|

JOHN RUBINO'SLATEST BOOK |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

"MELT-UP MONITOR "

Meltup Monitor: FLOWS - The Currency Cartel Carry Cycle - 09 Dec 2013 Meltup Monitor: FLOWS - Liquidity, Credit & Debt - 04 Dec 2013 Meltup Monitor: Euro Pressure Going Critical - 28- Nov 2013 Meltup Monitor: A Regression-to-the-Exponential Mean Required - 25 Nov 2013

|

![]()

"DOW 20,000 "

Lance Roberts Charles Hugh Smith John Rubino Bert Dohman & Ty Andros

|

HELD OVER

Currency Wars

Euro Experiment

Sultans of Swap

Extend & Pretend

Preserve & Protect

Innovation

Showings Below

"Currency Wars "

|

"SULTANS OF SWAP" archives open ACT II ACT III

ALSO Sultans of Swap: Fearing the Gearing! Sultans of Swap: BP Potentially More Devistating than Lehman! |

"EURO EXPERIMENT"

archives open EURO EXPERIMENT : ECB's LTRO Won't Stop Collateral Contagion!

EURO EXPERIMENT: |

![]()

"INNOVATION"

archives open |

"PRESERVE & PROTE CT"

archives open |

Weekend Jan. 24th, 2015

Follow Our Updates

on TWITTER

https://twitter.com/GordonTLong

AND FOR EVEN MORE TWITTER COVERAGE

STRATEGIC MACRO INVESTMENT INSIGHTS

2014 THESIS: GLOBALIZATION TRAP

2014 THESIS: GLOBALIZATION TRAP

NOW AVAILABLE FREE to Trial Subscribers

185 Pages

What Are Tipping Poinits?

Understanding Abstraction & Synthesis

Global-Macro in Images: Understanding the Conclusions

![]()

| JANIUARY | ||||||

| S | M | T | W | T | F | S |

| 1 | 2 | 3 | ||||

| 4 | 5 | 6 | 7 | 8 | 9 | 10 |

| 11 | 12 | 13 | 14 | 15 | 16 | 17 |

| 18 | 19 | 20 | 21 | 22 | 23 | 24 |

| 25 | 262 | 27 | 28 | 29 | 30 | 30 |

KEY TO TIPPING POINTS |

| 1 - Risk Reversal |

| 2 - Japan Debt Deflation Spiral |

| 3- Bond Bubble |

| 4- EU Banking Crisis |

| 5- Sovereign Debt Crisis |

| 6 - China Hard Landing |

| 7 - Chronic Unemployment |

| 8 - Geo-Political Event |

| 9 - Global Governance Failure |

| 10 - Chronic Global Fiscal ImBalances |

| 11 - Shrinking Revenue Growth Rate |

| 12 - Iran Nuclear Threat |

| 13 - Growing Social Unrest |

| 14 - US Banking Crisis II |

| 15 - Residential Real Estate - Phase II |

| 16 - Commercial Real Estate |

| 17 - Credit Contraction II |

| 18- State & Local Government |

| 19 - US Stock Market Valuations |

| 20 - Slowing Retail & Consumer Sales |

| 21 - China - Japan Regional Conflict |

| 22 - Public Sentiment & Confidence |

| 23 - US Reserve Currency |

| 24 - Central & Eastern Europe |

| 25 - Oil Price Pressures |

| 26 - Rising Inflation Pressures & Interest Pressures |

| 27 - Food Price Pressures |

| 28 - Global Output Gap |

| 29 - Corruption |

| 30 - Pension - Entitlement Crisis |

| 31 - Corporate Bankruptcies |

| 32- Finance & Insurance Balance Sheet Write-Offs |

| 33 - Resource Shortage |

| 34 - US Reserve Currency |

| 35- Government Backstop Insurance |

| 36 - US Dollar Weakness |

| 37 - Cyber Attack or Complexity Failure |

| 38 - Terrorist Event |

| 39 - Financial Crisis Programs Expiration |

| 40 - Natural Physical Disaster |

| 41 - Pandemic / Epidemic |

Reading the right books?

No Time?

We have analyzed & included

these in our latest research papers Macro videos!

![]()

OUR MACRO ANALYTIC

CO-HOSTS

John Rubino's Just Released Book

![]()

Charles Hugh Smith's Latest Books

![]()

![]()

Our Macro Watch Partner

Richard Duncan Latest Books

MACRO ANALYTIC

GUESTS

F William Engdahl

![]()

![]()

![]()

![]()

![]()

OTHERS OF NOTE

![]()

![]()

![]()

![]()

Book Review- Five Thumbs Up

for Steve Greenhut's

Plunder!

![]()

TODAY'S TIPPING POINTS

|

Scroll TWEETS for LATEST Analysis

Read More - OUR RESEARCH - Articles Below

HOTTEST TIPPING POINTS |

Theme Groupings |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Investing in Macro Tipping Points

THESE ARE NOT RECOMMENDATIONS - THEY ARE MACRO COMMENTARY ONLY - Investments of any kind involve risk. Please read our complete risk disclaimer and terms of use below by clicking HERE |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

We post throughout the day as we do our Investment Research for: LONGWave - UnderTheLens - Macro |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

"BEST OF THE WEEK "

|

Posting Date |

Labels & Tags | TIPPING POINT or THEME / THESIS or INVESTMENT INSIGHT |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

MOST CRITICAL TIPPING POINT ARTICLES TODAY

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| THESIS & THEMES | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

