, rather than stocks (note that bank lending remains anemic in the US, while the stock market roars higher). Indeed, China’s shadow banking (financial transactions outside of formal banks) has expanded to over 200% of China’s GDP or well north of $18 trillion in dollar terms. This situation favors the well-connected Chinese political elite and lends itself to corruption on an epic scale. Consider the following:

Corrupt officials favor real estate as a means of acquiring assets because they can put properties in relatives’ names. Between this and the fact that stock investing has yet to become a cultural phenomenon in China as it is in the US, China’s stock market has languished while its real estate market has boomed. However, the fact that so much “funny money” has moved into the Chinese economy via so many shadowy conduits makes the Chinese economy a potential inflationary nightmare. The “official” Chinese inflation data won’t show this, but you can see the clear signs:

Inflation is already present in the financial system. The signs are there if you know where to look. The question now is how the markets will adjust as it spreads. |

03-19-14 | CHINA | 6 - China Hard Landing | |||

CHINA - Cracks Beginning to Show The Dominoes Begin To Fall In China 03-18-14 Tim Staermose of Sovereign Man blog VIA ZHForget tapering. Forget Ukraine. The largest single risk to the world economy and financial markets right now is China. What’s going on in China reminds me a lot of what I witnessed firsthand when I lived in South Korea in the 1990s, before that economy’s crash in 1998. Just as China now, South Korea was an immature, state-controlled financial system funneling cheap money to well-connected and politically favored large enterprises. Fuelled by a steady diet of cheap money, these companies kept adding capacity with no regard to profitability or return on capital. They simply focused on producing more stuff and expanding their size. They employed more people, and everyone was happy. But, all the while, they were borrowing more and more money, until eventually they collapsed under the debt load when liquidity dried up. Before Korea, the exact same thing happened in Japan, and a giant, unsustainable debt binge brought the “miracle economy” to its knees. But the Korean and Japanese debt bubbles are nothing compared to what we see in China today. Consider this: in the last five years, the Chinese created $16 TRILLION in credit that is now circulating in the economy… financing ghost cities and useless infrastructure projects. Floor space per capita in China is now 30 square meters (about 320 sq. ft.) per person. Japan was at that level in 1988. And the economy burst the following year. More astounding, this $16 trillion in credit is DOUBLE the $8 trillion in credit that China created in the previous 5,000+ years of its existence. The Chinese government recognizes it has a problem. It realizes it can no longer keep the dam from breaking. And in the past week, it bit the bullet. In the last two weeks, Chaori Solar and Haixin Steel were allowed to default, i.e. they weren’t bailed out. This is the first time in China’s modern history they’ve had a default, let alone two. They can no longer keep the game up, and the dominoes are beginning to topple. I cannot stress this enough. What we’re witnessing is a major paradigm shift. Of course, the Chinese government claims they can control the impact of these “relatively minor” corporate defaults. But as we saw during the sub-prime crisis in the Unites States, the complex web of inter-linkages in the financial system means they are playing with fire. I expect many more defaults in China in the coming weeks and months. I expect some important Chinese financial institutions to get into trouble. And I expect the Chinese government will completely lose control over the situation. My recommendations are 2-fold: 1. If you have any exposure to Chinese stocks, or the Chinese Yuan, I strongly suggest you reconsider. 2. If you have investments in iron ore or copper producers, get out. But it’s not all doom and gloom. It’s going to take time for China to suffer through this crisis. But, if the Chinese government lets the dominoes fall where they may, the country will be better off in the long term. The lessons from markets such as South Korea and Indonesia, in aftermath of the 1997-1999 Asian economic crisis, are clear. If China frees up and liberalizes its financial markets in the face of a crisis, writes off bad loans, and closes down insolvent banks, it will emerge in a much stronger position once the crisis blows over. And there will be lots of money to be made buying good-quality Chinese shares during the crisis. But, for now, it’s time to brace for the downturn. |

