|

TODAY'S TIPPING POINTS TODAY'S TIPPING POINTS

|

pdf Download

Have your own site? Offer free content to your visitors with TRIGGER$ Public Edition!

Sell TRIGGER$ from your site and grow a monthly recurring income!

Contact [email protected] for more information - (free ad space for participating affiliates).

HOTTEST TIPPING POINTS |

|

|

Theme Groupings |

|

We post throughout the day as we do our Investment Research for:

LONGWave - UnderTheLens - Macro

Scroll TWEETS for LATEST Analysis Scroll TWEETS for LATEST Analysis

|

"BEST OF THE WEEK "

MOST CRITICAL TIPPING POINT ARTICLES TODAY

|

|

|

|

| Market - WEDNESDAY STUDIES |

| STUDIES - MACRO pdf |

|

|

|

TECHNICALS & MARKET

|

01-12-16 |

STUDY |

|

Clients told to seek safety of Bunds and Treasuries. 'This is about return of capital, not return on capital. In a crowded hall, exit doors are small'

RBS warned clients of trouble just before the 2008 crisis. It has done so again Photo: Getty Images

RBS has advised clients to brace for a “cataclysmic year” and a global deflationary crisis, warning that major stock markets could fall by a fifth and oil may plummet to $16 a barrel.

The bank’s credit team said markets are flashing stress alerts akin to the turbulent months before the Lehman crisis in 2008. “Sell everything except high quality bonds. This is about return of capital, not return on capital. In a crowded hall, exit doors are small,” it said in a client note.

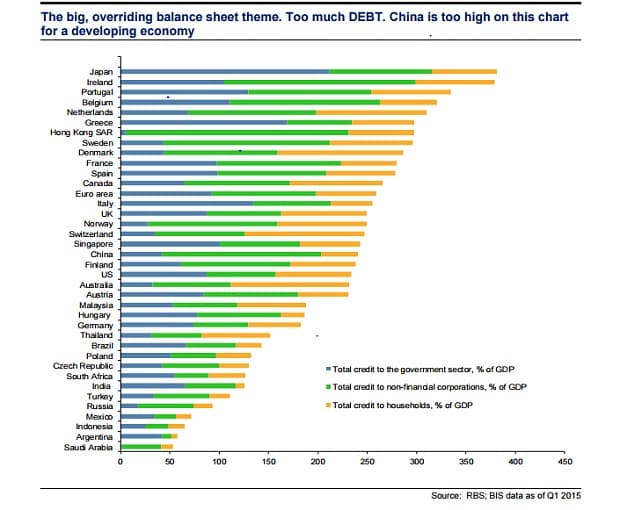

Andrew Roberts, the bank’s credit chief, said that global trade and loans are contracting, a nasty cocktail for corporate balance sheets and equity earnings. This is particularly ominous given that global debt ratios have reached record highs.

Mr Roberts expects Wall Street and European stocks to fall by 10pc to 20pc, with even an deeper slide for the FTSE 100 given its high weighting of energy and commodities companies. “London is vulnerable to a negative shock. All these people who are ‘long’ oil and mining companies thinking that the dividends are safe are going to discover that they’re not at all safe,” he said.

Brent oil prices will continue to slide after breaking through a key technical level at $34.40, RBS claimed, with a “bear flag” and “Fibonacci” signals pointing to a floor of $16, a level last seen after the East Asia crisis in 1999. The bank said a paralysed OPEC seems incapable of responding to a deepening slowdown in Asia, now the swing region for global oil demand.

Morgan Stanley has also slashed its oil forecast, warning that Brent could fall to $20 if the US dollar keeps rising. It argued that oil is intensely leveraged to any move in the dollar and is now playing second fiddle to currency effects.

RBS forecast that yields on 10-year German Bunds would fall time to an all-time low of 0.16pc in a flight to safety, and may break zero as deflationary forces tighten their grip. The European Central Bank’s policy rate will fall to -0.7pc.

US Treasuries will fall to rock-bottom levels in sympathy, hammering hedge funds that have shorted US bonds in a very crowded “reflation trade”.

RBS first issued its grim warnings for the global economy in November but events have moved even faster than feared. It estimates that the US economy slowed to a growth rate of 0.5pc in the fourth quarter, and accuses the US Federal Reserve of “playing with fire” by raising rates into the teeth of the storm. “There has already been severe monetary tightening in the US from the rising dollar,” it said.

It is unusual for the Fed to tighten when the ISM manufacturing index is below the boom-bust line of 50. It is even more surprising to do so after nominal GDP growth has fallen to 3pc and has been trending down since early 2014. It is unusual for the Fed to tighten when the ISM manufacturing index is below the boom-bust line of 50. It is even more surprising to do so after nominal GDP growth has fallen to 3pc and has been trending down since early 2014.

RBS said the epicentre of global stress is China, where debt-driven expansion has reached saturation. The country now faces a surge in capital flight and needs a “dramatically lower” currency. In their view, this next leg of the rolling global drama is likely to play out fast and furiously.

“We are deeply sceptical of the consensus that the authorities can ‘buy time’ by their heavy intervention in cutting reserve ratio requirements (RRR), rate cuts and easing in fiscal policy,” it said.

Mr Roberts said the tightening cycle by the Anglo-Saxon central banks is already over. There will be no rate rises by the Bank of England before the downturn hits, and the next action by the Fed may be a humiliating volte-face and a rate cut.