US DOLLAR - Beggar-thy-Neighbor The $9 Trillion US Dollar Carry Trade is Blowing Up 01-23-15 Phoenix Capital Research The US Dollar rally, combined with the ECB’s policies are at risk of blowing up a $9 trillion carry trade. When the Fed cut interest rates to zero in 2008, it flooded the system with US Dollars. The US Dollar is the reserve currency of the world. NO matter what country you’re in (with few exceptions) you can borrow in US Dollars. And if you can borrow in US Dollars at 0.25%... and put that money into anything yielding more… you could make a killing. A hedge fund in Hong Kong could borrow $100 million, pay just $250,000 in interest and plow that money into Brazilian Reals which yielded 11%... locking in a $9.75 million return. This was the strictly financial side of things. On the economics side, Governments both sovereign and local borrowed in US Dollars around the globe to fund various infrastructure and municipal projects. Simply put, the US Government was practically giving money away and the world took notice, borrowing Dollars at a record pace. Today, the global carry trade (meaning money borrowed in US Dollars and invested in other assets) stands at over $9 TRILLION (larger than the economy of France and Brazil combined). This worked while the US Dollar was holding steady. But in the summer of last year (2014), the US Dollar began to breakout of a multi-year wedge pattern:

Why does this matter? Because the minute the US Dollar began to rally aggressively, the global US Dollar carry trade began to blow up. It is not coincidental that oil commodities, and emerging market stocks took a dive almost immediately after this process began.

This process is not over, not by a long shot. As anyone who invested during the Peso crisis or Asian crisis can tell you, when carry trades blow up, the volatility can be EXTREME. The market drop in October was just the start. Once the US Dollar rally really begins picking up steam, we could very well see a crash. |

01-24-15 | US DOLLAR |

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| MOST CRITICAL TIPPING POINT ARTICLES THIS WEEK - Jan 18th, 2014 - Jan 24th, 2014 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| RISK REVERSAL | 1 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| JAPAN - DEBT DEFLATION | 2 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| BOND BUBBLE | 3 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

BOND BUBBLE - Falling Earnings The Beginning of the End of the $100 TRILLION Bond Bubble 01-19-15 Phoenix Capital Research's blog The big story in the world is the bond bubble. ENTITLEMENTS - "The Spending of Other Peoples Money" For over 30 years, sovereign nations, particularly in the West have been buying votes by offering social payments in the form of welfare, Medicare, social security, and the like. The ridiculousness of this should not be lost on anyone. Politicians, in order to be elected, promise to allocate taxpayer funds on social programs that will benefit said taxpayers down the road (we’re simply talking about social spending, not infrastructure or other costs. The concept that taxpayers might simply just keep the money to begin with never enters the equation. And because everyone believes that they are somehow spending someone else’s money, they play along. When you believe that you are spending someone else’s money, it’s very easy to write a blank check, which is precisely what Western nations have been doing for years, promising everyone a safe and secure retirement without ever bothering to see where the money would come from. When actual bills came due to fund this stuff, Governments quickly discovered that current tax revenues couldn’t cover it… so they issued sovereign debt to make up the difference. SOVEREIGN DEBT & BANKING And so the bond bubble was created. The large banks, that have a monopoly on managing sovereign debt auctions, were only too happy to play along with this. The reasons are as follows:

Since it was rarely if ever a problem to issue sovereign debt, Governments kept promising future payments that they didn’t have until we reach today: the point at which most Western nations are sporting Debt to GDP ratios well north of 300% when you consider unfunded liabilities (the social spending programs mentioned earlier). Now, cutting social spending is usually considered political suicide (after all, the voters put you in office in the first place based on you promising to pay them welfare payments down the road). So rather than default on the social contract made with voters, the political class will simply push to issue MORE debt to finance old debt that is coming due. The US did precisely this in the fourth quarter of 2014, issuing over $1 trillion in new debt simply to pay back old debt that was coming due. BOND BUBBLE - In the 8th Inning This is how the bond market becomes a bubble. Between 2000 and today, the global bond market has nearly TRIPLED in size. Today, it’s north of $100 trillion in size. And it’s backstopping over $555 trillion in derivatives trades. There is literally no easy fix to any of this. The pain will be severe. And so everyone in charge of the important decisions (the political elite, the big banks, and the Central Banks) will push this as far as it can possibly go before taking the inevitable hit. The fact that Central banks are now openly cutting interest rates to NEGATIVE should tell you how far along we are in terms of funding problems (at these rates, bond holders are PAYING the Government for the right to own bonds). From a baseball analogy we’re in the late 8th, possibly early 9th inning. When the game ends, the entire mess will collapse. And it will make 2008 look like a joke.

|

01-22-15 | GLOBAL RISK MACRO MONETARY US FISCAL |

3- Bond Bubble | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

EU BANKING CRISIS |

4 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| SOVEREIGN DEBT CRISIS [Euope Crisis Tracker] | 5 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

CHINA BUBBLE |

6 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

GROWTH - Shrinking Growth Rates

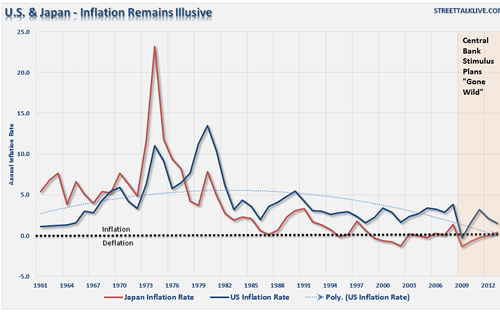

Deflation Is A Problem For The Fed 01-20-15 Lance Roberts The biggest worry of the Federal Reserve, and frankly every Central Banker on the planet, is deflation. The reason is that deflation, as an economic pressure, is dangerous and once entrenched becomes difficult to break. For the Fed, the fear of inflation is far less worrisome. Conventional monetary policy tools, mainly interest rates, can be used to some degree of success to stymie inflationary pressures. The problem is that such actions, as shown below, have ALWAYS led to an economic recession or negative financial consequence.