03-19-14 | CHINA |

||||

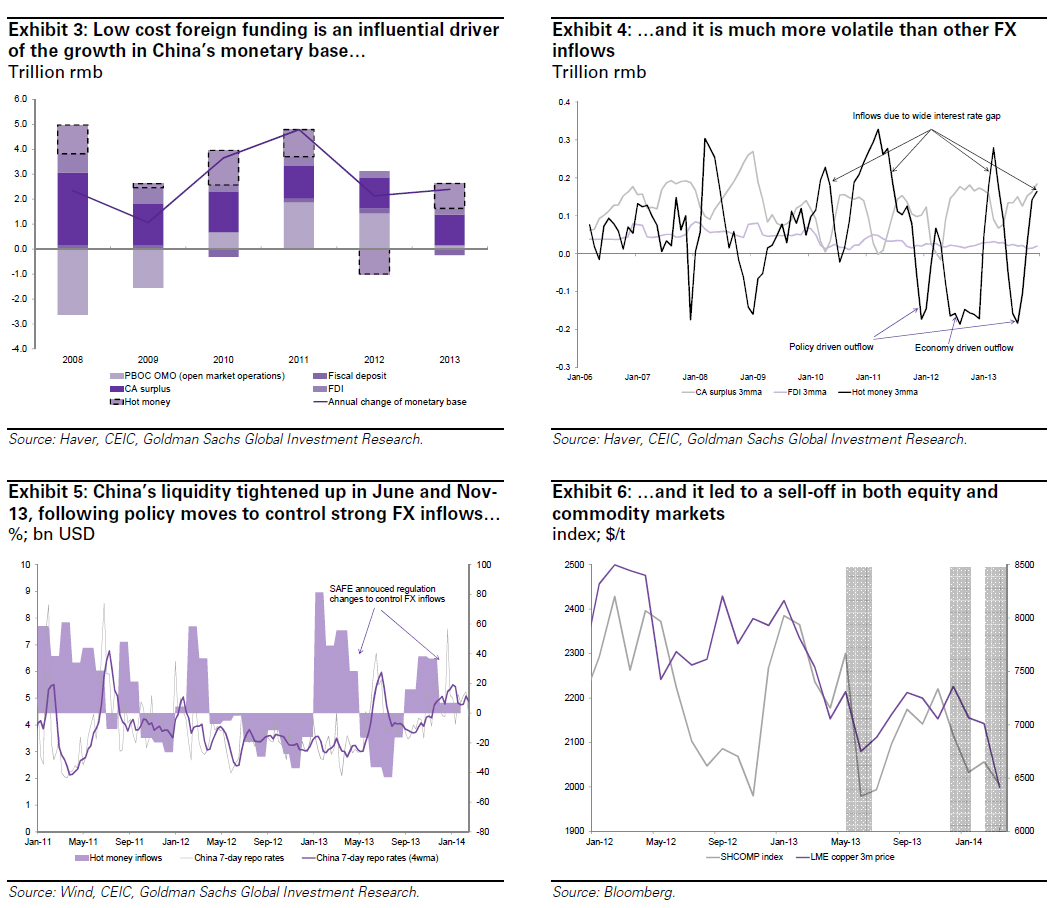

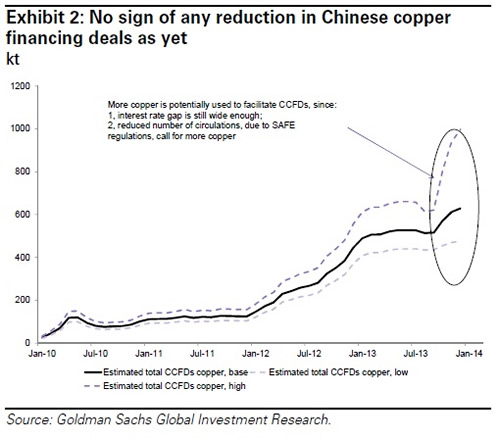

CHINESE SHADOW BANKING - CCFD (Chinese Commodity Funding Deals) What Is The Common Theme: Iron Ore, Soybeans, Palm Oil, Rubber, Zinc, Aluminum, Gold, Copper, And Nickel? 03-18-14 Goldman Sachs via ZHSo what has changed since last May, in addition to the realization that virtually every hard asset is now being used by China to mask hot money inflows into the Chinese economy taking advantage of rate differentials between the Renminbi and the Dollar? Well, this time around China may finally be serious about normalizing its epic credit bubble, which as we pointed out before, added a ridiculous $1 trillion in bank assets in just the fourth quarter of 2013 alone. Specifically, as Goldman notes in a just released analysts on the future of CCDS, "the recent managed CNY depreciation is a signal that the government wants to increase FX volatility and reduce the hot money inflow pressure gradually."