RBS is not alone in fearing trouble. UBS issued what it called a “significant change” to its house view late last week, saying policy chaos in China had unsettled markets. It cut exposure to equities from overweight to neutral on a “six-month tactical horizon”. It went underweight emerging markets.

UBS said it is a precautionary move, insisting that the current global credit cycle has not yet peaked. Low oil prices should ultimately feed through to higher consumer spending and boost growth.

Larry Summers, the former US Treasury Secretary, said it would be a mistake to dismiss the current financial squall as froth. Markets often sense a gathering storm when policy-makers are still asleep at the wheel. He has long argued that the world economy is so far out of kilter that it takes permanent financial bubbles to keep growth going, an inherently unstable structure.

Yet there is something strange about the latest events. Austerity is finally over in Europe and fiscal policy in the US this year will be expansionary.

China’s slowdown hit its bottom in June and a fitful recovery has been building, driven by extra budget spending and credit growth. While the composite PMI indicator for manufacturing and services slipped back last month, it is still higher in the summer.

David Owen, from Jefferies, said there is a “weird disconnect” between the economic fundamentals and the market malaise.

“There is no evidence of anything rolling over in the US. Europe is clearly recovering and the M3 money supply in Germany is growing at almost 10pc, which normally means stronger activity,” he said.

Bank of America said panic selling had triggered its “contrarian buy signal”, since 88pc of global equity indexes are now trading below their 200-day and 50-day moving averages. The "Bull & Bear" index is at an ultra-negative level of 1.3.

It said a “big tradable multi-week rally awaits” but requires catalysts, above all a stabilisation of the Chinese yuan and oil, better PMI data and a halt to the rising dollar.

The risk is that this market storm drags on long enough to hit investment, regardless of what the economic data should imply. At the end of the day, market psychology can itself become an economic "fundamental".

Pessimists warn that unless there is a batch of irrefutably good data from China over the next two or three months, the sell-off could become self-fulfilling and quickly metamorphose into the next global crisis.