However, as can be witnessed in both Japan and the U.S., Central Bank monetary policy tools have little effect in reversing deflationary pressures.

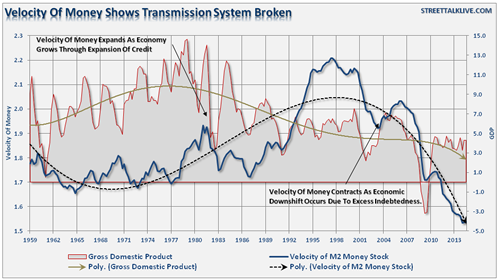

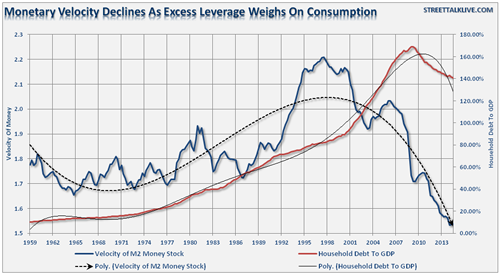

For several years, there have been repetitive screams that inflation was imminent due to deficits, a fiat currency and expanding debt levels. Yet, the opposite has been true. The lack of inflation has been a construct of the underlying structural dynamics of the economy. Home ownership rates have plunged, technological advances and productivity increases have fostered wage suppression, and high levels of uncounted unemployed (54% of the 16-54 aged labor force) drag on economic strength. The exceptionally low yields on government treasuries is clear evidence that inflation is not a threat. For all the money that has been spent trying to ignite the engine of economic growth; it has all remained a futile effort at this point. Velocity Of Money The velocity of money is defined by Wikipedia as:

As the velocity of money accelerates, demand rises and inflationary pressures increase. However, as you can clearly see, the demand for money has been on the decline since the turn of the century.

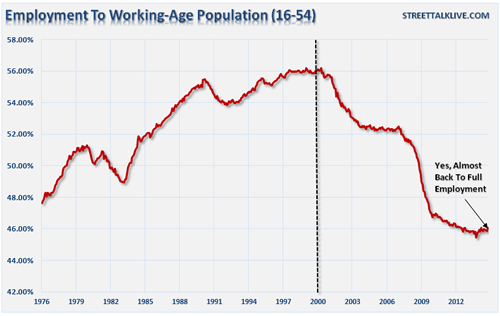

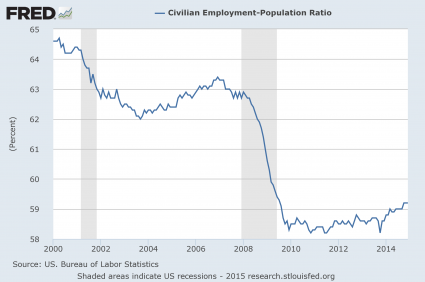

Employment Even with all the financial stimulation from bailouts, to QE programs, tax incentives and credits, etc., the velocity of money has waned since the end of the last recession as the economy has sputtered along at sub-par growth rates. Of course, much of that can be attributed to sustained levels of high unemployment which has suppressed both wage growth and aggregate end demand which in turn has kept businesses on the defensive. As discussed previously, the most important segment of the labor force(those between the ages of 16-54) remain largely unemployed.

Wages Wages are a critical weapon in defeating deflation. Wages have remained not only in a long term downtrend but have also lagged the pace of inflation over time. The median wage level today in the U.S., had it kept pace with inflation, should be closer to $90,000 annually versus $50,000 today. This suppression of wages due to rising productivity levels, and now a large and available labor pool, contributes to the lack of aggregate end demand. The deflationary pressures of declining wage growth remain a major level of concern as the disparity between rich and poor continues to growth. The chart below,from my friend Doug Short, shows the income problem. The problem with wage deflation for the Fed is that in order for wage growth to occur, the economy really does need to begin to approach "real" full employment. As the supply of labor shrinks, the demand for increases in wages can occur. The problem is that with uncounted masses of individuals residing in the shadows, the demand for labor is swamped by the demand for jobs. This keeps wages suppressed. The issue for the Fed is that the decline in the "unemployment rate," caused by a shrinking labor force, is potentially obfuscating the difference between a "real" and a"statistical" full employment level. While it is expected that millions of individuals will retire in the coming years ahead; the reality is that many of those "potential" retirees will continue to work throughout their retirement which will inflate the labor pool and keep a lid on future wage growth. The Fed's repetitive "QE" programs were aimed at the very heart of the deflationary problem. The Fed was convinced that by stimulating a "wealth effect," the consumer would begin increasing consumption which would then spiral demand out into the economy. While the Fed certainly inflated asset prices higher, it has done little to translate across the broad economy. As I discussed in "For 90% There Has Been No Recovery:"

While the Fed's efforts created a short term wealth effect in the stock market, the excess reserves created by the QE programs remained bottled up at the banks rather than flowing through the system. Before the 2008 financial crisis, excess bank reserves remained constant going back to 1980 averaging just $18.9 billion. Today, those excess reserves are near record levels $2.75 Trillion. The threat of a deflation, more than six years after the last recession, remains an imminent threat. It is not just a domestic issue, but a global one. The Eurozone, Japan, and even China are all wrestling with slowing economic expansion despite success rounds of interventions. The continued hope, of course, is that the next round of interventions will be the one that finally sparks the inflationary pressures needed to jump start the engine of economic recovery. Unfortunately, that has yet to be the case, and the rate of diminishing returns from each program continue to increase. The collapse in commodity prices, interest rates and the surge in dollar are all clear signs that money is seeking "safety" over "risk." Maybe you should be asking yourself what it is that they know that you don't? The answer could be extremely important.