In other words, the day when the Commodity Funding Deals finally end is fast approaching.

Here is Goldman's take on what will certainly be a watershed event - one which will certainly dwarf the recent Chaori Solar default in its significance and scale. Virtually every hard asset is now being used by China to mask hot money inflows into the Chinese economy taking advantage of rate differentials between the Renminbi and the Dollar. CCFDs are ongoing and facilitating ‘hot money’ inflows into China by providing a mechanism to import low-cost foreign financing. In general, the profitability of most hedged commodity financing deals remains substantial (iron ore is the exception), due to a still positive CNY and USD interest rate differential, limited depreciation in the CNY forward curve and available commodity supply. In 2013, ‘hot money’ accounted for c. 42% of the growth in China’s monetary base of which we estimate that CCFDs contributed US$81-160 bn or c.31% of China’s total FX short-term loans. Given this, it is crucial for the government to manage the immediate impact of ‘hot money’ flow changes on the economy and markets. An increasing range of commodities are being used to raise foreign financing, which now includes iron ore, soybeans, palm oil, rubber, zinc, and aluminum, as well as gold, copper, and nickel. CCFDs create excess physical demand and tighten the physical markets artificially; in contrast, an unwind creates excess supply and thus is bearish to prices. We think CCFDs will be unwound over the medium term, mainly triggered by an increase in Chinese FX volatility, as indicated by recent CNY depreciation and PBOC’s latest move to widen the daily trading band. FX volatility could result in a higher cost of currency hedging, effectively closing the interest rate arbitrage. Higher US rates are another likely catalyst for an unwind in the long run. A continuous CNY depreciation in the short term, however, would trigger some deals to be unwound sooner than expected, and hence place downside risks to our short-term commodity price forecasts.

|

03-19-14 | CHINA SHADOW BANKING |

||||

GLOBAL GEO-POLITICS - The Collapsing Petrodollar Strategy Petrodollar Alert: Putin Prepares To Announce "Holy Grail" Gas Deal With China 03-21-14 Zero Hedge If it was the intent of the West to bring Russia and China together - one a natural resource (if "somewhat" corrupt) superpower and the other a fixed capital / labor output (if "somewhat" capital misallocating and credit bubbleicious) powerhouse - in the process marginalizing the dollar and encouraging Ruble and Renminbi bilateral trade, then things are surely "going according to plan." For now there have been no major developments as a result of the shift in the geopolitical axis that has seen global US influence, away from the Group of 7 (most insolvent nations) of course, decline precipitously in the aftermath of the bungled Syrian intervention attempt and the bloodless Russian annexation of Crimea, but that will soon change. Because while the west is focused on day to day developments in Ukraine, and how to halt Russian expansion through appeasement (hardly a winning tactic as events in the 1930s demonstrated), Russia is once again thinking 3 steps ahead... and quite a few steps east. While Europe is furiously scrambling to find alternative sources of energy should Gazprom pull the plug on natgas exports to Germany and Europe (the imminent surge in Ukraine gas prices by 40% is probably the best indication of what the outcome would be), Russia is preparing the announcement of the "Holy Grail" energy deal with none other than China, a move which would send geopolitical shockwaves around the world and bind the two nations in a commodity-backed axis. One which, as some especially on these pages, have suggested would lay the groundwork for a new joint, commodity-backed reserve currency that bypasses the dollar, something which Russia implied moments ago when its finance minister Siluanov said that Russia may regain from foreign borrowing this year. Translated: bypass western purchases of Russian debt, funded by Chinese purchases of US Treasurys, and go straight to the source. Here is what will likely happen next, as explained by Reuters:

More details on the revelation of said "Holy Grail":

Summarizing what should be and is painfully obvious to all, but apparently to the White House, which keeps prodding at Russia, is the following:

Bingo. And now add bilateral trade denominated in either Rubles or Renminbi (or gold), add Iran, Iraq, India, and soon the Saudis (China's largest foreign source of crude, whose crown prince also happened to meet president Xi Jinping last week to expand trade further) and wave goodbye to the petrodollar. As reported previoisly, China has already implicitly backed Putin without risking it relations with the West. "Last Saturday China abstained in a U.N. Security Council vote on a draft resolution declaring invalid the referendum in which Crimea went on to back union with Russia. Although China is nervous about referendums in restive regions of other countries which might serve as a precedent for Tibet and Taiwan, it has refused to criticize Moscow. The support of Beijing is vital for Putin. Not only is China a fellow permanent member of the U.N. Security Council with whom Russia thinks alike, it is also the world's second biggest economy and it opposes the spread of Western-style democracy." This culminated yesterday, when as we reported last night, Putin thanked China for its "understanding over Ukraine." China hasn't exactly kept its feelings about closer relations with Russia under wraps either:

The punchline: "A strong alliance would suit both countries as a counterbalance to the United States." An alliance that would merely be an extension of current trends in close bilateral relations, including not only infrastructure investment but also military supplies:

And as if pushing Russia into the warm embrace of the world's most populous nation was not enough, there is also the second most populated country in the world, India.

To summarize: while the biggest geopolitical tectonic shift since the cold war accelerates with the inevitable firming of the "Asian axis", the west monetizes its debt, revels in the paper wealth created from an all time high manipulated stock market while at the same time trying to explain why 6.5% unemployment is really indicative of a weak economy, blames the weather for every disappointing economic data point, and every single person is transfixed with finding a missing airplane

|

03-2214 | GLOBAL GEO-POL PETRODOLLAR |

8 - Geo-Political Event | |||

UKRAINE - A Financial Battlefield RATIONALE: RUSSIAN ARGUMENTS

RATIONALE: US / EU / UK / JAPAN / CANADA ARGUMENTS

FINANCIAL WARFARE

|

01-19-14 | UKRAINE | 8 - Geo-Political Event | |||

UKRAINE CONFLICT - Russian Economic & Sanctions

With The White House proclaiming Russian stocks a "sell" today (and in the meantime Russian stocks and the Ruble strengthening), it is clear, as Citi's Steven Englander notes, that the Russia/Ukraine crisis may be the first major political conflict that is played out in international financial markets. The difference, Englander points out, between this and standard imposition of sanctions is that both sides have some options that can inflict damage on the other side. International finance as a continuation of war by other means (via Citi's Steven Englander) Normally sanctions involve a big group of countries on one side and a vulnerable target on the other so the vulnerability is very asymmetric. Small countries can occasionally expropriate big country assets but in most cases that ostracizes the small country from the international financial community. The US/EU are hoping that they can make the crisis sufficiently painful to Russia that it backs off from the Ukraine. The Russians may suspect that the willingness in the West to pay a financial/economic price is limited and that public opinion will swing quickly if volatility emerges. So far we have:

There are even reports that there were efforts by Russia in 2008 to exacerbate the US financial crisis, although the reports do not have firsthand documentation. Other countries may be watching this as a template for how events would play out in case Asian political issues over conflicting territorial claims or other issues escalate. These developments may give a different meaning to the term ‘currency wars’ that became so popular in recent years. One advantage using finance as a weapon is that it can be scaled up or down as needed, and is much more reversible than military actions. It is also quicker than traditional trade sanctions to have an impact, and arguably is more likely to hit decision-makers and those who have access to them than trade sanctions, which often hit the poor and almost always create profit-making opportunities for the well-connected in sanctions-running. How far can this go and what are the implications? So far the steps taken are baby steps – sanctions applied to a handful of Russians and Crimeans by the US and EU, but no real screws being applied (Russian President Putin not named, for example). Probably there are huge holes through which transactions can continue to occur and the sanctions can be evaded. However, if the crisis intensifies, the US/EU may be tempted to apply broader sanctions on Russian assets on the view that this is the quickest way to apply pressure and that Russians will be unable or unwilling to move their assets into friendly jurisdictions quickly enough. For the Russians, the temptation may be to try and sell USD assets in order to disrupt US asset markets, but the leverage may be temporary. Their reserves are almost USD470bn but they have been actively diversifying away from USD for years. Relative to the size of any market they might be tempted to disrupt, the USD holdings are small. Moreover the sense that the price was being driven down by politically-motivated selling would likely attract buyers on the view that the effects would be limited. Were they do convince other countries to join them, the impact would be more longer lasting and more disruptive, but it is a little bit like letting your own home run down because it will lower the property value of a neighbor you dislike. The damage you do to yourself is more than you can expect to do to your neighbor. The Russian holdings of USD are probably enough to give the USD a big whack, were they to go into the market selling, especially as since there may be selling pressures already from other reserve managers, and given the trend-loving nature of currency investors. Once you get past hurt feelings, it is not clear that USD weakness would be a US economic or financial market negative. A strong dollar is hardly a US policy priority, to the extent that USD weakness would crowd in both exports and imported inflation, it would probably be viewed as going in the direction preferred by Fed policymakers. Were it not for the unfriendly motivation, it is unlikely that US policymakers would object. Long-term implications If the use of financial market warfare intensifies, the risks are:

This would unwind many years of international capital market liberalization. Moreover, it would have the greatest impact in discouraging long-term, illiquid investments, as these would be most vulnerable to seizure. It is much easier to cut positions in short term liquid assets if there is trouble brewing. External deficit EM economies would probably suffer the most since creditors would see an extra force majeure risk premium added. Apolitical safe havens would probably benefit the most. Where there is an interaction with the traditional currency war discussion is that the damage to EM borrowers would probably be greater than to G10 borrowers. When EM countries depreciate, they often get hit by higher bond yields as well. G10 countries, even when they depreciate sharply, often do not face big pressures on their bond markets. Moreover, higher food prices from depreciation are not nearly the same social issue in G10 that they are in EM |

01-18-14 | UKRAINE | 8 - Geo-Political Event | |||

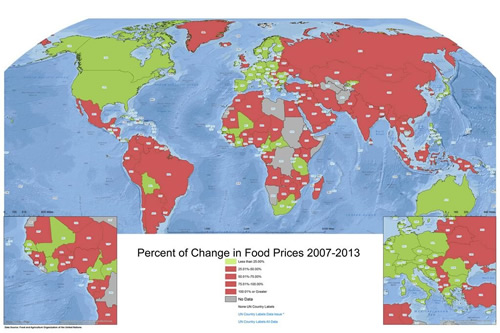

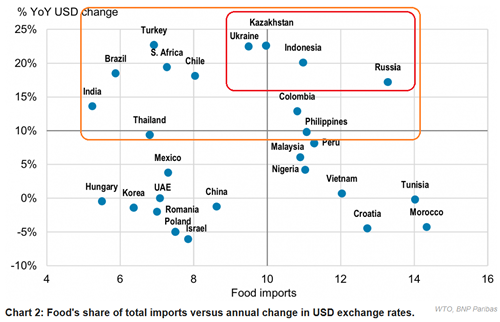

FOOD INFATION - Its Initially Going to Be A Retail CRE and EM Problem There is a Correlation Between Food Price Inflation & Social Unrest

The Ukrainean Breadbasket Has Food Price Pressures

Things Could Potentially Get Worse |

03-18-14 | GLOBAL RISK FOOD |

27 - Food Price Pressures | |||

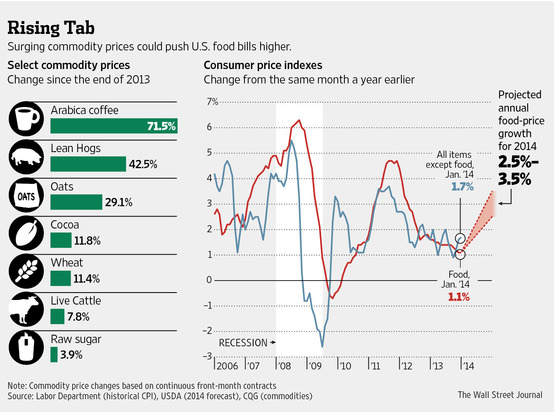

FOOD INFATION - Its Initially Going to Be A Retail CRE and EM Problem Food Prices Surge as Drought Exacts a High Toll on Crops 03-17-14 WSJ Costs Pinch Consumers, Companies Still Grappling With Sluggish Economic Recovery

Surging prices for food staples from coffee to meat to vegetables are driving up the cost of groceries in the U.S., pinching consumers and companies that are still grappling with a sluggish economic recovery. Federal forecasters estimate retail food prices will rise as much as 3.5% this year, the biggest annual increase in three years, as drought in parts of the U.S. and other producing regions drives up prices for many agricultural goods. Globally, food inflation has been tame, but economists are watching for any signs of tighter supplies of key commodities such as wheat and rice that could push prices higher. In the U.S., much of the rise in the food cost comes from higher meat and dairy prices, due in part to tight cattle supplies after years of drought in states such as Texas and California and rising milk demand from fast-growing Asian countries. But prices also are higher for fruits, vegetables, sugar and beverages, according to government data. In futures markets, coffee prices have soared so far this year more than 70%, hogs are up 42% on disease concerns and cocoa has climbed 12% on rising demand, particularly from emerging markets. Drought in Brazil, the world's largest producer of coffee, sugar and oranges, has increased coffee prices, while dry weather in Southeast Asia has boosted prices for cooking oils such as palm oil.