|

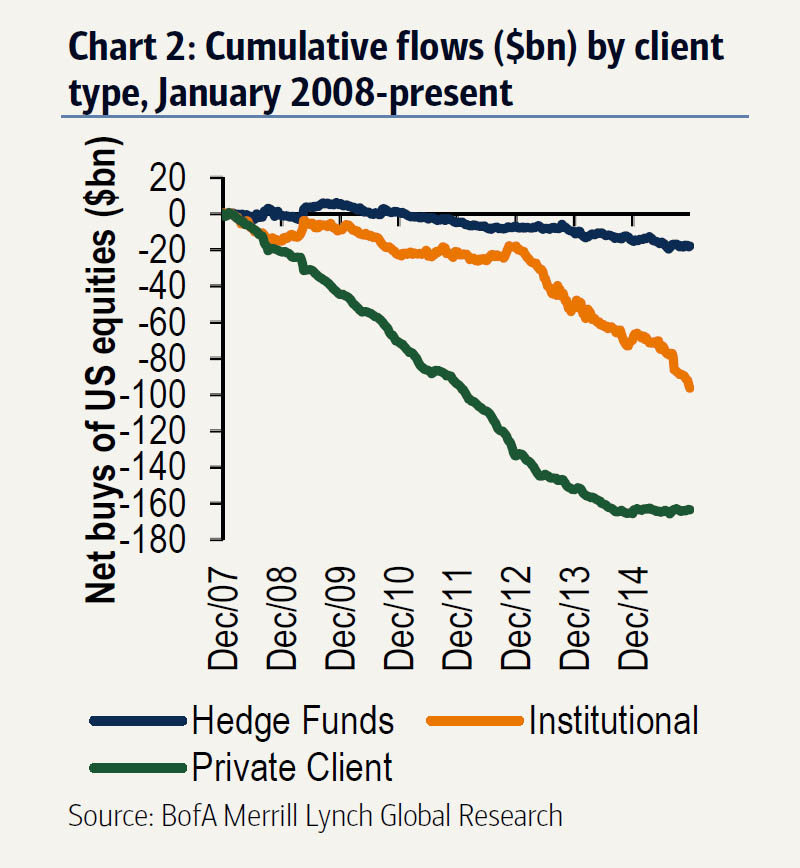

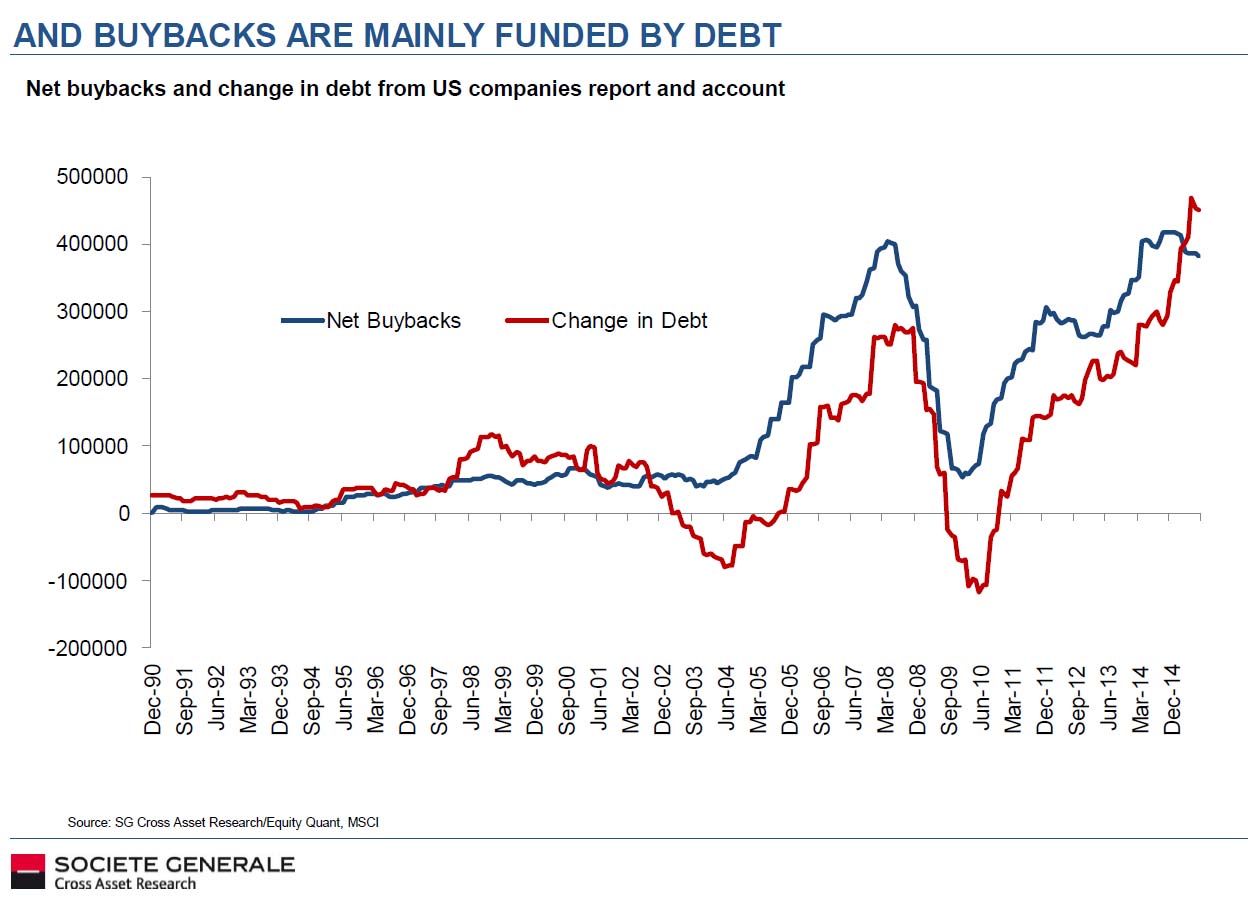

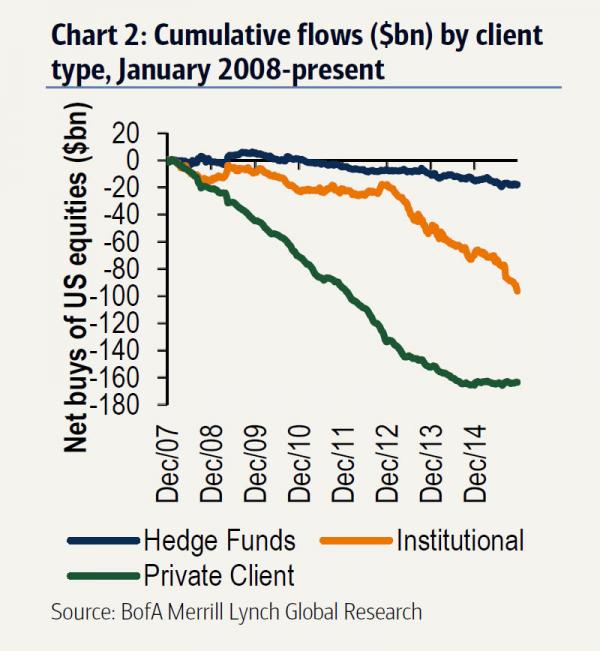

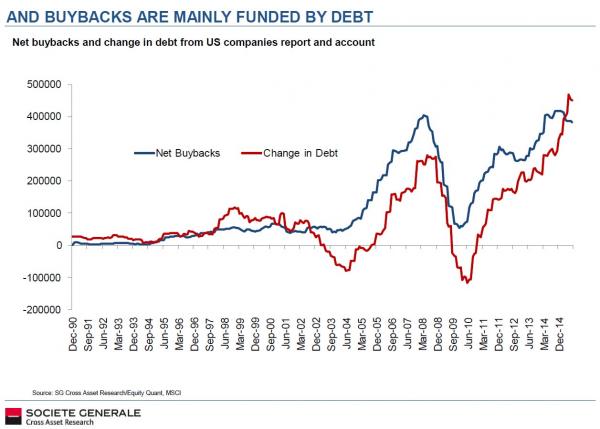

As we have reported on numerous prior occasions, the biggest marginal buyer of stocks in both 2014 and 2015 (and forecast to remain in 2016), are corporations themselves, using debt-funded buybacks to push their stocks to record highs, allowing the smart money to sell in record amounts.

But what happens when companies are so levered that they can't possibly afford to issue any more debt, virtually all of which has been used to repurchase stocks, as we have shown before...

... especially in a time when yields on Investment Grade bonds are rising courtesy of the first Fed rate hike in nearly a decade, and when cash flows are sliding faster with every passing year?