|

01-23-15 |

MACRO MONETARY US MONETARY |

11 - Shrinking Revenue Growth Rate | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| TO TOP | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| MACRO News Items of Importance - This Week | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

GLOBAL MACRO REPORTS & ANALYSIS |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

US ECONOMIC REPORTS & ANALYSIS |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

US STANDARD OF LIVING - A 'Shadow" State of the Union A SHADOW STATE OF THE UNION Please use the following scorecard during the State of the Union to see what is mentioned, what is not and what is being done about any on the list of 27 items below.

A product of the Chicago Cook Country political apparatus It is our studied opinion that anything discussed will have almost no signficance to the American people once all the spin, happy-talk and platitudes are stripped away!

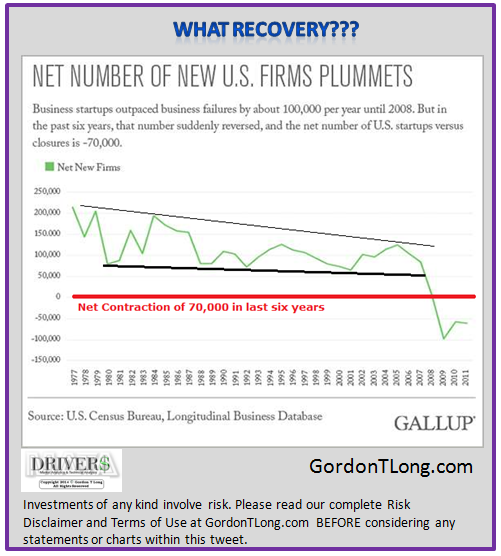

27 Facts That Show How The Middle Class Has Fared Under 6 Years Of Barack Obama 01-18-15 Michael Snyder - The Economic Collapse blog, During his State of the Union speech on Tuesday evening, Barack Obama is going to promise to make life better for middle class families. Of course he has also promised to do this during all of his other State of the Union addresses, but apparently he still believes that there are people out there that are buying what he is selling. Each January, he gets up there and tells us how the economy is “turning around” and to believe that much brighter days are right around the corner. And yet things just continue to get even worse for the middle class. The numbers that you are about to see will not be included in Obama’s State of the Union speech. They don’t fit the “narrative” that Obama is trying to sell to the American people. But all of these statistics are accurate. They paint a picture of a middle class that is dying. Yes, the decline of the U.S. middle class is a phenomenon that has been playing out for decades. But without a doubt, our troubles have accelerated during the Obama years. When it comes to economics, he is completely and utterly clueless, and the policies that he has implemented are eating away at the foundations of our economy like a cancer. The following are 27 facts that show how the middle class has fared under 6 years of Barack Obama… #1 American families in the middle 20 percent of the income scale now earn less money than they did on the day when Barack Obama first entered the White House. #2 American families in the middle 20 percent of the income scale have a lower net worth than they did on the day when Barack Obama first entered the White House. #3 According to a Washington Post article published just a few days ago, more than 50 percent of the children in U.S. public schools now come from low income homes. This is the first time that this has happened in at least 50 years. #4 According to a Census Bureau report that was recently released, 65 percent of all children in the United States are living in a home that receives some form of aid from the federal government. #5 In 2008, the total number of business closures exceeded the total number of businesses being created for the first time ever, and that has continued to happen every single year since then. #6 In 2008, 53 percent of all Americans considered themselves to be “middle class”. But by 2014, only 44 percent of all Americans still considered themselves to be “middle class”. #7 In 2008, 25 percent of all Americans in the 18 to 29-year-old age bracket considered themselves to be “lower class”. But in 2014, an astounding 49 percent of all Americans in that age range considered themselves to be “lower class”. #8 Traditionally, owning a home has been one of the key indicators that you belong to the middle class. So what does the fact that the rate of homeownership in America has been falling for seven years in a row say about the Obama years? #9 According to a survey that was conducted last year, 52 percent of all Americans cannot even afford the house that they are living in right now. #10 After accounting for inflation, median household income in the United States is 8 percent lower than it was when the last recession started in 2007. #11 According to one recent survey, 62 percent of all Americans are currently living paycheck to paycheck. #12 At this point, one out of every three adults in the United States has an unpaid debt that is “in collections“. #13 When Barack Obama first set foot in the Oval Office, 60.6 percent of all working age Americans had a job. Today, that number is sitting at only 59.2 percent…