Though rising, U.S. food inflation isn't yet near some lofty recent levels. In 2008, food prices jumped 5.5%, the most in 18 years, and they climbed 3.7% in 2011. Inflation also could be tempered if U.S. farmers, as expected, plant large corn and soybean crops this spring and receive favorable weather during the summer. That would hold down feed prices for livestock and poultry, as well as ingredient costs for breakfast cereals and baked goods. The U.S. Department of Agriculture estimated last month that retail food prices will rise between 2.5% and 3.5% this year, up from 1.4% last year. The inflation comes despite sharp decreases over the past year in the prices of grains, including corn, after a big U.S. harvest. In other years—notably 2008—surging grain prices were a key contributor to higher food costs. Food prices have gained 2.8%, on average, for the past 10 years, outpacing the increase in prices for all goods, which rose 2.4%, according to the government. Overall consumer prices are expected to rise 1.9% this year, according to economists surveyed by The Wall Street Journal. RETAIL PRESSURES Still, the price increases pose a challenge for food makers, restaurants and retailers, which must decide how much of the costs they can pass along and still retain customers at a time of intense competition and thin profit margins. During previous inflationary periods, food makers switched to less-expensive ingredients or reduced package sizes to maintain their profit margins. Retailers and restaurants usually raise prices as a last resort.

One reason prices are higher now is the lingering effect from the historic 2012 U.S. drought, which sent animal-feed prices surging to record highs and caused livestock and dairy farmers to cull herds, analysts said. In California, the biggest U.S. producer of agricultural products, about 95% of the state is suffering from drought conditions, according to data from the U.S. Drought Monitor. This has led to water shortages that are hampering crop and livestock production. U.S. fresh-vegetable prices that jumped 4.7% last year are forecast to rise as much as 3% this year, while fruit that gained 2% last year will rise up to 3.5% in 2014, according to the USDA. Dry weather in Brazil has contributed to a dramatic increase this year in prices for arabica coffee, the world's most widely produced variety. Arabica-coffee futures, which were at a seven-year low last year, settled at a two-year high of $2.0505 a pound on March 13. In each of the past two years, global food prices on average declined from the previous year, as farmers ramped up production of wheat, sugar and other commodities, according to the United Nations Food and Agriculture Organization, which publishes a monthly food-price index. But that index rose 5.2 points to 208.1 last month compared with January, the sharpest jump since mid-2012. EMERGING MARKETS Food-price increases are a particularly touchy issue for emerging markets, where spending on food accounts for a higher share of monthly budgets than in wealthier countries. In 2008, a spike in food prices caused riots from Haiti to sub-Saharan Africa and South Asia. Three years later, in 2011, rising food prices were a factor behind the Arab Spring protests in North Africa and the Middle East that ultimately toppled governments in Tunisia and Egypt. The increase in global prices last month surprised some economists, and raised the specter of more severe increases that could hit the world's poorest countries, economists said.

"To be honest, until a month ago, our feeling and thinking was that most markets were well-supplied," said John Baffes, a senior economist at the World Bank. "Now, the question is: Are those adverse weather conditions going to get worse? If they do, then indeed, we may see more food price increases. |