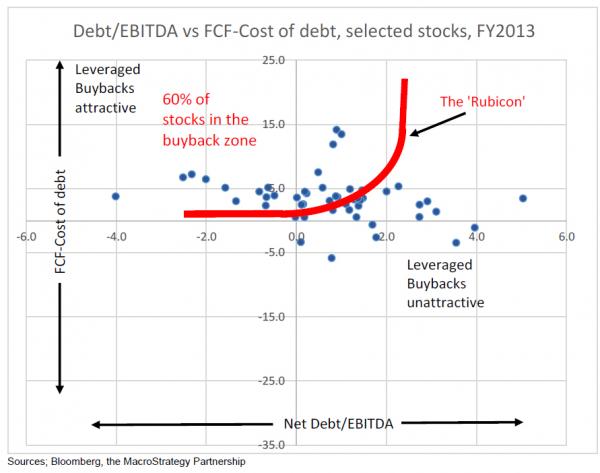

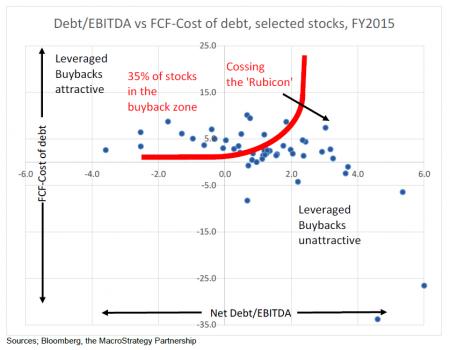

For another version of the answer we have provided many times before, we go to MacroStrategy's Julien Garran, who informs us that as credit & returns deteriorate, an increasing number of stocks are crossing the "Rubicon." By Rubicon he means the "cut-off point where corporates can no longer justify gearing up to do buybacks. In 2013, 60% of my sample could justify buybacks. Since then, US corporates have raised debt by US$1.1trn and bought back US$1.1trn of stock. But now, with debt levels & costs up, and returns down, only 35% make the grade." That, in his view is also the key to the narrowing breadth in the market. His conclusion: breadth is now set to narrow to the point where the whole market turns down in 2016.

Some more details on Crossing the Rubicon:

Why does breadth decline? In my view, corporates’ ability to gear-up and buy-back stock is critical to the story.

From the start of 2014, US corporates covered their entire capex budgets from internal funds. They then raised US$1.1trn of debt to do US$1.1trn of corporate buybacks (Data from the Fed’s Z1 report & Factset).

The combination of rising debt, deteriorating returns and a rising cost of debt means that, increasingly, corporate’s debt levels threaten their credit ratings, or their marginal cost of debt deteriorates relative to their cashflow yields. Both threaten their ability to gear up to buy back stock. And both threaten the value of their equity.

As more companies cross the Rubicon out of the buyback zone, the bid for their equity shrivels. The key to trading the topping process is to sell the sectors which will see their margin cost of debt rise above the free cashflow from new business. Clearly the extractive industries, the utilities, and several industrial and retail companies have already crossed the line. I think that the leveraged buyout firms in the US are likely the next to go, as their cost of funding continues to blow out.

To show the process, I have taken 50 S&P companies from 10 sectors (excluding financials). I've put them in a matrix with net debt/EBITDA on the horizontal axis and the free cashflow yield less the cost of debt on the vertical axis. The zone to the left and above the red line show the prime opportunities for gearing up for buybacks. That’s because free cashflow yields are well above the current marginal cost of debt, and net debt to EBITDA is contained. The zone to the right & below the red line shows stocks that will struggle to gear up for buybacks – either because their cost of debt is up to or above their free-cashflow yields, or because the net debt to EBITDA is too high.

For the 2013 financial year, 60% of stocks in my sample were in good shape to gear-up for buybacks.

By the end of 2015, just 35% of the sample were in good shape to do buybacks.

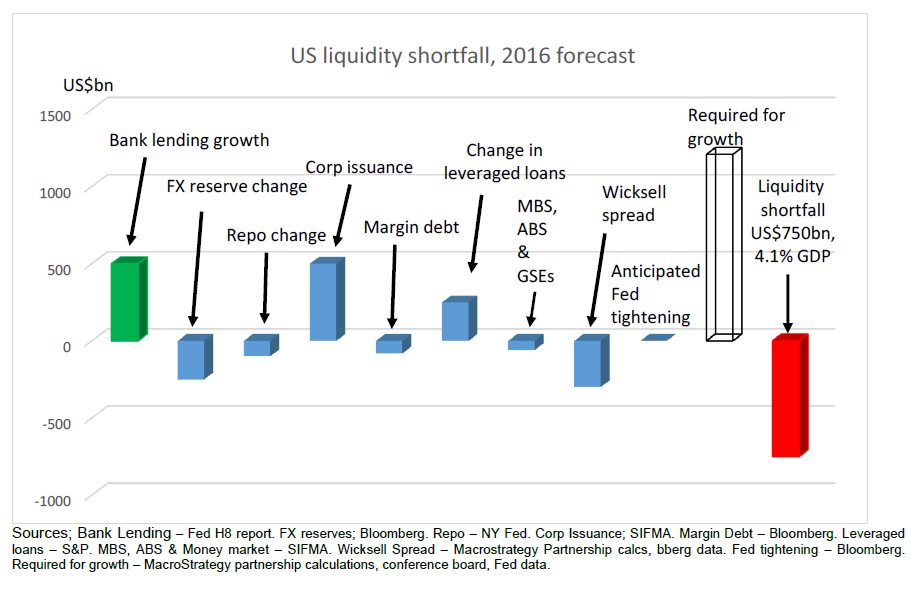

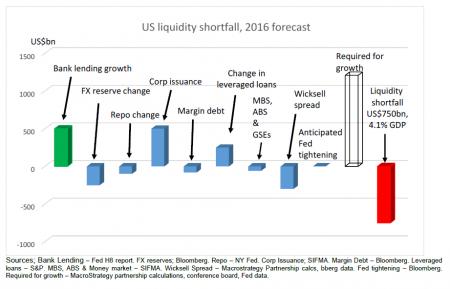

I estimate that the liquidity shortfall will expand further in 2016, to US$750bn. Against that backdrop, I expect more pressure on credit, returns & growth, more corporates will cross the Rubicon. And as that continues I expect that buyback activity will fade further, and the net bid for equities will likely evaporate.