#14 While Barack Obama has been in the White House, the average duration of unemployment in the United States has risen from 19.8 weeks to 32.8 weeks. #15 It is hard to believe, but an astounding 53 percent of all American workers make less than $30,000 a year. #16 At the end of Barack Obama’s first year in office, our yearly trade deficit with China was 226 billion dollars. Last year, it was more than 314 billion dollars. #17 When Barack Obama was first elected, the U.S. debt to GDP ratio was under 70 percent. Today, it is over 101 percent. #18 The U.S. national debt is on pace to approximately double during the eight years of the Obama administration. In other words, under Barack Obama the U.S. government will accumulate about as much debt as it did under all of the other presidents in U.S. history combined. #19 According to the New York Times, the “typical American household” is now worth 36 percent less than it was worth a decade ago. #20 The poverty rate in the United States has been at 15 percent or above for 3 consecutive years. This is the first time that has happened since 1965. #21 From 2009 through 2013, the U.S. government spent a whopping 3.7 trillion dollars on welfare programs. #22 While Barack Obama has been in the White House, the number of Americans on food stamps has gone from 32 million to 46 million. #23 Ten years ago, the number of women in the U.S. that had full-time jobs outnumbered the number of women in the U.S. on food stamps by more than a 2 to 1 margin. But now the number of women in the U.S. on food stamps actually exceeds the number of women that have full-time jobs. #24 One recent survey discovered that about 22 percent of all Americans have had to turn to a church food panty for assistance. #25 An astounding 45 percent of all African-American children in the United States live in areas of “concentrated poverty”. #26 40.9 percent of all children in the United States that are living with only one parent are living in poverty. #27 According to a report that was released late last year by the National Center on Family Homelessness, the number of homeless children in the United States has reached a new all-time record high of 2.5 million. Unfortunately, this is just the beginning. The incredibly foolish decisions that have been made by Obama, Congress and the Federal Reserve have brought us right to the precipice of another major financial crisis and another crippling economic downturn. So as bad as the numbers that I just shared with you above are, the truth is that they are nothing compared to what is coming. We are heading into the greatest economic crisis that any of us have ever seen, and it is going to shock the world. I hope that you are getting ready. |

01-20-15 | US SOU |

US ECONOMY |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| CENTRAL BANKING MONETARY POLICIES, ACTIONS & ACTIVITIES | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

SWISS PEG FAILURE - First Central Bank to Lose Control

As Bloomberg reports,

How big a problem is this? (via Goldman Sachs)

And despite the Polish Central Bank's comments that:

Here come the populist politicians to the rescue...

* * * * * * But Poland has a bigger problem than just mortgages. As Goldman Sachs goes on to explain...

* * * The Repercussions are only just starting... |

01-20-15 | MACRO MONETARY | CENTRAL BANKS |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

SWISS PEG FAILURE - First Central Bank to Lose Control The Financial System Broke Last Week 01-17-15 Phoenix Capital Research via ZH Global Central banks’ reputations are on borrowed time. ALL of the so called, “economic recovery” that began in 2009 has been based on the Central Banks’ abilities to rein in the collapse.

However, the insanity was in fact greater than this. It is one thing to bluff your way through the weakest recovery in 80+ years with empty promises; but it’s another thing entirely to roll the dice on your entire country’s solvency just to see what happens. JAPAN

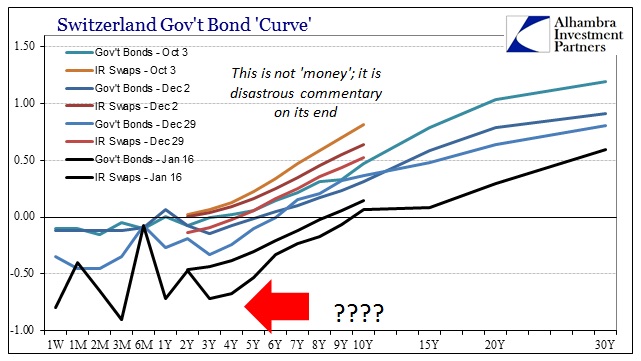

BROKEN This was the “Rubicon” moment: the instant at which Central Banks gave up pretending that their actions or policies were aimed at anything resembling public good or stability. It was now about forcing reality to match Central Bankers’ theories and forecasts. If reality didn’t react as intended, it wasn’t because the theories were misguided… it was because Central Bankers simply hadn’t left the paperweight on the “print” button long enough. At this point the current financial system was irrevocably broken. We simply had yet to feel it. SWISS PEG That is, until, last week, when the Swiss National Bank lost control, breaking a promise, and a currency peg, losing an amount of money equal to somewhere between 10% and 15% of Swiss GDP in a single day, and showing, once and for all, that there are problems so big that even the ability to print money can’t fix them. Please let this sink in: a Central bank lost control last week. This will not be a one-off event. With the Fed and other Central banks now leveraged well above 50-to-1, even those entities that were backstopping an insolvent financial system are themselves insolvent. The Big Crisis, the one in which entire countries go bust, has begun. It will not unfold in a matter of weeks; these sorts of things take months to complete. But it has begun. |

01-18-15 | MACRO MONETARY | CENTRAL BANKS |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

SWISS PEG FAILURE - Keynesian Central Banking Is Destroying Money And Markets The SNB's Wake-Up Call: Keynesian Central Banking Is Destroying Money And Markets 01-17-15 Jeffrey Snider of Alhambra Investment Partners via Contra Corner blog,via ZH It seems everyone was short the franc (CHF) as a matter of taking monetarism at face value. In other words, it amounted to believing the central party line about the economy and normalcy despite the fact that markets have been increasingly pessimistic about it all and actively and aggressively betting against it. Goldman Sachsis just one of many:

The only way to be surprised about the removal of the peg, or even to be short the franc in the first place, was spelled out in the first sentence, “as European growth normalized.” Being short the franc was essentially the same thing asbeing long the European economy. Given all that has transpired in the past seven or even eight months, there was no shortage of contrary indications that such an assumption was more than precarious and ultimately asymmetric against. Of course, the counter opinion is the same old “it wasn’t big enough last time but it will be this time.” In other words, the ABS, covered bond buying and negative nominal rates were just the warmup to the real QE event. Unfortunately, that is revisionist as the ECB has been taking intense monetary measures pretty steadily since the day it first announced the original OMT in the middle 2010. The only accomplishment in that time has been an internalrecalculation about “the economy” itself.