03-18-14 | GLOBAL RISK FOOD |

27 - Food Price Pressures | |||

| TO TOP | ||||||

| MACRO News Items of Importance - This Week | ||||||

GLOBAL MACRO REPORTS & ANALYSIS |

||||||

US ECONOMIC REPORTS & ANALYSIS |

||||||

| CENTRAL BANKING MONETARY POLICIES, ACTIONS & ACTIVITIES | ||||||

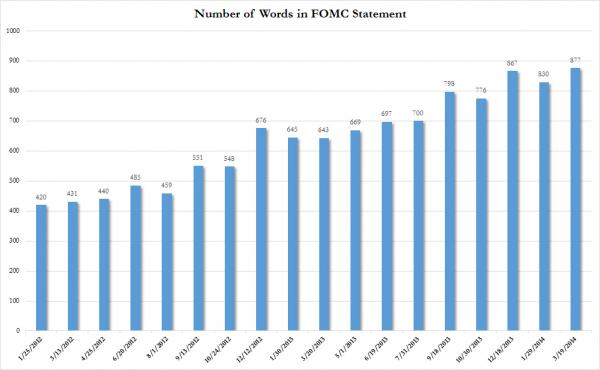

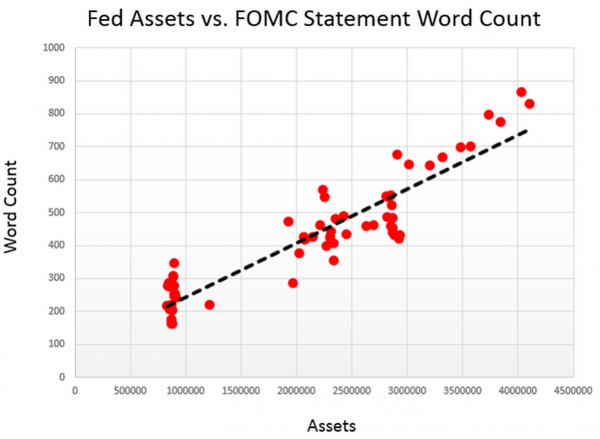

FOMC MEETING - A "Slip" and a "Pattern" Why disastrous? Here is the statement that sent stocks reeling:

The major market moving 'slip' HIGHLIGHT POINTS

The Wall Street Journal's Jon Hilsenrath clarifies

FINANCIAL MARKETS

KEY PATTERN DEMONSTRATED The S&P 500 tracked AUDJPY through all the excitement

877 words in the FOMC statement, which is an all time record It is needed to justify this

|

03-20-14 | US MONETARY | CENTRAL BANKS |

|||

| Market | ||||||

| TECHNICALS & MARKET |

|

|||||

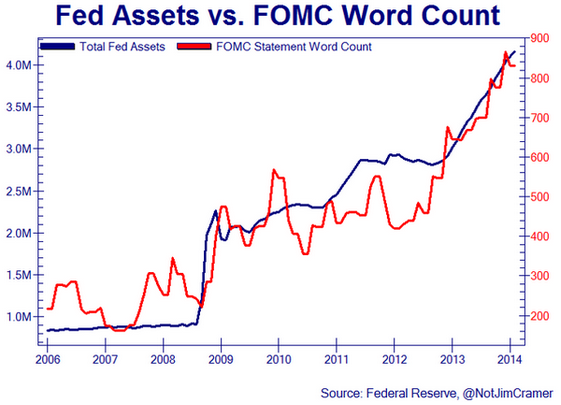

PATTERNS - Beware When the Fed's Asset Quarterly (13 Wk) ROC Goes Negative FLOWS: Its the 2nd Derivative

|

03-17-14 | FLOWS | ||||

| COMMODITY CORNER - HARD ASSETS | PORTFOLIO | |||||

| COMMODITY CORNER - AGRI-COMPLEX | PORTFOLIO | |||||

| SECURITY-SURVEILANCE COMPLEX | PORTFOLIO | |||||

| THESIS | ||||||

| 2014 - GLOBALIZATION TRAP | 2014 |  |

||||

|

||||||

|

2013 2014 |

|

|||||

2011 2012 2013 2014 |

|

|||||

| THEMES | ||||||

| FLOWS -FRIDAY FLOWS | THEME |  |

||||

FLOWS - Credit, Liquidity and Debt

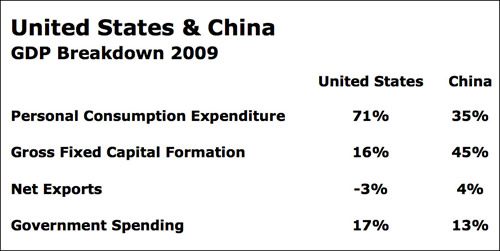

The China Crisis Richard Duncan China's economy is tipping into crisis because its economic growth model of export-led, investment-driven growth has taken China as far as it can. In a global economy that is barely growing, there is no one left for China to export more to. The end of the Great China Boom will have a profound impact on every corner of the globe. Here's what's happening. In the past, very rapid credit growth in the United States fuelled the US economy and pulled in sharply increasing amounts of imports each year. Surging US demand created a bonanza for the global economy as the rest of the world expanded its investment and industrial production to satisfy orders from the United States. No country benefited more than China.