The conclusion:

My recommendations are; Short US indices, long the US$, long gold & gold equities & short the leveraged buyout sector in the US.

So is 2016 the year it all falls apart? Stay tuned for the follow up comments from Garran because if he is right, the answer is a resounding yes.

|

| |

TIPPING POINTS, STUDIES, THESIS, THEMES & SII

COVERAGE THIS WEEK PREVIOUSLY POSTED - (BELOW)

|

| MOST CRITICAL TIPPING POINT ARTICLES THIS WEEK - Jan 10th, 2016 - Jan 16th, 2016 |

|

|

|

| TIPPING POINTS - This Week - Normally a Tuesday Focus |

| BOND BUBBLE |

|

|

1 |

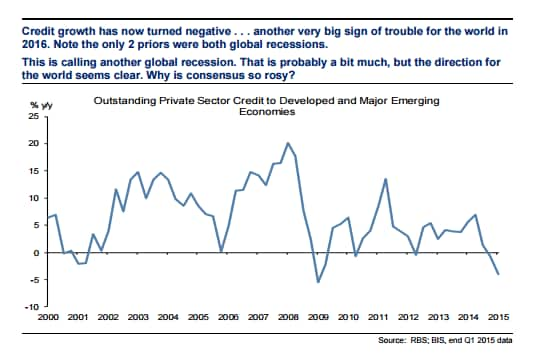

BOND BUBBLE

THE ONE CHART YOU SHOULD BE PAYING ATTENTION TO!

|

01-12-16 |

|

1 |

| RISK REVERSAL - WOULD BE MARKED BY: Slowing Momentum, Weakening Earnings, Falling Estimates |

|

|

2 |

| GEO-POLITICAL EVENT |

|

|

3 |

| CHINA BUBBLE |

|

|

4 |

| JAPAN - DEBT DEFLATION |

|

|

5 |

EU BANKING CRISIS |

|

|

6 |

| TO TOP |

| MACRO News Items of Importance - This Week |

GLOBAL MACRO REPORTS & ANALYSIS |

|

|

|

US ECONOMIC REPORTS & ANALYSIS |

|

|

|

| CENTRAL BANKING MONETARY POLICIES, ACTIONS & ACTIVITIES |

|

|

|

|

|

|

|

| Market - WEDNESDAY STUDIES |

| STUDIES - MACRO pdf |

|

|

|

TECHNICALS & MARKET |

|

STUDY |

|

China's market turmoil and an extended downturn in oil wreaked havoc on stocks this week, with the S&P 500 Index and the Dow Jones Industrial Average off to their worst start of a year.

The sell-off has some questioning the strength of the U.S. economy, but few think the world's largest growth center is at risk for a contraction. However, one widely regarded investor says there's little debate: the U.S. is likely already in a recession—and he claims to have hard numbers to bolster his case.

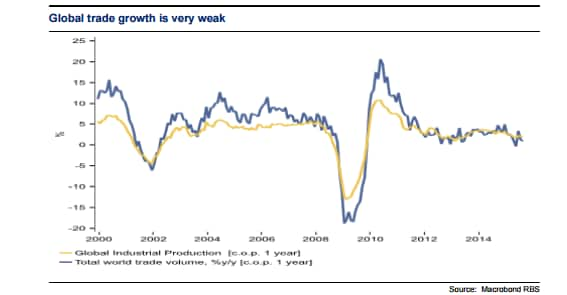

Looking at International Monetary Fund data, "the year-over-year change in global exports is at the second lowest level since 1958," Raoul Pal, Publisher of the Global Macro Investor told CNBC's"Fast Money" this week. Basically, it means economies around the world are shipping their goods at near historically low levels. "Something massive is going on in the global economy and people are missing it," Pal added.

The steep decline in 2015 exports is second only to 2009, when the global recession led to a 37 percent drop in export growth.

Read More US close to recession, world already in one: Pro

There are two main contributing factors to this recession, Pal told CNBC:

-

-

China's slowdown.

The greenback's strength has helped keep a lid on energy prices, but it's had undeniable spillover effects, the investor said.

"It started unraveling in oil and all commodities, that impacted exports. Everyone had dollar debts and no one had money," Pal added.

The investor correctly predicted the dollar's surge back in November 2014 on CNBC's "Fast Money". Since that call, the dollar has risen 15 percent—an ascent that Pal believes will only continue due to the shortage of dollars globally.

"I don't think I've ever been this right in my career," Pal said.

The dollar's sustained strength has called into question moves by the Federal Reserve and shaken commodity markets. For the time being, Pal believes the greenback's got nowhere else to go but up –and global markets are going to pay for it.

"The markets are following a pattern. Growth has been revised down and it looks like the markets will have to" compensate for the adjustment, Pal said.

"China is certainly a big mess and it's likely to get worse," he said. "Even whether they devalue their currency sharply or slowly, there's still a big mess to work out with all of the debts in the system. I think it's a problem."