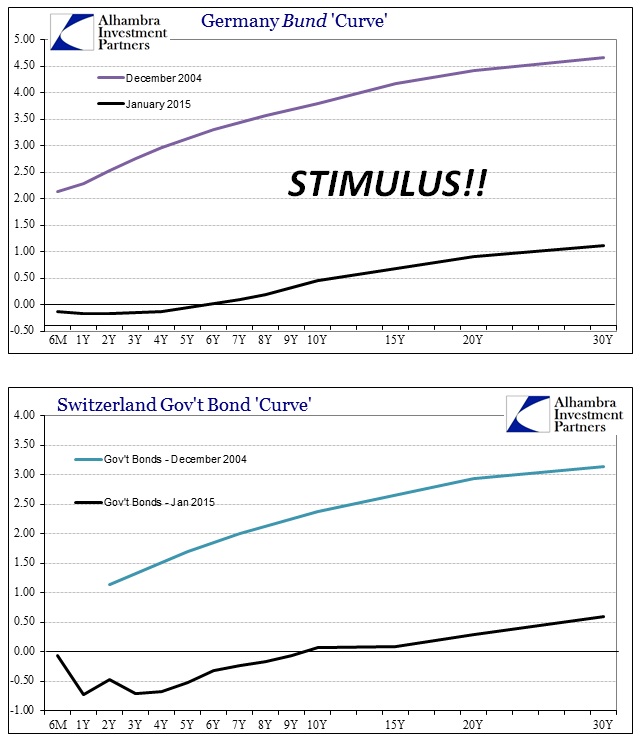

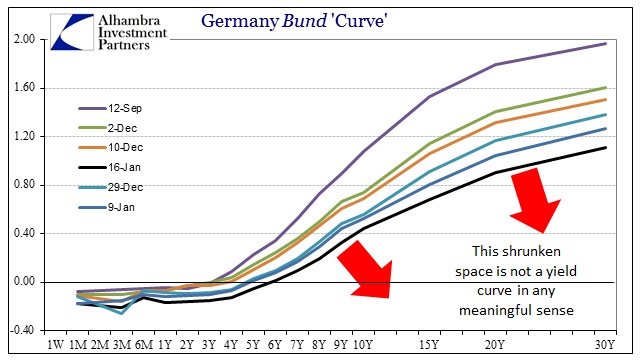

Nothing about Switzerland’s financial system in the latter half of 2014 was anything like a positive interpretation on the state of the European economy. In fact, the Swiss debauchery was as much screaming about the insanity of the ECB and just how ineffective and impotent the entire practical operation was right down to the smallest detail. The most obvious interpretation of the chart below is short the recovery in not just Europe, and not just from the past two days: The utter lunacy of the ECB is reaching its inevitable end because lunacy itself cannot create economic, or even financial, normalcy. The Keynesian heart of all of this is that they fully believe redistribution can make for potent economic tonic, but redistribution is at its root a very negative factor. So monetary theory attends to that by placing what it believes are limitations upon its usage and scale; “yes, inflation is bad, but we will only be using the slightest amount.” And you can easily see exactly what that “slightest amount” gains, as instead the failure of “just a little” redistribution is but added to; and then a little more; and a little more. It doesn’t take long before the constant hold of interventionary redistribution mangles even the most basic of functions in finance – the time value of money (credit). Central bankers will talk about “term premiums” as if that mattered to them in the slightest, rather speaking about such essential market function as if a field researcher gazing upon the rudimentary research subject. The object of redistribution is to kill money as if that will make people spend for the sake of spending. Instead they only kill basic interpretations of “money” and lead that suppression toward unbridled euphoria elsewhere. Just in these most basic terms, how low do interest rates have to be suppressed in order for this all to work?Well, if you believe the IS-LM framework then it all depends on the natural rate of interest, which has been “calculated”, apparently, even more negative than it supposedly has been since 2007. To an economist, let alone a central banker, the world is but a spreadsheet with equations that need to be balanced, and if there is no economic momentum than the balancing factor must be that natural interest rate. The more the economy fails to respond to “just a little” redistribution, the more negative the “natural” rate is equalized in the regression; in programming, this is referred to as an “infinite loop.” Alan Greenspan once queried the FOMC, in mid-2003, about what might happen once the zero lower bound was reached. That thought applied only to the shortest end of the credit space, the overnight rate at which the Fed thought it could control all the rest. In other words, because Greenspan, and the rest of them worldwide, believed that they could exert tremendous influence just from an overnight rate (that turned out to be more anachronistic than anesthetic) the economy’s variability might easily be corralled. That was the primary mistake of all of this, really, in that monetary authorities far overestimated (and continue to do so) their influence and the influence of the tools they used (which were relevant in the 1970’s far, far more than the 2000’s). It seems these same central bankers, in a mad dash toward proving they have at least some control, are going to take the whole damn thing, bills to notes to bonds, down to the zero lower bound. It started in Japan and has spread now to Europe, where Germany and Switzerland (and Denmark) are seeing negative rates out to 6 or even 9 years.