With exports and investment booming, China's economic growth exploded. The size of its GDP grew from $350 billion in 1990 to $8.2 trillion in 2012. And, as China's economy grew, it pulled in huge amounts of imports from around the world - raw materials from Australia, South-East Asia, Africa and South America; oil from the Middle-East and Russia; and advanced machinery from Germany and Japan. China became the world's second engine of growth. China's economy was peculiarly lopsided, however. Investment amounted to 49% of GDP in 2011, whereas household consumption amounted to only 35% of GDP. That is twice the world average for investment and less than half the global average for consumption.

This imbalance between investment and consumption illustrates how dependent China's economy is on demand from the rest of the world. Export-led, investment-driven growth worked miracles for China for three decades. But the conditions that existed between, say, 1985 and 2007, are no longer in place today. During those years, total debt in the United States increased from $9 trillion to $50 trillion; and the ratio of total debt to GDP rose from 150% to 370%. Today, the growth of total debt in the US is less than 2% a year (adjusted for inflation). That is too little to generate meaningful economic growth there. Consequently, imports into the US are depressed. Goods imported were flat in 2013 relative to 2012. Therefore, the growth in world trade is weak and the global economy is verging on recession. In this environment, it is not possible for China to continue growing its exports at a double-digit annual pace. During the first two months of this year, China's exports actually contracted by 1.6% compared with the first two months of last year. China has responded to the crisis in global growth by investing more in domestic infrastructure and by radically expanding domestic credit. Bank loans have increased by 135% since the crisis began and lending by the shadow banking system has grown even more rapidly. However, there is a limit as to how many highways and bridges that China can build. Moreover, the longer the credit binge continues the greater the probability of a systemic banking crisis becomes. With global demand for Chinese exports saturated, any further investment in factories will only result in losses since China already has enormous excess industrial capacity across almost every industry. To put it mildly, China is in trouble. And that spells trouble for the rest of the world. As a result,

The scenario outlined above is more likely to play out gradually rather than overnight. China still has a great deal of scope to stimulate its economy by running very large budget deficits the way Japan has done for the last 24 years. Moreover, in all probability, the Fed and other central banks would respond to this risk of global recession by significantly increasing the amount of fiat money they print each month. Therefore, while I don't expect the crisis in China's economic growth model to produce an immediate crisis in the global economy, I do believe that it will create very significant headwinds for the rest of the world during the years immediately ahead. This is another reason why Quantitative Easing is unlikely to end any time soon.

|

03-21-14 | FLOWS CHINA |

||||

| SHADOW BANKING -LIQUIDITY / CREDIT ENGINE | THEME | |||||

| CRACKUP BOOM - ASSET BUBBLE | THEME | |||||

| ECHO BOOM - PERIPHERAL PROBLEM | THEME | |||||

| PRODUCTIVITY PARADOX -NATURE OF WORK | THEME | |||||

| STANDARD OF LIVING -EMPLOYMENT CRISIS | THEME | |||||

| CORPORATOCRACY -CRONY CAPITALSIM | THEME |  |

||||

CORRUPTION & MALFEASANCE -MORAL DECAY - DESPERATION, SHORTAGES. |

THEME |  |

||||

| SOCIAL UNREST -INEQUALITY & A BROKEN SOCIAL CONTRACT | THEME | |||||

| SECURITY-SURVEILLANCE COMPLEX -STATISM | THEME | |||||

| GLOBAL FINANCIAL IMBALANCE - FRAGILITY, COMPLEXITY & INSTABILITY | THEME | |||||

| CENTRAL PLANINNG -SHIFTING ECONOMIC POWER | THEME | |||||

| CATALYSTS -FEAR & GREED | THEME | |||||

| GENERAL INTEREST |

|

|||||

| TO TOP | ||||||

Ongoing massive investment in infrastructure is increasingly wasteful. And, the wild lending spree underway is increasingly destabilizing.

Ongoing massive investment in infrastructure is increasingly wasteful. And, the wild lending spree underway is increasingly destabilizing.

Tipping Points Life Cycle - Explained

Click on image to enlarge

{kind=link}

{kind=link}

{kind=link}

{kind=link}

TO TOP

|

YOUR SOURCE FOR THE LATEST THINKING & RESEARCH

|

�

TO TOP