Despite the doom and gloom Pal predicted, he suggested one buying opportunity.

"Right now I think one of the best bets in the world is to own the TLT or bonds," Pal said, speaking of the iShares bond exchange traded fund and government debt.

"No one is long of bonds and I think the most likely outcome is that the bond market has a huge rally, expressing inflation."

|

| |

| COMMODITY CORNER - AGRI-COMPLEX |

|

|

|

|

|

|

|

| THESIS - Mondays Posts on Financial Repression & Posts on Thursday as Key Updates Occur |

| 2015 - FIDUCIARY FAILURE |

2015 |

THESIS 2015 |

|

| 2014 - GLOBALIZATION TRAP |

2014 |

|

|

2013 - STATISM |

2013-1H

2013-2H |

|

|

2012 - FINANCIAL REPRESSION |

2012

2013

2014 |

|

|

FINANCIAL REPRESSION |

01-11-16 |

|

|

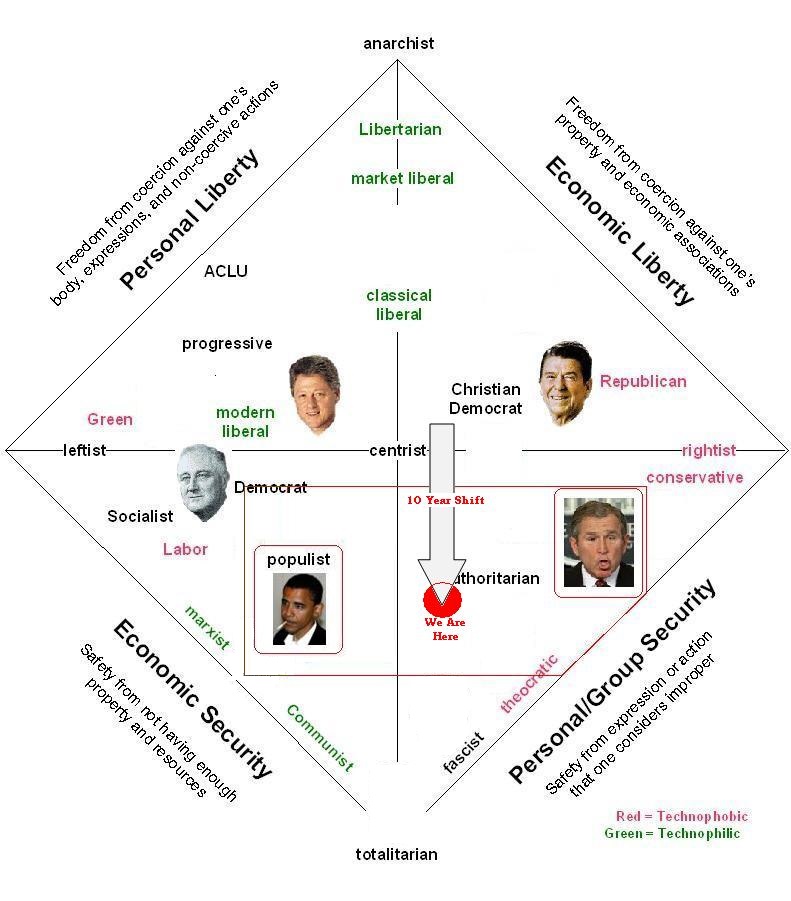

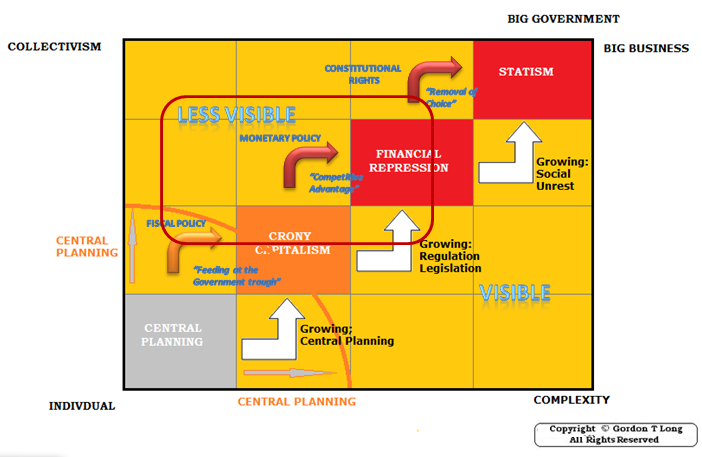

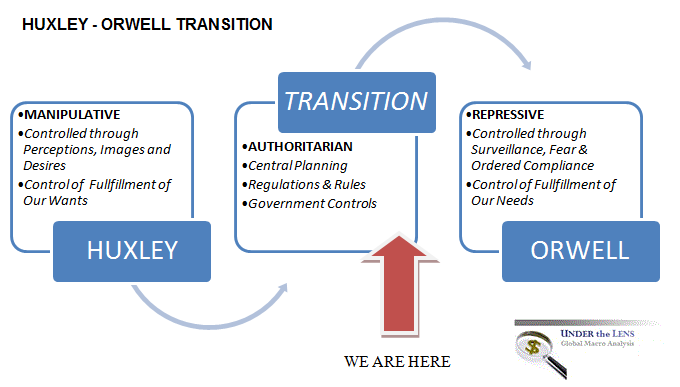

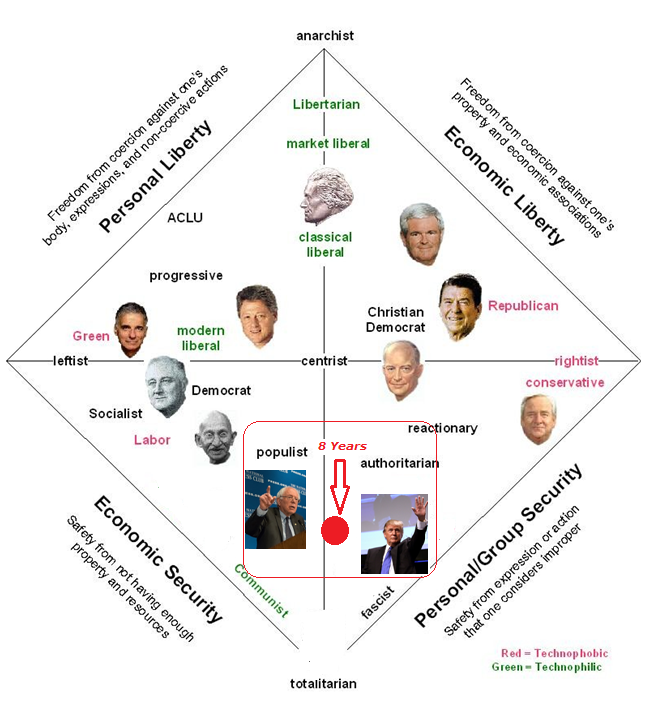

Recent research released by both the Pew Research Center and Gallup warn of an accelerating erosion in confidence in our government, politicians and the political process. It is clear to most that we have a growing “Crisis of Trust” which is signaling a “Failure of Leadership” as governments steadily exert increasing power and authority over our lives!

FOUR YEARS AGO WE BECAME SERIOUSLY ALARMED!

In the fall of 2012 having become seriously alarmed, we wrote our annual thesis paper entitled “STATISM” and laid out the frightening direction of US political leadership. We had initially hoped it was a cyclical pattern which had reached a cyclical bottom.

WE FOCUSED, MAPPED & TRACKED IT

Our subsequent research efforts have resulted in a large supporting video library of expert guest interviews at Macro embellishing on each of the sequentially emerging boxes in the following road-map and additionally the creation of the Financial Repression Authority to understand how our sacred public freedoms were being unwittingly surrendered through financial bondage.