The zero lower bound was supposed to be a narrow and dangerous obstacle, not a universal standard. |

01-18-15 | MACRO MONETARY | CENTRAL BANKS |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Market | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| TECHNICALS & MARKET |

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

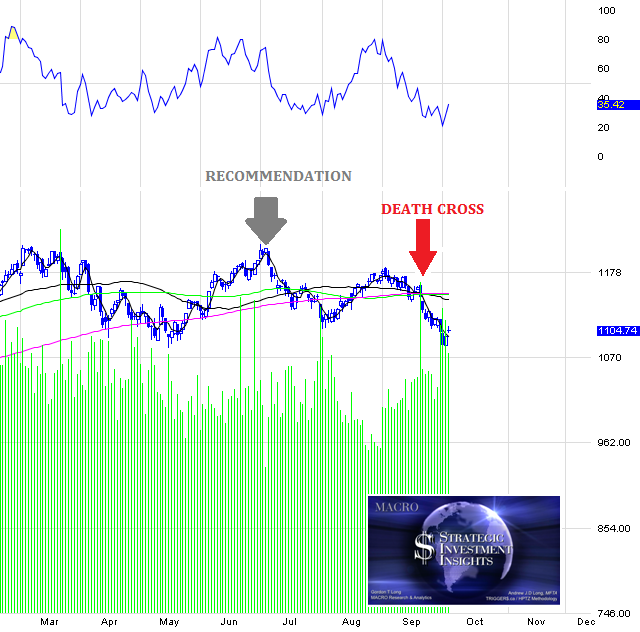

PATTERNS - Falling Earnings WHY THE SPX MACRO BIA$ IS NEGATIVE FOR Q1 1- DRAMATICALLY FALLING EARNINGS

2- WEAKENING MARGIN GROWTH

3- BOND SPREADS 4- WEAKENING BUYBACKS 5- BUSINESS CYCLE - 5 YEARS |

01-21-15 | PATTERNS | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| COMMODITY CORNER - AGRI-COMPLEX | PORTFOLIO | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| SECURITY-SURVEILANCE COMPLEX | PORTFOLIO | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| THESIS | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2014 - GLOBALIZATION TRAP | 2014 |  |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

2013 2014 |

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

2011 2012 2013 2014 |

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

CURRENCY WARS - Beggar-thy-Neighbor Central bank prophet fears QE warfare pushing world financial system out of control 01-20-15 UK Telegraph - Ambrose Evans-Pritchard, in Davos Former BIS chief economist warns that QE in Europe is doomed to failure and may draw the region into deeper difficulties The economic prophet who foresaw the Lehman crisis with uncanny accuracy is even more worried about the world's financial system going into 2015. Beggar-thy-neighbour devaluations are spreading to every region. All the major central banks are stoking asset bubbles deliberately to put off the day of reckoning. This time emerging markets have been drawn into the quagmire as well, corrupted by the leakage from quantitative easing (QE) in the West. "We are in a world that is dangerously unanchored," said William White, the Swiss-based chairman of the OECD's Review Committee. "We're seeing true currency wars and everybody is doing it, and I have no idea where this is going to end." Mr White is a former chief economist to the Bank for International Settlements - the bank of central banks - and currently an advisor to German Chancellor Angela Merkel. He said the global elastic has been stretched even further than it was in 2008 on the eve of the Great Recession. The excesses have reached almost every corner of the globe, and combined public/private debt is 20pc of GDP higher today. "We are holding a tiger by the tail," he said. He warned that QE in Europe is doomed to failure at this late stage and may instead draw the region into deeper difficulties. "Sovereign bond yields haven't been so low since the 'Black Plague': how much more bang can you get for your buck?" he told The Telegraph before the World Economic Forum in Davos. "QE is not going to help at all. Europe has far greater reliance than the US on small and medium-sized companies (SMEs) and they get their money from banks, not from the bond market," he said. "Even after the stress tests the banks are still in 'hunkering down mode'. They are not lending to small firms for a variety of reasons. The interest rate differential is still going up," he said. The warnings come just as the European Central Bank prepares a blitz of bond purchases at a crucial meeting on Thursday. Most ECB-watchers expect QE of around €500bn now that the eurozone is already in deflation. Even the Bundesbank is struggling to come with fresh reasons to oppose it. The psychological potency of this largesse will depend on whether the ECB opts for shock-and-awe concentration or trickles out the stimulus slowly. It also depends on the exact mechanism used to conduct QE, a loose term at best. ECB president Mario Draghi hopes that bond purchases will push money out into the broader economy through a "wealth effect", but critics fear this will be worse than useless if it leads to an asset bubble without gaining traction on the real economy. Classic moneratists say the ECB may end up spinning its wheels should it merely try to expand the money base. Mr White said QE is a disguised form of competitive devaluation. "The Japanese are now doing it as well but nobody can complain because the US started it," he said. "There is a significant risk that this is going to end badly because the Bank of Japan is funding 40pc of all government spending. This could end in high inflation, perhaps even hyperinflation. "The emerging markets got on the bandwagon by resisting upward pressure on their currencies and building up enormous foreign exchange reserves. The wrinkle this time is that ...corporations in these countries - especially in Asia and Latin America - have borrowed $6 trillion in US dollars, often through offshore centres. That is going to create a huge currency mismatch problem as US rates rise and the dollar goes back up." Mr White's warnings are ominous. He acquired great authority in his long years at the BIS arguing that global central banks were falling into a trap by holding real rates too low in the 1990s, effectively stealing growth from the future through "intertemporal" effects. He argues that this created a treacherous dynamic. The authorities kept having to push rates lower with the trough of each cycle, building up ever greater imbalances, in an ineluctable descent to the "zero bound", where monetary levers stop working properly. Under his guidance, the BIS annual reports over the three years before the Lehman crisis were a rising crescendo of alarm calls at a time when other global watchdogs were asleep. His legendary report in June 2008 openly discussed whether the world was on the cusp of events that might prove as dangerous and intractable as the Great Depression, as it indeed it was. Mr White said central banks have been put in an invidious position, compelled to respond to a deep economic disorder that is beyond their power. The latest victim is the Swiss National Bank, which was effectively crushed last week by greater global forces as it tried to repel safe-haven flows into the franc. The SNB was damned whatever it tried to do. "The only choice they had was to take a blow to the left cheek, or to the right cheek," he said. He deplores the rush to QE as an "unthinking fashion". Those who argue that the US and the UK are growing faster than Europe because they carried out QE early are confusing "correlation with causality". The Anglo-Saxon pioneers have yet to pay the price. "It ain't over until the fat lady sings. There are serious side-effects building up and we don't know what will happen when they try to reverse what they have done." The painful irony is that central banks may have brought about exactly what they most feared by trying to keep growth buoyant at all costs, he argues, and not allowing productivity gains to drive down prices gently as occurred in episodes of the 19th century. "They have created so much debt that they may have turned a good deflation into a bad deflation after all." |