The detailed research included a focus on the driving linkages between the identified stages as the developed economies (and the US in particular) accelerated towards more centralized government control of almost all facets of our lives.

WHERE WE FIND OURSELVES TODAY

The facts are overwhelming and indisputable for anyone taking the time (which we did) to do their ‘due diligence’. Time and space which we don’t have here.

As we now agonizingly watch the US Presidential Primary Campaigns, cognoscente of what we previously witnessed in the UK (Jeremy Corbyn), Italy (Beppo Brillo), France (Marie Le Pen) and a raft of other political hot areas, we see a now unquestionable deteriorating shift. A shift firmly rooted in a Crisis of Trust and a direct result of a Failure of Leadership.

ONE CRISIS WAY FROM A MONUMENTAL “TOTALITARIAN” MISTAKE

The Financial Repression Authority is presently concerned that a Geo-political event, conflict or crisis could soon abruptly catapult the developed economies into a mistaken political direction and a deeper cyclical low. A cycle which is presently already on a dangerous trajectory. Paul Craig Roberts (a former US Assistant Treasury Secretary) just frustratingly penned “The Rule Of Law No Longer Exists In Western Civilization” outlining the seriousness of criminal and immoral actions by the US government. He illustrates that the dictatorial methods and unlegislated executive orders by the current President to overturn the Second Amendment are now the political leadership ‘order of the day’ and writes: “He (Obama) has the corrupt US Department of Justice, a criminal organization, looking for ways for the dictator to overturn both Congressional legislation and Supreme Court rulings.”

CONCLUSION

Paul Craig Roberts and the Financial Repression Authority (FRA) sadly concludes – “Out of Evil comes Dictatorship”

As the insightful Canadian national anthem warns so well, we must all “Stand on Guard for Thee!”

Never more than today.

|

2011 - BEGGAR-THY-NEIGHBOR -- CURRENCY WARS |

2011

2012

2013

2014 |

|

|

2010 - EXTEND & PRETEND |

|

|

|

| THEMES - Normally a Thursday "Themes" Post & a Friday "Flows" Post |

I - POLITICAL |

|

|

|

CENTRAL PLANNING - SHIFTING ECONOMIC POWER - STATISM

MACRO MAP - EVOLVING ERA OF CENTRAL PLANNING

|

G |

THEME |

|

| - - CRISIS OF TRUST - Era of Uncertainty |

G |

THEME |

|

CORRUPTION & MALFEASANCE - MORAL DECAY - DESPERATION - RESENTMENT. |

US |

THEME PAGE |

|

| - - SECURITY-SURVEILLANCE COMPLEX - STATISM |

G |

THEME |

|

| - - CATALYSTS - FEAR (POLITICALLY) & GREED (FINANCIALLY) |

G |

THEME |

|

II-ECONOMIC |

|

|

|

| GLOBAL RISK |

|

|

|

| - GLOBAL FINANCIAL IMBALANCE - FRAGILITY, COMPLEXITY & INSTABILITY |

G |

THEME |

|

| - - SOCIAL UNREST - INEQUALITY & A BROKEN SOCIAL CONTRACT |

US |

THEME |

|

| - - ECHO BOOM - PERIPHERAL PROBLEM |

M |

THEME |

|

| - -GLOBAL GROWTH & JOBS CRISIS |

|

|

|

| - - - PRODUCTIVITY PARADOX - NATURE OF WORK |

|

THEME |

MA w/ CHS |

| |

01-08-16 |

THEME |

MA w/ CHS |

| - - - STANDARD OF LIVING - EMPLOYMENT CRISIS, SUB-PRIME ECONOMY |

US |

THEME |

MA w/ CHS |

III-FINANCIAL |

|

|

|

FLOWS -FRIDAY FLOWS

FLOWS - Liqudity, Credit & Debt

LIQUIDITY: Central Bank Liquidity Increases has slowed or Stopped

>> CREDIT: Cycle has turned

DEBT: Defaults/ Bankruptcies Will Emerge

|

MATA

RISK ON-OFF |

THEME |

w/ R Duncan

|

| CRACKUP BOOM - ASSET BUBBLE |

12-31-15 |

THEME |

|

| SHADOW BANKING - LIQUIDITY / CREDIT ENGINE |

M |

THEME |

|

| GENERAL INTEREST |

|

|

|

| STRATEGIC INVESTMENT INSIGHTS - Weekend Coverage |

|

|

|

|

RETAIL - CRE

|

|

SII |

|

US DOLLAR

|

|

SII |

|

YEN WEAKNESS

|

|

SII |

|

OIL WEAKNESS

|

|

SII |

|

| TO TOP |

| |

Read More - OUR RESEARCH - Articles Below

Tipping Points Life Cycle - Explained

Click on image to enlarge

|

YOUR SOURCE FOR THE LATEST

GLOBAL MACRO ANALYTIC

THINKING & RESEARCH

|

�

|

| TERMS OF USE |

Gordon T Long is not a registered advisor and does not give investment advice. His comments are an expression of opinion only and should not be construed in any manner whatsoever as recommendations to buy or sell a stock, option, future, bond, commodity or any other financial instrument at any time. Of course, he recommends that you consult with a qualified investment advisor, one licensed by appropriate regulatory agencies in your legal jurisdiction, before making any investment decisions, and barring that, we encourage you confirm the facts on your own before making important investment commitments.

THE CONTENT OF ALL MATERIALS: SLIDE PRESENTATION AND THEIR ACCOMPANYING RECORDED AUDIO DISCUSSIONS, VIDEO PRESENTATIONS, NARRATED SLIDE PRESENTATIONS AND WEBZINES (hereinafter "The Media") ARE INTENDED FOR EDUCATIONAL PURPOSES ONLY.

The Media is not a solicitation to trade or invest, and any analysis is the opinion of the author and is not to be used or relied upon as investment advice. Trading and investing can involve substantial risk of loss. Past performance is no guarantee of future returns/results. Commentary is only the opinions of the authors and should not to be used for investment decisions. You must carefully examine the risks associated with investing of any sort and whether investment programs are suitable for you. You should never invest or consider investments without a complete set of disclosure documents, and should consider the risks prior to investing. The Media is not in any way a substitution for disclosure. Suitability of investing decisions rests solely with the investor. Your acknowledgement of this Disclosure and Terms of Use Statement is a condition of access to it. Furthermore, any investments you may make are your sole responsibility.

THERE IS RISK OF LOSS IN TRADING AND INVESTING OF ANY KIND. PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS.

Gordon emperically recommends that you consult with a qualified investment advisor, one licensed by appropriate regulatory agencies in your legal jurisdiction, before making any investment decisions, and barring that, he encourages you confirm the facts on your own before making important investment commitments.

|

DISCLOSURE STATEMENT

|

Information herein was obtained from sources which Mr. Long believes reliable, but he does not guarantee its accuracy. None of the information, advertisements, website links, or any opinions expressed constitutes a solicitation of the purchase or sale of any securities or commodities.

Please note that Mr. Long may already have invested or may from time to time invest in securities that are discussed or otherwise covered on this website. Mr. Long does not intend to disclose the extent of any current holdings or future transactions with respect to any particular security. You should consider this possibility before investing in any security based upon statements and information contained in any report, post, comment or recommendation you receive from him. |

|

FAIR USE NOTICE This site contains

copyrighted material the use of which has not always been specifically

authorized by the copyright owner. We are making such material available in

our efforts to advance understanding of environmental, political, human

rights, economic, democracy, scientific, and social justice issues, etc. We

believe this constitutes a 'fair use' of any such copyrighted material as

provided for in section 107 of the US Copyright Law. In accordance with

Title 17 U.S.C. Section 107, the material on this site is distributed

without profit to those who have expressed a prior interest in receiving the

included information for research and educational purposes.

If you wish to use

copyrighted material from this site for purposes of your own that go beyond

'fair use', you must obtain permission from the copyright owner.

COPYRIGHT © Copyright 2010-2011 Gordon T Long. The information herein was obtained from sources which Mr. Long believes reliable, but he does not guarantee its accuracy. None of the information, advertisements, website links, or any opinions expressed constitutes a solicitation of the purchase or sale of any securities or commodities. Please note that Mr. Long may already have invested or may from time to time invest in securities that are recommended or otherwise covered on this website. Mr. Long does not intend to disclose the extent of any current holdings or future transactions with respect to any particular security. You should consider this possibility before investing in any security based upon statements and information contained in any report, post, comment or recommendation you receive from him.

|

|