01-23-15 | THEME | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| THEMES | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

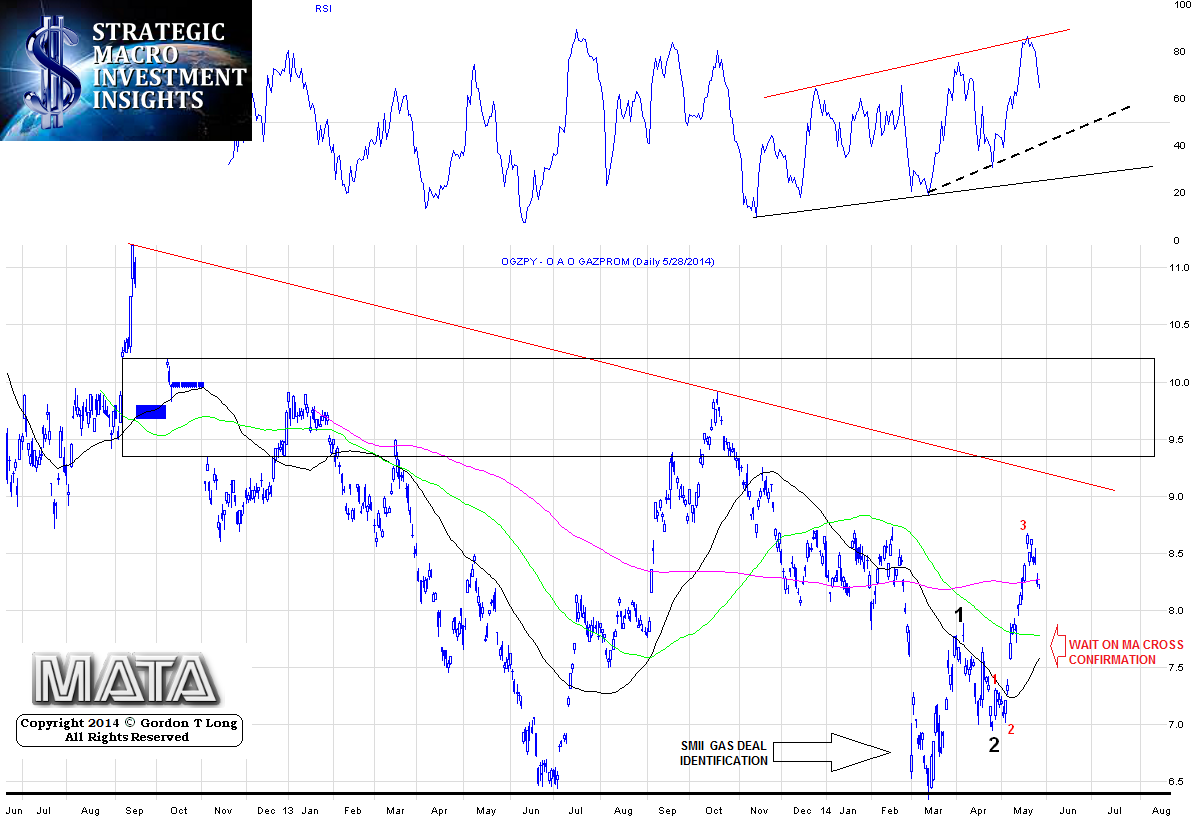

| FLOWS -FRIDAY FLOWS | THEME |  |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| SHADOW BANKING -LIQUIDITY / CREDIT ENGINE | THEME | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| CRACKUP BOOM - ASSET BUBBLE | THEME | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| ECHO BOOM - PERIPHERAL PROBLEM | THEME | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| PRODUCTIVITY PARADOX -NATURE OF WORK | THEME | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| STANDARD OF LIVING -EMPLOYMENT CRISIS | THEME | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| CORPORATOCRACY -CRONY CAPITALSIM | THEME |  |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

CORRUPTION & MALFEASANCE -MORAL DECAY - DESPERATION, SHORTAGES. |

THEME |  |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| SOCIAL UNREST -INEQUALITY & A BROKEN SOCIAL CONTRACT | THEME | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| SECURITY-SURVEILLANCE COMPLEX -STATISM | THEME | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| GLOBAL FINANCIAL IMBALANCE - FRAGILITY, COMPLEXITY & INSTABILITY | THEME | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| CENTRAL PLANINNG -SHIFTING ECONOMIC POWER | THEME | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| CATALYSTS -FEAR & GREED | THEME | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| GENERAL INTEREST |

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| STRATEGIC INVESTMENT INSIGHTS | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

SII | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

SII | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

SII | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

SII | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| TO TOP | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

As we noted last week,

As we noted last week,

Tipping Points Life Cycle - Explained

Click on image to enlarge

{kind=link}

{kind=link}

TO TOP

|

YOUR SOURCE FOR THE LATEST THINKING & RESEARCH

|

�

TO TOP